|

市場調查報告書

商品編碼

1404420

汽車超級電容器 -市場佔有率分析、產業趨勢/統計、2024-2029 年成長預測Automotive Ultra-capacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

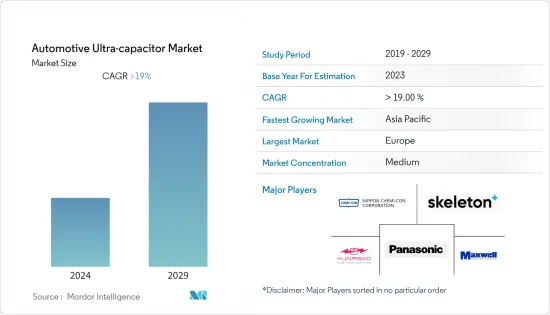

汽車超級電容器市場目前價值15億美元。

預計未來五年將成長至 42.7 億美元,預測期內收益複合年增率為 19%。

從中期來看,由於頒布了更嚴格的排放氣體和燃油效率法規,以及政府加強補貼和福利等措施來增加電動車的普及,預計在預測期內將出現強勁成長。

超級電容器的使用擴大了電池負載,使汽車製造商能夠實現燃油效率、延長電池壽命、減輕車輛重量並減少二氧化碳排放。超級電容器可能會在所有類型的車輛中迅速普及,包括傳統車輛、混合和電動車,以滿足世界各地日益嚴格的排放法規。

超級電容器通常與汽車電池並聯,以支援啟動/停止和再生煞車應用中出現的短時(小於 30 秒)尖峰負載需求。超級電容器提供的高能量、快速充電和放電能力促使汽車製造商將其部署在啟動/停止和再生煞車系統中。汽車內燃機、燃料電池和蓄電池等初級能源已被認為在滿足峰值功率需求和為上述應用捕獲能量方面效率低下。

汽車超級電容器市場趨勢

日益嚴格的廢氣法規和對電動車的需求不斷增加

世界各國政府都在製定雄心勃勃的排放目標,而增加電動車的使用被視為實現這些目標的一種方式。例如,歐盟(EU)的目標是到2030年將溫室氣體排放減少55%,中國則制定了2025年使新車銷售量的25%為電動車的目標。

大多數電動車所使用的鋰離子電池在能量密度、充電時間和整體性能方面都有了很大的改善。這使得電動車更加實用,對消費者也更有吸引力。

對電動車不斷成長的需求將導致電池化學和材料的技術進步。需要更先進、更有效率的汽車電池來確保安全和性能。許多著名的汽車製造商都致力於與汽車電池製造公司建立長期的業務關係。例如

- 2023年6月,Panasonic控股的負責人表示,該日本公司打算在三年內將與特斯拉共同管理的內華達州工廠的電動車電池產量提高10%。松下能源計畫在內華達州超級工廠增設第 15 條生產線。松下能源在會上宣布,計劃在2026年3月將內華達工廠的產能提高10%。

美國環保署 (EPA) 和美國運輸部國家公路交通安全管理局 (NHTSA) 正在推動環保車輛(小客車和商用車)的生產,以確保提高燃油效率並減少碳排放。正在努力支持。透過這些努力,政府計畫在2025年減少約31億噸二氧化碳排放,節省約60億桶石油。

此外,歐盟 (EU) 還制定了排放標準,規範小客車和商用車的二氧化碳排放量。近年來,交通運輸排放增加,目前佔歐盟溫室氣體排放的四分之一。

因此,歐盟委員會、歐洲議會和歐盟成員國正準備將輕型車輛的二氧化碳排放法規從 2025 年延長至 2030 年。此外,為了滿足上述標準,超級電容器的採用正在增加,預計在預測期內也會出現類似的趨勢。

