|

市場調查報告書

商品編碼

1415443

鋼鐵市場:按產品、型態和最終用途行業 - 2024-2030 年全球預測Iron & Steel Market by Product (Iron Ore, Steel), Form (Pipes/Tubes, Rods/Bars, Sheets/Plates), End-Use Industry - Global Forecast 2024-2030 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

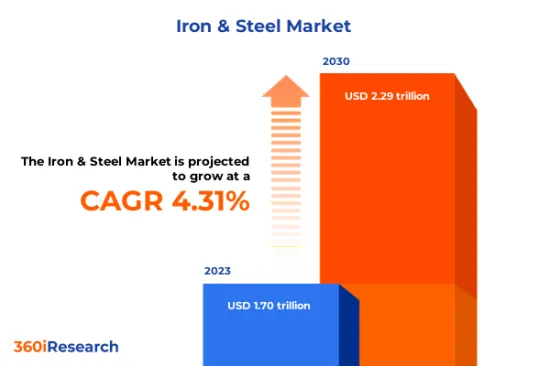

預計2023年鋼鐵市場規模為1.7兆美元,2024年達到1.77兆美元,預計2030年將達2.29兆美元,複合年成長率為4.31%。

全球鋼鐵市場

| 主要市場統計 | |

|---|---|

| 基準年[2023] | 1.7兆美元 |

| 預測年份 [2024] | 1.77兆美元 |

| 預測年份 [2030] | 2.29兆美元 |

| 複合年成長率(%) | 4.31% |

鋼鐵市場包括源自鐵礦石和回收金屬廢料的金屬原料的生產、分銷和消費。這些原料被加工成各種行業的各種最終產品,包括汽車、建築、航太、能源、包裝和重型機械。全球鋼鐵業競爭激烈,擁有多元化的鐵合金產品系列,包括碳鋼、合金鋼、不銹鋼、鑄鐵、生鐵、熟鐵和其他特殊金屬。世界快速的都市化正在增加對住宅和商業建築、道路、橋樑和交通基礎設施的需求,而這些都需要關鍵的鋼鐵產品。此外,汽車產業以及能源和電力產業鋼鐵消費的增加正在推動市場成長。然而,鋼鐵市場受到溫室氣體排放和價格波動等環境問題的影響,影響整個價值鏈的盈利。市場相關人員加大對新興國家鋼鐵的投資和政府支持。此外,採用以舉措為重點的舉措,例如基於氫的綠色鋼鐵生產技術和基於回收的循環經濟模式,可以減少能源消耗和碳排放,為市場帶來了利潤豐厚的機會。

區域洞察

在美洲,由於最近對設備現代化和加強生產流程的投資,美國出現了顯著成長,加拿大也是該地區鋼鐵生產的主要貢獻者。兩國共用相似的消費者需求和購買行為,主要是由基礎設施和汽車製造業所推動的。在歐洲、中東和非洲地區,德國的粗鋼產量領先歐洲,其次是義大利、法國和西班牙。由於快速都市化以及建築、石油和天然氣以及交通運輸等關鍵產業的成長,中東地區的鋼鐵需求不斷增加。在非洲,南非因其發達的採礦業而成為主要生產國,為當地生產提供原料。在亞太地區,中國在全球鋼鐵工業中佔據主導地位,其龐大的人口帶動了國內對建築材料、汽車、機械和家用電器的需求。日本以其生產優質鋼材的先進技術而聞名。同時,印度日益都市化,並大力投資基礎設施計劃,刺激了對鋼鐵產品的需求。

FPNV定位矩陣

FPNV定位矩陣對於評估鋼鐵市場至關重要。我們檢視與業務策略和產品滿意度相關的關鍵指標,以對供應商進行全面評估。這種深入的分析使用戶能夠根據自己的要求做出明智的決策。根據評估,供應商被分為四個成功程度不同的像限:前沿(F)、探路者(P)、利基(N)和重要(V)。

