|

市場調查報告書

商品編碼

1273333

粉煤灰市場 - 增長、趨勢和預測 (2023-2028)Fly Ash Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

預計在預測期內,飛灰市場的複合年增長率將超過 4%。

主要亮點

- 由於 2020 年 COVID-19 爆發導致飛灰需求減少,市場受到負面影響,幾乎所有主要最終用戶行業都暫時停止了生產。 然而,2021年,隨著各地建築業穩步增長,對粉煤灰的需求增加,促進了市場的增長。

- 市場受到建築行業不斷增長的需求以及促進粉煤灰使用的政府政策不斷增加的推動。 另一方面,粉煤灰的有害特性和對寒冷氣候的不適應阻礙了市場增長。

- 由於建築業的快速發展,粉煤灰市場也在增長。 當與石灰和水混合時,飛灰會形成一種類似波特蘭水泥的化合物。 對廢物處理和預製混凝土產品的需求增加對製造商來說是一個機會,促進了市場的增長。

- 預計亞太地區將主導市場,印度和中國等國家/地區的消費量最大。

粉煤灰市場趨勢

建築業需求增加

- 人口增長、工業化進程加快和生活水平提高正在推動建築行業對粉煤灰的需求。 粉煤灰用於建造堤壩和碾壓混凝土壩。 飛灰因其抗滲性和強度而被用作可流動和結構填料中的填料。 在鋪設柏油馬路時,它也用作填充劑來填充空隙。

- 全球建築業正在興起,創造了對粉煤灰的需求。 亞太地區正以世界上最快的複合年增長率增長,其次是北美,因為飛灰的二氧化碳排放量低且對環境友好,因此世界各國政府都在推廣使用飛灰。 歐洲是世界第三大粉煤灰市場。

- 高速公路和高速公路大型項目的興建增加了對粉煤灰的需求。 世界各國政府都在資助建築業。 例如,2022 年 2 月,法國政府與中國合作在全球建設了七大基礎設施項目。 兩國簽署《第四輪中法第三方市場合作試點項目清單》。 根據該協議,兩國同意投資各種基礎設施項目。

- 根據美國建築師協會 (AIA) 的數據,2022 年建築物的建築支出增長了 9% 以上。 預計 2023 年將再增長 6%。 據 Statista 估計,2022 年建築業預計將達到 8.2 萬億美元,2029 年將達到 17 萬億美元。

- 此外,中國的建築行業正在經歷巨大的增長。 根據國家統計局(NBS)的數據,2021 年,中國建築業產值將達到 4.5 萬億美元左右。 在美國,建築業受到有利的經濟條件、增加的就業機會以及政府對促進建築業發展的承諾的支持。 在美國,超過 50% 的混凝土是使用粉煤灰製造的。

