|

市場調查報告書

商品編碼

1435922

聚合物太陽能電池:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Polymer Solar Cells - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

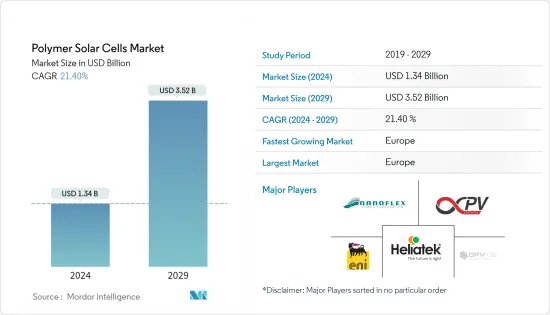

聚合物太陽能電池市場規模預計到2024年為13.4億美元,預計到2029年將達到35.2億美元,在預測期內(2024-2029年)成長21.40%,複合年成長率成長。

主要亮點

- 從長遠來看,旨在提高轉換效率的聚合物太陽能電池技術的進步預計將在預測期內推動市場發展。

- 相反,與矽太陽能電池相比,聚合物太陽能電池的效率較低,預計將阻礙預測期內的市場成長。

- 儘管如此,在預測期內,有關開發具有更高轉換效率的新型聚合物的研究和開發預計將成為市場的重大成長機會。

聚合物太陽能電池市場趨勢

市場驅動的技術進步

- 聚合物太陽能電池,也稱為有機光伏電池(OPV),是使用有機聚合物層將光轉化為電能的第三代光伏電池。聚合物太陽能電池重量輕、彈性、可客製化,且對環境的負面影響較小。

- 2022年,全球太陽能光電技術總裝置容量約為1046.61吉瓦,較2017年的390.87吉瓦成長近167.7%。隨著近年來光伏技術的快速進步,聚合物太陽能電池在2022年的效率將達到18.42%。實驗室情況。為了進一步提高效率,具有不同分子結構的各種組織正在深入研究,並預計在不久的將來滲透到太陽能市場。

- 儘管聚合物太陽能電池比矽太陽能電池具有重量輕、成本低、透明、壽命長(超過5000小時)等多項優勢,但其低能量轉換使得高效的商業應用非常有限。

- Solarmer Energy Inc.表示,由於技術進步,目前聚合物太陽能電池的效率預計將隨著時間的推移而提高,技術進步提供了高效的聚合物分子結構,使聚合物太陽能電池能夠取代矽基太陽能電池,預計這將提高市場競爭力。和其他替代太陽能電池技術將在預測期內推動市場。

歐洲可能主導市場

- 歐洲是太陽能發電技術最大的市場之一,截至2022年太陽能發電裝置容量約225.47GW,高於2017年的109.98GW。隨著技術的進步,該地區正在進行各種研究計劃,以使太陽能電池板更便宜、更靈活。可以附著在多個表面上。

- Heliatek GmbH 和 OPVIUS GmbH 等公司正在開發聚合物太陽能電池,並已在該地區展示了多個計劃。

- 最大的聚合物或有機太陽能電池計劃發生在法國。這稱為 BiOPV(有機建築整合太陽能)。該計劃包括在屋頂安裝約500平方公尺的有機太陽能發電裝置,發電量約23.8兆瓦時。

- 截至 2023 年,該地區還有其他幾個研發計劃正在進行中。 2023 年 10 月,法國和西班牙的調查團隊利用高通量射出成型技術開發了一種嵌入塑膠組件中的有機光伏模組。研究人員將熱塑性聚氨酯注入模組中,發現它提高了機械穩定性,同時保持了高彈性。研究人員首先使用稱為 P3HT:O-IDTBR 的光活性混合物透過卷軸式印刷創建了該模組。選擇這種混合物是考慮到型態與後續射出成型過程相關的形態和熱穩定性。預計在預測期內完成各個領域和應用的研發將擴大該地區的市場。

聚合物太陽能電池產業概況

聚合物太陽能電池市場將整合。市場主要企業包括(排名不分先後)Eni SpA、NanoFlex Power Corporation、Infinity PV、OPVIUS GmbH、Heliatek GmbH 等。

埃尼研究開發的技術擴大了整合太陽能發電的範圍。鈣鈦礦電池與有機太陽能電池一起可以用半透明薄膜製造,從而降低材料成本和生產技術,使傳統太陽能電池以前不可能實現的應用成為可能,例如嵌入建築物建築幕牆。除此之外,最近國際和歐盟在建築能源效率領域的指令促進了這項應用。因此,預計會有廣泛的應用。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查範圍

- 市場定義

- 調查先決條件

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 北美洲

第6章 競爭形勢

- 併購、合資、合作與協議

- 主要企業採取的策略

- 公司簡介

- Solarmer Energy Inc.

- NanoFlex Power Corporation

- Infinity PV

- OPVIUS GmbH

- Heliatek GmbH

- Eni SpA

第7章市場機會與未來趨勢

The Polymer Solar Cells Market size is estimated at USD 1.34 billion in 2024, and is expected to reach USD 3.52 billion by 2029, growing at a CAGR of 21.40% during the forecast period (2024-2029).

Key Highlights

- Over the long term, technological advancements in polymer solar cell technology aimed at increasing conversion efficiency are expected to drive the market during the forecast period.

- On the flip side, the lower efficiency of polymer solar cells as compared to silicon solar cells is expected to hinder market growth during the forecasting period.

- Nevertheless, research and development into the development of new polymers with higher conversion efficiencies is expected to be a significant growth opportunity for the market beyond the forecast period.