市場佔有率分析

市場佔有率分析是一種綜合工具,可以對鋼鐵市場供應商的現狀進行深入而深入的研究。全面比較和分析供應商在整體收益、基本客群和其他關鍵指標方面的貢獻,以便更好地了解公司的績效及其在爭奪市場佔有率時面臨的挑戰。此外,該分析還提供了對該行業競爭特徵的寶貴考察,包括在研究基準年觀察到的累積、分散主導地位和合併特徵等因素。這種詳細程度的提高使供應商能夠做出更明智的決策並制定有效的策略,從而在市場上獲得競爭優勢。

該報告對以下幾個方面提供了寶貴的見解:

1-市場滲透率:提供有關主要企業所服務的市場的全面資訊。

2-市場開拓:我們深入研究利潤豐厚的新興市場,並分析它們在成熟細分市場中的滲透率。

3- 市場多元化:提供有關新產品發布、開拓地區、最新發展和投資的詳細資訊。

4-競爭力評估與資訊:對主要企業的市場佔有率、策略、產品、認證、監管狀況、專利狀況、製造能力等進行全面評估。

5- 產品開發與創新:提供對未來技術、研發活動和突破性產品開發的見解。

本報告解決了以下關鍵問題:

1-鋼鐵市場的市場規模和預測是多少?

2-在鋼鐵市場預測期內需要考慮投資哪些產品、細分市場、應用和領域?

3-鋼鐵市場的技術趨勢和法律規範是什麼?

4-鋼材市場主要供應商的市場佔有率是多少?

5-進入鋼鐵市場的合適型態或策略手段是什麼?

目錄

第1章 前言

第2章調查方法

第3章執行摘要

第4章市場概況

第5章市場洞察

- 市場動態

- 促進因素

- 全球住宅投資增加

- 汽車業、能源電力業用鋼量增加

- 用於鋼鐵生產的鐵礦石和其他礦物的可用性

- 抑制因素

- 鋼材原料價格不穩定

- 機會

- 繼續向淨零鋼鐵過渡

- 新興國家增加鋼鐵投資和政府支持

- 任務

- 環境挑戰與鋼鐵產能過剩相關問題

- 促進因素

- 市場區隔分析

- 產品類型:由於鐵礦石的使用量增加

- 型態:能源領域擴大使用片材/板材來生產太陽能板

- 最終用戶產業:由於鋼材具有高強度和韌性,建設產業中鋼材的使用量不斷增加。

- 市場趨勢分析

- 高通膨的累積效應

- 波特五力分析

- 價值鍊和關鍵路徑分析

- 法律規範

第6章鋼鐵市場:依產品

- 鐵礦石

- 鋼

第7章鋼鐵市場:依型態

- 管/管

- 棒材/棒材

- 片材/板材

第8章鋼鐵市場:依最終用途產業

- 航太

- 車

- 建造

- 能源

- 機械設備

- 包裝

第9章 南北美洲鋼鐵市場

- 阿根廷

- 巴西

- 加拿大

- 墨西哥

- 美國

第10章亞太地區鋼鐵市場

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 菲律賓

- 新加坡

- 韓國

- 台灣

- 泰國

- 越南

第11章歐洲、中東和非洲鋼鐵市場

- 丹麥

- 埃及

- 芬蘭

- 法國

- 德國

- 以色列

- 義大利

- 荷蘭

- 奈及利亞

- 挪威

- 波蘭

- 卡達

- 俄羅斯

- 沙烏地阿拉伯

- 南非

- 西班牙

- 瑞典

- 瑞士

- 土耳其

- 阿拉伯聯合大公國

- 英國

第12章競爭形勢

- FPNV定位矩陣

- 市場佔有率分析:主要企業

- 主要企業競爭情境分析

- 併購

- 合約、合作和夥伴關係

第13章競爭產品組合

- 主要公司簡介

- ArcelorMittal SA

- Baoshan Iron & Steel Co., Ltd.