- 由於這些因素,預計建築行業對粉煤灰的需求在預測期內將快速增長。

亞太地區主導市場

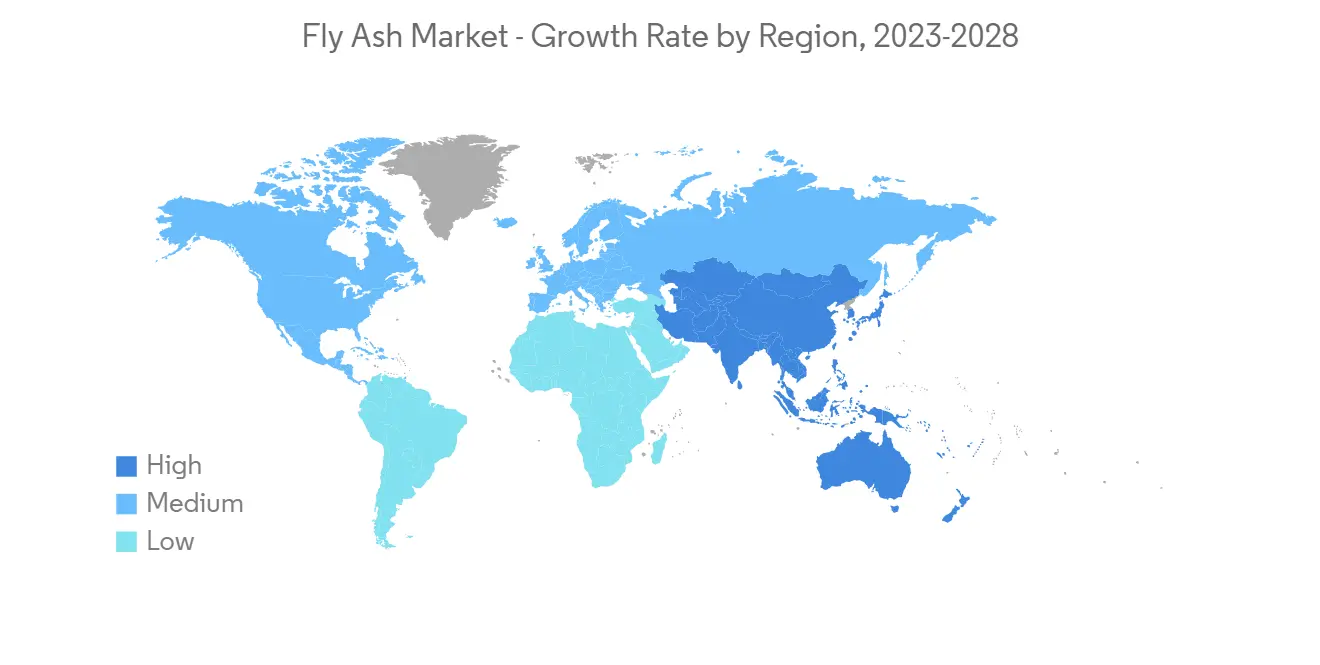

- 由於中國、印度和日本等國家/地區的需求不斷增加,預計亞太地區將成為預測期內規模最大、增長最快的地區。

- 隨著各國政府強調飛灰消費的生態原因,對飛灰的需求正在增加。 與不含飛灰的混合物相比,使用飛灰可使類似混合物的水灰比更低。 馬來西亞、印度尼西亞、中國和印度等政府正在增加對粉煤灰基礎設施的投資。 粉煤灰具有低滲透性和低二氧化碳排放量,有助於減少排放。

- 在到 2025 年的未來五年內,中國將在重大建設項目上投資 1.43 萬億美元。 根據國家發改委的數據,上海計劃在未來三年內投資 387 億美元,而廣州則簽署 16 個新的基礎設施項目,投資 80.9 億美元。。

- 2022 年,印度通過政府在基礎設施和經濟適用房方面的舉措(例如全民住房和智慧城市計劃)為建築業貢獻了約 6400 億美元。 該國建築活動的增加可能會推動對矽的需求,進而在預測期內推動氯甲烷市場。

- 在農業領域,飛灰用於穩定土壤,約佔飛灰市場的 14%。 採礦業正在尋找替代裝載材料,飛灰是一種經過驗證的替代材料,因為它可以減少大約 50% 的用水量。 亞太地區約佔全球採礦項目的38%,這增加了對粉煤灰的需求。

- 飛灰還用於水處理,降低總溶解固體 (TDS)、總懸浮固體 (TSS) 和水的 PH 值以淨化水,因此該地區對飛灰的需求正在促進

- 該地區的主要參與者包括 Boral Limited 和 Ashtech (India) Pvt Ltd。

- 上述因素以及政府的支持促成了粉煤灰市場需求的增加。

粉煤灰行業概況

粉煤灰市場較為分散,主要參與者佔據的市場份額很小。 市場上的公司包括 Boral、Cemex SAB de CV、Charah Solutions Inc.、Separation Technologies LLC 和 Cement Australia。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第 1 章介紹

- 調查先決條件

- 本次調查的範圍

第 2 章研究方法論

第 3 章執行摘要

第 4 章市場動態

- 促進因素

- 建築行業的需求增加

- 促進粉煤灰使用的政府政策

- 抑制因素

- 粉煤灰的有害特性

- 在寒冷氣候下不相容

- 工業價值鏈分析

- 波特的五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章市場細分(基於價值的市場規模)