Polymer Solar Cells Market Trends

Technological Advancements to Drive the Market

- Polymer solar cells, also called organic photovoltaic (OPV), are third-generation PV cells that use an organic polymer layer to convert light into electricity. Polymer solar cells are lightweight, flexible, customizable, and have a less adverse environmental impact.

- In 2022, global solar PV technology had a total installed capacity of around 1046.61 GW, growing by nearly 167.7% from 390.87 GW in 2017. With rapid improvements in PV technology in recent years, polymer solar cells achieved an efficiency of 18.42% in 2022 under lab conditions. In order to further increase efficiency, various organizations with different molecular structures are performing intensive research and are expected to penetrate the solar PV market in the near future.

- Polymer solar cells have a few advantages over silicon solar cells, like being lighter in weight, cheaper in cost, transparent, and having a longer lifetime (greater than 5000 hrs), but due to their low energy conversion, efficient commercial applications are very limited.

- As per Solarmer Energy Inc., the present efficiency of polymer solar cells is estimated to improve over time due to technological improvement, which is expected to provide efficient polymer molecular structure and make polymer solar cells more competitive in the market with silicon-based solar cells and other alternative solar cell technologies, driving the market during the forecast period.

Europe is Likely to Dominate the Market

- Europe was one of the largest markets for solar PV technology, with around 225.47 GW of solar PV installations as of 2022, up from 109.98 GW in 2017. With technological advancements, the region is doing various research projects to achieve cheaper and more flexible solar panels that can be installed on multiple surfaces.

- Companies like Heliatek GmbH and OPVIUS GmbH are developing polymer solar cells and have demonstrated a few projects in the region.

- The largest polymer or organic solar cell project was in France. It is called the BiOPV (Building Integrated Organic Photovoltaic). The project includes the installation of organic photovoltaics on the roof of around 500 square meters that generate nearly 23.8 MWh of electricity.

- As of 2023, a few other R&D projects were going on in the region. In October 2023, a French-Spanish research team developed organic photovoltaic modules embedded into plastic parts through high throughput injection molding. The researchers injected thermoplastic polyurethane into the modules and found it enhanced their mechanical stability while keeping a high flexibility. The researchers first created modules in roll-to-roll printing using a photoactive blend known as P3HT: O-IDTBR. This blend was chosen due to its morphological and thermal stability, which are relevant to the later injection molding process. The completion of R&D in various sectors and applications is expected to expand the market in the region during the forecast period.

Polymer Solar Cells Industry Overview

The polymer solar cells market is consolidated. Some of the key players in the market (in no particular order) include Eni SpA, NanoFlex Power Corporation, Infinity PV, OPVIUS GmbH, and Heliatek GmbH, among others.

Eni's research developed a technology that widens the horizons of integrated photovoltaics. Together with organic photovoltaic cells, perovskite cells can be made in semi-transparent thin film with reduced material costs and production techniques, enabling applications that have hitherto been impossible for conventional solar cells, such as embedding on building facades. Among other things, this application is promoted by recent international and EU directives in the area of energy efficiency for buildings. It is, therefore, destined to have an extensive range of uses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecasts in USD million, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Mexico

- 5.1.2 Europe

- 5.1.2.1 Germany

- 5.1.2.2 France

- 5.1.2.3 United Kingdom

- 5.1.2.4 Rest of Europe

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 India

- 5.1.3.3 Japan

- 5.1.3.4 South Korea

- 5.1.3.5 Rest of Asia-Pacific

- 5.1.4 South America

- 5.1.4.1 Brazil

- 5.1.4.2 Argentina

- 5.1.4.3 Rest of South America

- 5.1.5 Middle-East and Africa

- 5.1.5.1 Saudi Arabia

- 5.1.5.2 United Arab Emirates

- 5.1.5.3 South Africa

- 5.1.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Solarmer Energy Inc.

- 6.3.2 NanoFlex Power Corporation

- 6.3.3 Infinity PV

- 6.3.4 OPVIUS GmbH

- 6.3.5 Heliatek GmbH

- 6.3.6 Eni SpA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年碲化鎘全球市場報告

2024 年碲化鎘全球市場報告 衛星太陽能電池材料的全球市場:材料類型(矽、銅銦鎵硒、砷化鎵)、應用、軌道和地區 - 預測(截至 2030 年)

衛星太陽能電池材料的全球市場:材料類型(矽、銅銦鎵硒、砷化鎵)、應用、軌道和地區 - 預測(截至 2030 年) 歐洲TOPCon太陽能電池市場:分析與預測(2023-2032)

歐洲TOPCon太陽能電池市場:分析與預測(2023-2032) 全球奈米複合太陽能電池市場評估:按類型、材料類型、應用、地區、機會、預測(2017-2031)

全球奈米複合太陽能電池市場評估:按類型、材料類型、應用、地區、機會、預測(2017-2031) 太陽能電池市場:按類型、技術、應用分類 - 2024-2030 年全球預測

太陽能電池市場:按類型、技術、應用分類 - 2024-2030 年全球預測 新一代太陽能電池市場:按材料、部署和最終用途分類 - 2024-2030 年全球預測

新一代太陽能電池市場:按材料、部署和最終用途分類 - 2024-2030 年全球預測 軟性太陽能電池的成長機會

軟性太陽能電池的成長機會 單晶太陽能電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按電網類型、按應用、安裝、技術、地區和競爭細分

單晶太陽能電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按電網類型、按應用、安裝、技術、地區和競爭細分 生物混合太陽能電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按材料、按應用、地區和競爭細分

生物混合太陽能電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按材料、按應用、地區和競爭細分 拓普康太陽能電池市場,按類型、安裝、最終用戶、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

拓普康太陽能電池市場,按類型、安裝、最終用戶、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測