- China Ansteel Group Corporation Limited

- China Baowu Steel Group Corp., Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hesteel Group Company Limited

- Hyundai Steel Company

- Industrias CH

- JFE Steel Corporation

- Jindal Steel and Power Limited

- JSW Steel Limited

- Kobe Steel, Ltd.

- Mitsui & Co., Ltd.

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Sabre Steel Inc

- Salzgitter AG

- Shandong Iron and Steel Group Co., Ltd.

- SSAB AB

- Tata Steel Limited

- ThyssenKrupp AG

- United States Steel Corporation

- 主要產品系列

第14章附錄

- 討論指南

- 關於許可證和定價

[193 Pages Report] The Iron & Steel Market size was estimated at USD 1.70 trillion in 2023 and expected to reach USD 1.77 trillion in 2024, at a CAGR 4.31% to reach USD 2.29 trillion by 2030.

Global Iron & Steel Market

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2023] | USD 1.70 trillion |

| Estimated Year [2024] | USD 1.77 trillion |

| Forecast Year [2030] | USD 2.29 trillion |

| CAGR (%) | 4.31% |

The iron & steel market encompasses producing, distributing, and consuming metallic raw materials derived from iron ore and recycled scrap metal. These materials are fabricated into various end products across various industries, such as automotive, construction, aerospace, energy, packaging, and heavy machinery. The global iron and steel industry is highly competitive, with a diversified product portfolio of ferrous alloys, including carbon steel, alloy steel, stainless steel, cast iron, pig iron, wrought iron, and other specialty metals. Rapid global urbanization has increased demand for residential and commercial buildings, roads, bridges, and transportation infrastructure, which require significant steel products. Furthermore, the increasing steel consumption in the automotive and energy & power industries is leading to market growth. However, environmental concerns due to greenhouse gas emissions and price volatility affecting profitability across the value chain are impacting the iron & steel market. Increasing investment by the market players and government support for iron & steel in emerging economies. Moreover, adopting sustainability-focused initiatives such as hydrogen-based green steel production techniques and recycling-based circular economy models that reduce energy consumption and carbon emissions is an lucrative opportunity for the market.

Regional Insights

In the Americas, the US iron & steel industry has seen substantial growth following recent investments to modernize facilities and enhance production processes and Canada also contributes significantly to this region's steel output. Both countries share similar consumer needs and purchasing behaviors primarily driven by infrastructure development and automobile manufacturing sectors. In the EMEA region, Germany leads European crude steel production, followed by Italy, France, and Spain. The Middle East has experienced increasing demand for iron & steel due to rapid urbanization and growth in critical sectors such as construction, oil & gas, and transportation. In Africa, South Africa stands out as a major producer due to its well-developed mining sector that supplies raw materials for local production. In the Asia Pacific region, China dominates the iron & steel industry globally, with its massive population driving domestic demand for construction materials, automobiles, machinery, and appliances. Japan is known for its advanced technology employed in manufacturing high-quality steel. At the same time, India's increasing urbanization has led to significant investments in infrastructure projects that drive up demand for iron & steel products.

FPNV Positioning Matrix

The FPNV Positioning Matrix is pivotal in evaluating the Iron & Steel Market. It offers a comprehensive assessment of vendors, examining key metrics related to Business Strategy and Product Satisfaction. This in-depth analysis empowers users to make well-informed decisions aligned with their requirements. Based on the evaluation, the vendors are then categorized into four distinct quadrants representing varying levels of success: Forefront (F), Pathfinder (P), Niche (N), or Vital (V).

Market Share Analysis

The Market Share Analysis is a comprehensive tool that provides an insightful and in-depth examination of the current state of vendors in the Iron & Steel Market. By meticulously comparing and analyzing vendor contributions in terms of overall revenue, customer base, and other key metrics, we can offer companies a greater understanding of their performance and the challenges they face when competing for market share. Additionally, this analysis provides valuable insights into the competitive nature of the sector, including factors such as accumulation, fragmentation dominance, and amalgamation traits observed over the base year period studied. With this expanded level of detail, vendors can make more informed decisions and devise effective strategies to gain a competitive edge in the market.