- 類型

- F級

- C級

- 用途

- 建築

- 磚塊

- 道路建設

- 波特蘭水泥、混凝土

- 農業

- 礦業

- 水處理

- 其他用途

- 建築

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 意大利

- 法國

- 其他歐洲

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙特阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第 6 章競爭格局

- 併購、合資企業、合作、合同

- 市場份額分析**/排名分析

- 主要公司採用的策略

- 公司簡介

- Ashtech Industries

- Boral Resources

- Charah Solutions,Inc

- Cemex SAB de CV

- Cement Australia

- LafargeHolcim

- Salt River Materials Group

- Seperation Technologies LLC

- Suyog Suppliers

- Waste Management

第 7 章市場機會與未來趨勢

- 由於廢物處理和預製混凝土產品的需求增加

簡介目錄

Product Code: 68701

The fly ash market is estimated to register a CAGR of over 4% during the forecast period.

Key Highlights

- The market was negatively impacted by COVID-19 in 2020, as almost all the major end-user industries halted their production temporarily, leading to a decrease in demand for fly ash. However, the construction industry experienced steady growth in 2021 across all regions, which increased the demand for fly ash and helped the market to grow.

- Increasing demand from the construction industry and increasing government policies to promote the usage of fly ash are driving the market. On the flip side, the harmful properties of fly ash and its non-suitability in cold weather conditions are hindering market growth.

- The fly ash market has been growing due to the construction industry's rapid growth. When mixed with lime and water, fly ash forms a compound like Portland cement. Rising demand from waste management and precast concrete products is an opportunity for the manufacturers and helps the market's growth.

- The Asia-Pacific region is expected to dominate the market, with the largest consumption being registered in countries like India and China.

Fly Ash Market Trends

Increasing Demand from the Construction Industry

- Growing population, increasing industrialization, and living standards have driven the demand for fly ash in the construction industry. Fly ash is used for the construction of embankments and roller-compacted concrete dams. Fly ash is used as a filler in flowable and structural fills as it gives impermeability and more strength. It is also used as a filler material in asphalt road laying to fill voids.

- Globally the construction industry is increasing, generating demand for fly ash. Asia-Pacific region is growing at the fastest CAGR across the globe, followed by North America due to the promotion of fly ash by governments of various countries as it releases less carbon dioxide and is eco-friendly. Europe has the world's third-largest fly ash market.

- The emerging mega projects of expressways and highways have increased the demand for fly ash. Governments of various countries are funding the construction industry. For instance, in February 2022, France government partnered with China to build seven key infrastructure projects globally. Both countries signed the Fourth Round China-France Third-Party Market Cooperation Pilot Project List. Under the agreement, the two countries have agreed to invest in various infrastructure projects.

- According to the American Institute of Architects (AIA), construction spending on buildings increased by over 9% in 2022. It is estimated to increase further by 6% in 2023. According to the estimation by Statista, the construction industry size amounted to USD 8.2 trillion in 2022 and is expected to reach USD 17 trillion by 2029.

- Furthermore, China is experiencing massive growth in its construction sector. According to the National Bureau of Statistics (NBS), in 2021, the construction output in China was valued at approximately USD 4.5 trillion. In the United States, the construction industry is backed by good economic conditions, increasing job opportunities, and the government's commitment to boosting the construction industry. More than 50% of the concrete in the United States is manufactured using fly ash.

- Owing to the aforementioned factors, the demand for fly ash from the construction industry is projected to grow at a rapid rate during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is forecasted to be the largest and the fastest-growing region over the forecast period owing to the increasing demand from countries such as China, India, and Japan.

- The demand for fly ash is increasing because various governments have emphasized ecological reasons for the consumption of fly ash. The usage of fly ash allows for a low water-cement ratio for similar mixtures when compared to non-fly ash mixes. The government of countries like Malaysia, Indonesia, China, and India is investing more in infrastructure developments from fly ash as it is less permeable and emits less carbon dioxide, contributing towards fewer emissions.

