|

市場調查報告書

商品編碼

1435780

礬土:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Bauxite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

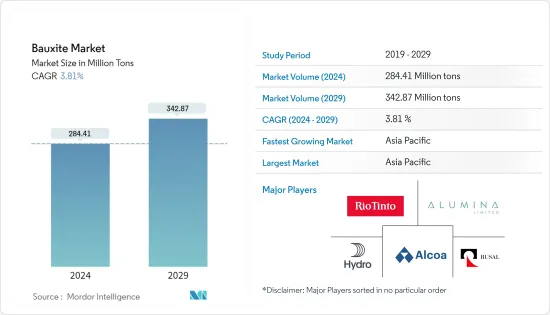

預計2024年礬土市場規模為28,441萬噸,預估至2029年將達3,4,287萬噸,預測期(2024-2029年)複合年成長率為3.81%。

主要亮點

- 2020年,市場受到冠狀病毒感染疾病(COVID-19)爆發的負面影響,導致世界各地國家封鎖,擾亂製造活動和供應鏈,並導致生產停頓。然而,到了2021年,情況開始好轉,市場恢復了成長軌跡。

- 從中期來看,推動所研究市場的主要因素是其在水泥行業中的使用加速以及氧化鋁在工業應用中的持續使用。

- 與礬土開採相關的環境問題預計將阻礙未來幾年的市場成長。

- 來自中國的耐火材料和磨料以及扁平礬土生產等商業應用的需求不斷增加,預計將為所研究的市場帶來機會。

- 亞太地區主導全球礬土市場,預計未來幾年將實現最快的成長。

礬土市場趨勢

冶金應用中對氧化鋁的需求不斷增加

- 礬土是一種含有大量鋁的沉積岩。它是鋁和鎵的主要來源,主要由三水鋁石、水鋁石和水鋁石等鋁礦物組成。

- 由於其氧化鋁含量高,礬土是氧化鋁生產的主要來源,然後加工成最終產品和氧化鋁生產。因此,增加氧化鋁產量正在推動所研究的市場。

- 氧化鋁因其密度低、無毒、導熱率高、耐腐蝕好、易於鑄造、機械加工和成型等各種優異性能而受到廣泛需求。氧化鋁產量的增加預計將在未來幾年推動礬土市場。

- 氧化鋁用於主要工業用途。除了製造鋁外,它還用於製造火星塞絕緣體和金屬塗料,以及作為固體火箭助推器的燃料成分。

- 此外,氧化鋁也用於製造量子乾涉裝置、電子電晶體等超導性元件。氧化鋁或氧化鋁也用作輻射防護的劑量計。

- 根據美國地質調查局估計,全球礬土資源量估計為550億至750億噸,足以滿足世界未來對金屬的需求。

- 根據美國人口普查局的數據,2022 年採礦和採石業收益總計 143.9 億美元,而 2021 年為 136.8 億美元。預計 2023 年該產業收益將達到 152.5 億美元。

- 美國地質調查局公佈的資料顯示,礬土和氧化鋁產量從 27.9 億噸大幅增加。

- 採礦和冶金是該國的主要工業。加拿大向世界各國供應 60 多種金屬和礦物。採礦業正在投資創新和新技術,這些技術正在迅速再形成該行業。採礦業也出現了整合,引發了對該行業未來幾年成長前景的猜測。

- 因此,由於上述所有因素,冶金用氧化鋁需求的增加預計將在預測期內推動調查市場的需求。

亞太地區主導市場

- 預計亞太地區將在預測期內主導礬土市場。中國、澳洲和印度等國家的快速工業化以及鋁在建築、建築、鋁箔和包裝等各個行業的使用不斷增加,繼續增加了該地區對礬土的需求。

- 此外,鋁的耐腐蝕、高延展性、高強度和輕重量等優越性能正在增加鋁在輕型汽車零件製造中的採用,推動該地區礬土市場的發展。

- 此外,礬土熔點高,用作耐火材料產品的原料,使其在該地區的需求量很大。耐火級礬土用於製造電弧鋼爐和高爐爐頂的磚。

- 礬土還可以透過與石灰石混合來製造水泥。生產的水泥氧化鋁含量高,以其快速沉降時間和強度而聞名,導致該地區對礬土的需求增加。

- 電動車的成長趨勢可能會進一步增加對鋁合金的需求。中國政府預計,到2025年,電動車產量的普及將達到20%。這反映在該國的電動車銷售趨勢上,2022年電動車銷量創下歷史新高。根據中國小客車協會統計,中國電動車銷量創歷史新高。 2022 年,電動車和插電式汽車銷量將達到 567 萬輛,幾乎是 2021 年銷量的兩倍。