Key Company Profiles

The report delves into recent significant developments in the Iron & Steel Market, highlighting leading vendors and their innovative profiles. These include ArcelorMittal S.A., Baoshan Iron & Steel Co., Ltd., China Ansteel Group Corporation Limited, China Baowu Steel Group Corp., Ltd., Cleveland-Cliffs Inc., Gerdau S/A, Hesteel Group Company Limited, Hyundai Steel Company, Industrias CH, JFE Steel Corporation, Jindal Steel and Power Limited, JSW Steel Limited, Kobe Steel, Ltd., Mitsui & Co., Ltd., Nippon Steel Corporation, Nucor Corporation, Outokumpu, POSCO, Sabre Steel Inc, Salzgitter AG, Shandong Iron and Steel Group Co., Ltd., SSAB AB, Tata Steel Limited, ThyssenKrupp AG, and United States Steel Corporation.

Market Segmentation & Coverage

This research report categorizes the Iron & Steel Market to forecast the revenues and analyze trends in each of the following sub-markets:

- Product

- Iron Ore

- Steel

- Form

- Pipes/Tubes

- Rods/Bars

- Sheets/Plates

- End-Use Industry

- Aerospace

- Automotive

- Construction

- Energy

- Machinery & Equipment

- Packaging

- Region

- Americas

- Argentina

- Brazil

- Canada

- Mexico

- United States

- California

- Florida

- Illinois

- New York

- Ohio

- Pennsylvania

- Texas

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Malaysia

- Philippines

- Singapore

- South Korea

- Taiwan

- Thailand

- Vietnam

- Europe, Middle East & Africa

- Denmark

- Egypt

- Finland

- France

- Germany

- Israel

- Italy

- Netherlands

- Nigeria

- Norway

- Poland

- Qatar

- Russia

- Saudi Arabia

- South Africa

- Spain

- Sweden

- Switzerland

- Turkey

- United Arab Emirates

- United Kingdom

- Americas

The report offers valuable insights on the following aspects:

1. Market Penetration: It presents comprehensive information on the market provided by key players.

2. Market Development: It delves deep into lucrative emerging markets and analyzes the penetration across mature market segments.

3. Market Diversification: It provides detailed information on new product launches, untapped geographic regions, recent developments, and investments.

4. Competitive Assessment & Intelligence: It conducts an exhaustive assessment of market shares, strategies, products, certifications, regulatory approvals, patent landscape, and manufacturing capabilities of the leading players.

5. Product Development & Innovation: It offers intelligent insights on future technologies, R&D activities, and breakthrough product developments.

The report addresses key questions such as:

1. What is the market size and forecast of the Iron & Steel Market?

2. Which products, segments, applications, and areas should one consider investing in over the forecast period in the Iron & Steel Market?

3. What are the technology trends and regulatory frameworks in the Iron & Steel Market?

4. What is the market share of the leading vendors in the Iron & Steel Market?

5. Which modes and strategic moves are suitable for entering the Iron & Steel Market?

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Limitations

- 1.7. Assumptions

- 1.8. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Iron & Steel Market, by Region

5. Market Insights

- 5.1. Market Dynamics

- 5.1.1. Drivers

- 5.1.1.1. Rising investment in residential construction worldwide

- 5.1.1.2. Increasing consumption of steel in automotive and energy & power industries

- 5.1.1.3. Availability of iron ore and other minerals for steel production

- 5.1.2. Restraints

- 5.1.2.1. Volatile prices of raw materials of iron & steel

- 5.1.3. Opportunities

- 5.1.3.1. Ongoing transition towards net zero steel

- 5.1.3.2. Increasing investment and government support for iron & steel in emerging economies

- 5.1.4. Challenges

- 5.1.4.1. Environmental challenges and problems associated with the excess capacity of iron & steel

- 5.1.1. Drivers

- 5.2. Market Segmentation Analysis

- 5.2.1. Product Type: Increasing use of iron ore owing to their high strength and durability