- China is investing USD 1.43 trillion in major construction projects in the next five years till 2025. According to National Development and Reform Commission (NDRC), the Shanghai plan includes an investment of USD 38.7 billion in the next three years, whereas Guangzhou signed 16 new infrastructure projects with an investment of USD 8.09 billion.

- In 2022, India contributed about USD 640 billion to the construction industry due to government initiatives in infrastructure development and affordable housing, such as housing to all, smart city plans, and others. The growing construction activities in the country are driving the demand for silicones, which, in turn, may drive the chloromethane market over the forecast period.

- The agriculture sector uses fly ash for soil stabilization, accounting for about 14% of the fly ash market. The mining industry is looking for alternative stowing materials, and fly ash has been demonstrated as the alternative, as fly ash reduces water consumption by about 50%. Asia Pacific holds about 38% of the global mining project, thus increasing the demand for fly ash.

- It is also used in water treatment to reduce total dissolved solids(TDS), total suspended solids(TSS), and the ph level of water to purify water in the region, thus propelling the demand for fly ash.

- Major companies in the region include Boral Limited and Ashtech (India) Pvt Ltd.

- The aforementioned factors and government support have helped contribute to the increasing demand for the fly ash market.

Fly Ash Industry Overview

The fly ash market is fragmented, with the major players accounting for marginal shares of the market. Some of the companies in the market include Boral, Cemex SAB de CV, Charah Solutions Inc., Separation Technologies LLC, and Cement Australia, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Industry

- 4.1.2 Government Policies to Promote the Usage of Fly Ash

- 4.2 Restraints

- 4.2.1 Harmful Properties of Fly Ash

- 4.2.2 Non-suitability in Cold Weather Conditions

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Class F

- 5.1.2 Class C

- 5.2 Application

- 5.2.1 Construction

- 5.2.1.1 Bricks and Blocks

- 5.2.1.2 Road Construction

- 5.2.1.3 Portland Cement and Concrete

- 5.2.2 Agriculture

- 5.2.3 Mining

- 5.2.4 Water Treatment

- 5.2.5 Other Applications

- 5.2.1 Construction

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Ashtech Industries

- 6.4.2 Boral Resources

- 6.4.3 Charah Solutions,Inc

- 6.4.4 Cemex SAB de CV

- 6.4.5 Cement Australia

- 6.4.6 LafargeHolcim

- 6.4.7 Salt River Materials Group

- 6.4.8 Seperation Technologies LLC

- 6.4.9 Suyog Suppliers

- 6.4.10 Waste Management

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand from Waste Management and Precast Concrete Products

02-2729-4219

+886-2-2729-4219

2024 年飛灰世界市場報告

2024 年飛灰世界市場報告 飛灰市場:按類別、按應用:2023-2032 年全球機會分析與產業預測

飛灰市場:按類別、按應用:2023-2032 年全球機會分析與產業預測 粉煤灰市場:按類型(C 類、F 類)、用途(農業、磚塊/塊、水泥/混凝土)- 2023-2030 年全球預測

粉煤灰市場:按類型(C 類、F 類)、用途(農業、磚塊/塊、水泥/混凝土)- 2023-2030 年全球預測 全球粉煤灰市場:到 2028 年的預測—按類型(F 類和 C 類)、應用(建築、農業、採礦、水處理、其他應用)和地區分析

全球粉煤灰市場:到 2028 年的預測—按類型(F 類和 C 類)、應用(建築、農業、採礦、水處理、其他應用)和地區分析 飛灰的全球市場:市場規模,佔有率,成長分析,各類型,各用途 - 產業預測(2022年~2028年)

飛灰的全球市場:市場規模,佔有率,成長分析,各類型,各用途 - 產業預測(2022年~2028年) 飛灰的全球市場 2023-2027

飛灰的全球市場 2023-2027 粉煤灰市場:現狀分析·預測 (2022年~2028年)

粉煤灰市場:現狀分析·預測 (2022年~2028年) 飛灰的全球市場預測(2022年~2027年)

飛灰的全球市場預測(2022年~2027年)