- 由於100%外商直接投資(FDI)、無需工業許可證、以及從手動生產流程到自動化生產流程的技術改造等政府優惠政策,國內電子製造業正穩步擴張。印度針對國內電子產品製造推出了修改獎勵特別配套計畫 (M-SIPS) 和電子發展基金 (EDF) 等新獎勵,預算為 1.14 億美元。

- 市場上一些因亞太企業發展而受到調查的主要製造商包括氧化鋁有限公司、澳洲鋁土礦有限公司和力拓集團。

- 因此,上述因素可能會增加預測期內該地區礬土的需求。

礬土業概況

礬土市場本質上是部分一體化的,主要企業佔據了全球市場的重要佔有率。市場主要企業包括(排名不分先後)力拓、俄羅斯鋁業、美國鋁業公司、氧化鋁有限公司、挪威海德魯公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 繼續使用工業應用中的氧化鋁

- 水泥業加速使用

- 其他司機

- 抑制因素

- 與礬土開採相關的環境問題

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 生產分析

第5章市場區隔(市場規模:基於數量)

- 目的

- 冶金用氧化鋁

- 水泥

- 耐火材料

- 研磨材料

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Alcoa Corporation

- Alumina Limited

- Aluminum Corporation of China Limited

- Australian Bauxite Limited

- Compagnie des Bauxites de Guinee(CBG)

- GRAFIT MADENCILIK SAN. TIC. AS

- Iranian Aluminium Co.

- LKAB Minerals

- Norsk Hydro ASA

- Possehl Erzkontor GmbH & Co. KG

- Queensland Alumina Limited

- Rio Tinto

- RusAL

- Vimetco NV

- YunXiang Develop Co.,Limited

第7章 市場機會及未來趨勢

簡介目錄

Product Code: 69277

The Bauxite Market size is estimated at 284.41 Million tons in 2024, and is expected to reach 342.87 Million tons by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Key Highlights

- The market experienced negative impacts in 2020 due to the COVID-19 outbreak, which led to nationwide lockdowns worldwide, disruptions in manufacturing activities and supply chains, and production halts. However, in 2021, the conditions began to recover, restoring the growth trajectory of the market.

- In the medium term, the major factors driving the market studied are accelerating usage in the cement industries and continuous usage of alumina from industrial applications.

- Environmental concerns related to bauxite mining are expected to hinder market growth in the coming years.

- Increasing demand from commercial applications such as refractories and abrasives and leveling off of bauxite production from China is expected to act as an opportunity for the market studied.

- Asia-Pacific dominated the global bauxite market and is also expected to register the fastest growth in the years to come.

Bauxite Market Trends

Increasing Demand of Alumina for Metallurgical Purposes

- Bauxite is a sedimentary rock having a high content of aluminum. It is the main source of aluminum & gallium and consists mostly of aluminum minerals, namely gibbsite, boehmite, and diaspore.

- Because of its high alumina content, bauxite is a primary source for alumina production, which is then processed to produce finished products and alumina production. Thus rising alumina production is driving the market studied.

- The demand for alumina is increasing owing to its various superior properties such as low density, non-toxic nature, high thermal conductivity, excellent corrosion resistivity, and its ability to be easily cast, machined, and formed. Rising alumina production is expected to drive the market for bauxite through the upcoming years.

- Alumina is used for key industrial purposes. Other than producing aluminum, it is used for the production of spark plug insulators and metallic paints, and it is used as a fuel component for solid rocket boosters.

- Furthermore, alumina is used for the fabrication of superconducting devices, such as quantum interference devices and electron transistors. Aluminum oxide or alumina is also used as a dosimeter for radiation protection.

- According to a US Geological survey, global resources of bauxite are estimated to be between 55 billion and 75 billion tons and are sufficient to meet world demand for metal well into the future.

- As per the United States Census Bureau, revenue in mining and quarrying amounted to USD 14.39 billion in 2022, as compared to USD 13.68 billion in 2021. The revenue from this sector is projected to amount to USD 15.25 billion in 2023.

- As per data published by the United States Geological Survey, the bauxite and alumina increased significantly from 2790 million metric tons.

- Mining and metallurgy are key industries in the country. Canada supplies over 60 metals and minerals to different countries worldwide. The mining industry invests in innovation and new technologies, which rapidly reshapes the sector. The mining industry also witnessed consolidations, which led to speculations regarding the growth prospects for the industry in the coming years.

- Therefore, owing to all the above-mentioned factors, increasing demand for alumina for metallurgical purposes is expected to boost the demand for the market studied over the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market for bauxite during the forecast period. In countries such as China, Australia, and India, owing to rapid industrialization and an increase in the usage of aluminum in various industries, such as building and construction, foil, and packaging, the demand for bauxite continues to increase in the region.

- Furthermore, superior properties of aluminum, like corrosion resistance, high ductility, high strength, and lightweight, have led to an increase in the adoption of aluminum for producing light vehicle parts, which is propelling the bauxite market in the region.