- 5.2.2. Form: Rising utilization of Sheets/Plates in energy sector for manufacturing solar panels

- 5.2.3. End-Users Industry: Increasing use of iron and steel in construction industry as it have high strength and and toughness

- 5.3. Market Trend Analysis

- 5.4. Cumulative Impact of High Inflation

- 5.5. Porter's Five Forces Analysis

- 5.5.1. Threat of New Entrants

- 5.5.2. Threat of Substitutes

- 5.5.3. Bargaining Power of Customers

- 5.5.4. Bargaining Power of Suppliers

- 5.5.5. Industry Rivalry

- 5.6. Value Chain & Critical Path Analysis

- 5.7. Regulatory Framework

6. Iron & Steel Market, by Product

- 6.1. Introduction

- 6.2. Iron Ore

- 6.3. Steel

7. Iron & Steel Market, by Form

- 7.1. Introduction

- 7.2. Pipes/Tubes

- 7.3. Rods/Bars

- 7.4. Sheets/Plates

8. Iron & Steel Market, by End-Use Industry

- 8.1. Introduction

- 8.2. Aerospace

- 8.3. Automotive

- 8.4. Construction

- 8.5. Energy

- 8.6. Machinery & Equipment

- 8.7. Packaging

9. Americas Iron & Steel Market

- 9.1. Introduction

- 9.2. Argentina

- 9.3. Brazil

- 9.4. Canada

- 9.5. Mexico

- 9.6. United States

10. Asia-Pacific Iron & Steel Market

- 10.1. Introduction

- 10.2. Australia

- 10.3. China

- 10.4. India

- 10.5. Indonesia

- 10.6. Japan

- 10.7. Malaysia

- 10.8. Philippines

- 10.9. Singapore

- 10.10. South Korea

- 10.11. Taiwan

- 10.12. Thailand

- 10.13. Vietnam

11. Europe, Middle East & Africa Iron & Steel Market

- 11.1. Introduction

- 11.2. Denmark

- 11.3. Egypt

- 11.4. Finland

- 11.5. France

- 11.6. Germany

- 11.7. Israel

- 11.8. Italy

- 11.9. Netherlands

- 11.10. Nigeria

- 11.11. Norway

- 11.12. Poland

- 11.13. Qatar

- 11.14. Russia

- 11.15. Saudi Arabia

- 11.16. South Africa

- 11.17. Spain

- 11.18. Sweden

- 11.19. Switzerland

- 11.20. Turkey

- 11.21. United Arab Emirates

- 11.22. United Kingdom

12. Competitive Landscape

- 12.1. FPNV Positioning Matrix

- 12.2. Market Share Analysis, By Key Player

- 12.3. Competitive Scenario Analysis, By Key Player

- 12.3.1. Merger & Acquisition

- 12.3.1.1. Tata Steel's 7 Subsidiary Companies to Be Merged with Parent Company in Current Financial Year

- 12.3.2. Agreement, Collaboration, & Partnership

- 12.3.2.1. Vale International to Supply Iron Ore to Essar's Steel Project in Saudi Arabia

- 12.3.2.2. Aramco, Baosteel and PIF Sign Agreement to Establish First Integrated Steel Plate Manufacturing Complex in Saudi Arabia

- 12.3.1. Merger & Acquisition

13. Competitive Portfolio

- 13.1. Key Company Profiles

- 13.1.1. ArcelorMittal S.A.

- 13.1.2. Baoshan Iron & Steel Co., Ltd.

- 13.1.3. China Ansteel Group Corporation Limited

- 13.1.4. China Baowu Steel Group Corp., Ltd.

- 13.1.5. Cleveland-Cliffs Inc.

- 13.1.6. Gerdau S/A

- 13.1.7. Hesteel Group Company Limited

- 13.1.8. Hyundai Steel Company

- 13.1.9. Industrias CH

- 13.1.10. JFE Steel Corporation

- 13.1.11. Jindal Steel and Power Limited

- 13.1.12. JSW Steel Limited

- 13.1.13. Kobe Steel, Ltd.