- Additionally, demand for bauxite is rising in the region due to its usage as a raw material in making refractory products since it has a high melting point. Refractory grade bauxite is used to manufacture bricks to line the roof of electric arc steel-making furnaces and blast furnaces.

- Bauxite is also used for manufacturing cement by mixing it with limestone. The cement produced has high alumina content and is known for its rapid settling time and strength, leading to an increasing demand for bauxite in the region.

- The increasing trend of electric vehicles may further propel the demand for aluminum alloys. The government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went record-breaking high in 2022. As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, touching almost double the sales figures achieved in 2021.

- The domestic electronics manufacturing sector has been expanding at a steady rate, owing to favorable government policies, such as 100% Foreign Direct Investment (FDI), no requirement for an industrial license, and the technological transformation from manual to automatic production processes. New incentives, such as the Modified Incentive Special Package Scheme (M-SIPS) and Electronics Development Fund (EDF), have been started in the country with a budget of USD 114 million for the domestic manufacturing of electronics in India.

- Some of the major manufacturers of the market studied operating in Asia-Pacific include Alumina Limited, Australian Bauxite Limited, and Rio Tinto.

- Therefore, the aforementioned factors are likely to boost the demand for bauxite in the region during the forecast period.

Bauxite Industry Overview

The bauxite market is partially consolidated in nature, with top players accounting for a significant share of the global market. Some of the major companies in the market include Rio Tinto, RusAL, Alcoa Corporation, Alumina Limited, and Norsk Hydro ASA, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Continuous Usage of Alumina from Industrial Applications

- 4.1.2 Accelerating Usage in the Cement Industries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Environmental Concern Related to Bauxite Mining

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Production Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Alumina for Metallurgical Purposes

- 5.1.2 Cement

- 5.1.3 Refractories

- 5.1.4 Abrasives

- 5.1.5 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Australia and New Zealand

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Russia

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alcoa Corporation

- 6.4.2 Alumina Limited

- 6.4.3 Aluminum Corporation of China Limited

- 6.4.4 Australian Bauxite Limited

- 6.4.5 Compagnie des Bauxites de Guinee (CBG)

- 6.4.6 GRAFIT MADENCILIK SAN. TIC. A.S.

- 6.4.7 Iranian Aluminium Co.

- 6.4.8 LKAB Minerals

- 6.4.9 Norsk Hydro ASA

- 6.4.10 Possehl Erzkontor GmbH & Co. KG

- 6.4.11 Queensland Alumina Limited

- 6.4.12 Rio Tinto

- 6.4.13 RusAL

- 6.4.14 Vimetco NV

- 6.4.15 YunXiang Develop Co.,Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand from Commercial Applications such as Refractories and Abrasives

- 7.2 Levelling Off of Bauxite Production from China

02-2729-4219

+886-2-2729-4219

全球鋁土礦市場 - 2023-2030

全球鋁土礦市場 - 2023-2030 鋁土礦開採市場:按等級、按應用分類:2023-2032 年全球機會分析與產業預測

鋁土礦開採市場:按等級、按應用分類:2023-2032 年全球機會分析與產業預測 礬土的全球市場分析:各廠房生產能力,生產量,運用效率,需求與供給,等級,終端用戶產業,銷售管道,地區需求,企業佔有率(2015年~2035年)

礬土的全球市場分析:各廠房生產能力,生產量,運用效率,需求與供給,等級,終端用戶產業,銷售管道,地區需求,企業佔有率(2015年~2035年) 礬土的全球市場 - 產業分析,規模,佔有率,成長,趨勢,預測(2023年~2030年)

礬土的全球市場 - 產業分析,規模,佔有率,成長,趨勢,預測(2023年~2030年) 鋁土礦市場:按產品(冶金級、耐火級)、用途(氧化鋁生產、水泥、耐火材料)- 2023-2030 年全球預測

鋁土礦市場:按產品(冶金級、耐火級)、用途(氧化鋁生產、水泥、耐火材料)- 2023-2030 年全球預測 礬土礦業的全球市場 (2022-2026年):蘊藏量、生產量、資產、計劃、需求促進因素、主要企業、預測

礬土礦業的全球市場 (2022-2026年):蘊藏量、生產量、資產、計劃、需求促進因素、主要企業、預測 礬土的全球市場

礬土的全球市場 東南亞的礬土產業的分析 (2023年~2032年)

東南亞的礬土產業的分析 (2023年~2032年) 礬土骨材的全球市場調查報告-產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測

礬土骨材的全球市場調查報告-產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測 耐火材料等級礬土的全球市場、美國市場的預測:2022年~2028年

耐火材料等級礬土的全球市場、美國市場的預測:2022年~2028年

▼