- 13.1.14. Mitsui & Co., Ltd.

- 13.1.15. Nippon Steel Corporation

- 13.1.16. Nucor Corporation

- 13.1.17. Outokumpu

- 13.1.18. POSCO

- 13.1.19. Sabre Steel Inc

- 13.1.20. Salzgitter AG

- 13.1.21. Shandong Iron and Steel Group Co., Ltd.

- 13.1.22. SSAB AB

- 13.1.23. Tata Steel Limited

- 13.1.24. ThyssenKrupp AG

- 13.1.25. United States Steel Corporation

- 13.2. Key Product Portfolio

14. Appendix

- 14.1. Discussion Guide

- 14.2. License & Pricing

LIST OF FIGURES

- FIGURE 1. IRON & STEEL MARKET RESEARCH PROCESS

- FIGURE 2. IRON & STEEL MARKET SIZE, 2023 VS 2030

- FIGURE 3. IRON & STEEL MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 4. IRON & STEEL MARKET SIZE, BY REGION, 2023 VS 2030 (%)

- FIGURE 5. IRON & STEEL MARKET SIZE, BY REGION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 6. IRON & STEEL MARKET DYNAMICS

- FIGURE 7. IRON & STEEL MARKET SIZE, BY PRODUCT, 2023 VS 2030 (%)

- FIGURE 8. IRON & STEEL MARKET SIZE, BY PRODUCT, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 9. IRON & STEEL MARKET SIZE, BY FORM, 2023 VS 2030 (%)

- FIGURE 10. IRON & STEEL MARKET SIZE, BY FORM, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 11. IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2023 VS 2030 (%)

- FIGURE 12. IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 13. AMERICAS IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 14. AMERICAS IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 15. UNITED STATES IRON & STEEL MARKET SIZE, BY STATE, 2023 VS 2030 (%)

- FIGURE 16. UNITED STATES IRON & STEEL MARKET SIZE, BY STATE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 17. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 18. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 19. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 20. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 21. IRON & STEEL MARKET, FPNV POSITIONING MATRIX, 2023

- FIGURE 22. IRON & STEEL MARKET SHARE, BY KEY PLAYER, 2023

LIST OF TABLES

- TABLE 1. IRON & STEEL MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2023

- TABLE 3. IRON & STEEL MARKET SIZE, 2018-2030 (USD MILLION)

- TABLE 4. GLOBAL IRON & STEEL MARKET SIZE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 5. IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 6. IRON & STEEL MARKET SIZE, BY IRON ORE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 7. IRON & STEEL MARKET SIZE, BY STEEL, BY REGION, 2018-2030 (USD MILLION)

- TABLE 8. IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 9. IRON & STEEL MARKET SIZE, BY PIPES/TUBES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 10. IRON & STEEL MARKET SIZE, BY RODS/BARS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 11. IRON & STEEL MARKET SIZE, BY SHEETS/PLATES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 12. IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 13. IRON & STEEL MARKET SIZE, BY AEROSPACE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 14. IRON & STEEL MARKET SIZE, BY AUTOMOTIVE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 15. IRON & STEEL MARKET SIZE, BY CONSTRUCTION, BY REGION, 2018-2030 (USD MILLION)

- TABLE 16. IRON & STEEL MARKET SIZE, BY ENERGY, BY REGION, 2018-2030 (USD MILLION)

- TABLE 17. IRON & STEEL MARKET SIZE, BY MACHINERY & EQUIPMENT, BY REGION, 2018-2030 (USD MILLION)

- TABLE 18. IRON & STEEL MARKET SIZE, BY PACKAGING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 19. AMERICAS IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 20. AMERICAS IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 21. AMERICAS IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 22. AMERICAS IRON & STEEL MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 23. ARGENTINA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 24. ARGENTINA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 25. ARGENTINA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 26. BRAZIL IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 27. BRAZIL IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 28. BRAZIL IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 29. CANADA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 30. CANADA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 31. CANADA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 32. MEXICO IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 33. MEXICO IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 34. MEXICO IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 35. UNITED STATES IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 36. UNITED STATES IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 37. UNITED STATES IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 38. UNITED STATES IRON & STEEL MARKET SIZE, BY STATE, 2018-2030 (USD MILLION)

- TABLE 39. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 40. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 41. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 42. ASIA-PACIFIC IRON & STEEL MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 43. AUSTRALIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 44. AUSTRALIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 45. AUSTRALIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 46. CHINA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 47. CHINA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 48. CHINA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 49. INDIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 50. INDIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 51. INDIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 52. INDONESIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 53. INDONESIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 54. INDONESIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 55. JAPAN IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 56. JAPAN IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 57. JAPAN IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 58. MALAYSIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 59. MALAYSIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 60. MALAYSIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 61. PHILIPPINES IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 62. PHILIPPINES IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 63. PHILIPPINES IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 64. SINGAPORE IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 65. SINGAPORE IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 66. SINGAPORE IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 67. SOUTH KOREA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 68. SOUTH KOREA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 69. SOUTH KOREA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 70. TAIWAN IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 71. TAIWAN IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 72. TAIWAN IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 73. THAILAND IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 74. THAILAND IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 75. THAILAND IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 76. VIETNAM IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 77. VIETNAM IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 78. VIETNAM IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 79. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 80. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 81. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 82. EUROPE, MIDDLE EAST & AFRICA IRON & STEEL MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 83. DENMARK IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 84. DENMARK IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 85. DENMARK IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 86. EGYPT IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 87. EGYPT IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 88. EGYPT IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 89. FINLAND IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 90. FINLAND IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 91. FINLAND IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 92. FRANCE IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 93. FRANCE IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 94. FRANCE IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 95. GERMANY IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 96. GERMANY IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 97. GERMANY IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 98. ISRAEL IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 99. ISRAEL IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 100. ISRAEL IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 101. ITALY IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 102. ITALY IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 103. ITALY IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 104. NETHERLANDS IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 105. NETHERLANDS IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 106. NETHERLANDS IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 107. NIGERIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 108. NIGERIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 109. NIGERIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 110. NORWAY IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 111. NORWAY IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 112. NORWAY IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 113. POLAND IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 114. POLAND IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 115. POLAND IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 116. QATAR IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 117. QATAR IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 118. QATAR IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 119. RUSSIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 120. RUSSIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 121. RUSSIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 122. SAUDI ARABIA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 123. SAUDI ARABIA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 124. SAUDI ARABIA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 125. SOUTH AFRICA IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 126. SOUTH AFRICA IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 127. SOUTH AFRICA IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 128. SPAIN IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 129. SPAIN IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 130. SPAIN IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 131. SWEDEN IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 132. SWEDEN IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 133. SWEDEN IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 134. SWITZERLAND IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 135. SWITZERLAND IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 136. SWITZERLAND IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 137. TURKEY IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 138. TURKEY IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 139. TURKEY IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 140. UNITED ARAB EMIRATES IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 141. UNITED ARAB EMIRATES IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 142. UNITED ARAB EMIRATES IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 143. UNITED KINGDOM IRON & STEEL MARKET SIZE, BY PRODUCT, 2018-2030 (USD MILLION)

- TABLE 144. UNITED KINGDOM IRON & STEEL MARKET SIZE, BY FORM, 2018-2030 (USD MILLION)

- TABLE 145. UNITED KINGDOM IRON & STEEL MARKET SIZE, BY END-USE INDUSTRY, 2018-2030 (USD MILLION)

- TABLE 146. IRON & STEEL MARKET, FPNV POSITIONING MATRIX, 2023

- TABLE 147. IRON & STEEL MARKET SHARE, BY KEY PLAYER, 2023

- TABLE 148. IRON & STEEL MARKET LICENSE & PRICING