由於上述全球市場的開拓,市場可能在預測期內顯著成長。

亞太地區和歐洲主導汽車超級電容器市場

歐洲地區混合動力汽車和電動車的銷售量快速成長,超級電容器的需求預計將成長,以滿足車輛電能的最佳利用。

每個地區的汽車製造商和生態系統相關人員已經開始根據客戶需求和偏好來適應不斷變化的地區模式。由於汽車需求的增加和全球生活水準的提高,研究目標市場預計將擴大。此外,都市化的加速和人口成長創造了對汽車的需求。

由於基礎設施的開拓和汽車銷售的增加,預計亞太市場在預測期內將以更快的速度成長。此外,汽車中大量使用電子元件的中國在收益方面領先市場,其次是日本、韓國和印度。

中國是全球最大的電動車生產國和消費國。銷售目標、有利的立法和城市空氣品質目標支持國內需求。例如,

- 中國對電動車和混合動力汽車製造商實施了配額,其銷量必須至少佔新車銷量的10%。此外,為了鼓勵民眾轉換電動車,北市每月只發放1萬張內燃機汽車登記許可證。

中國已經在混合公車中使用超級電容。這些公車配備了起停引擎和超級電容,可減少電池的負載,並延長其使用壽命。

隨著不斷的技術創新,中國製造商正在擴大其超級電容產品組合。中國中車是中國國有鐵路車輛製造商和全球最大的鐵路建設公司,它開發了一種基於石墨烯的超級電容,有潛力為電動公車提供更高效率和更長的供電。

汽車超級電容器產業概況

汽車超級電容器市場由 Maxwell Technologies、Skeleton Technologies、Kemet Corporation 和 Panasonic Corporation 等幾家主要企業主導。在預測期內,製造設施的快速擴張、汽車製造商和零件製造商之間合作夥伴關係的加強可能會顯示出市場的顯著成長。例如

- 2023 年 3 月,Invest Estonia 和 Skeleton Technologies 從德國政府和薩克森州獲得了 5,374 萬美元,用於在萊比錫建造第二個生產裝置。透過這筆基金,該公司擴大了超級電容器等產品範圍。

- 2022 年 10 月,Skeleton Technologies 發布了超級電池,並宣布殼牌作為合作夥伴。 SuperBattery是一項結合了超級電容器和電池特性的創新技術。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 電動車需求增加

- 市場抑制因素

- 與產品相關的高成本

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔(市場規模(美元))

- 按用途

- 開始/停止操作

- 再生煞車系統

- 其他用途

- 按車型

- 小客車

- 商用車

- 按銷售管道

- 目的地設備製造商(OEM)

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 其他

- 南美洲

- 中東/非洲

- 北美洲

第6章競爭形勢

- 供應商市場佔有率

- 公司簡介

- Maxwell Technologies

- Skeleton Technologies

- Panasonic Corporation

- Nesscap Battery

- Nippon Chem-Con Corporation

- Hitachi AIC Inc.

- ELNA America Inc.

- LOXUS Inc.

- Yunasko Ltd

- Nichicon Corporation

- LS Mtron Ltd

第7章 市場機會及未來趨勢

The automotive ultra-capacitor market is valued at USD 1.50 billion in the current year. It is anticipated to grow to USD 4.27 billion by the next five years, registering a CAGR of 19% in terms of revenue during the forecast period.

Over the medium term, the enactment of stringent emissions and fuel economy norms and increasing government initiatives, in terms of subsidies and benefits for increasing the adoption rate of electric vehicles, is expected to witness major growth during the forecast period.

The use of ultra-capacitors expanded the battery load and enabled vehicle manufacturers to achieve fuel efficiency, extended battery life, reduced vehicle weight, and reduced CO2 emissions. Ultra-capacitors are likely to penetrate at a faster rate in all vehicle types, including conventional, hybrid, and electric vehicles, to meet the growing stringent emission rules across the world.

Ultra-capacitors, typically connected in tandem with vehicle batteries, support peak load demands for short intervals (which are less than 30 seconds) encountered during start/stop and regeneration braking applications. The capacity for quick recharge and discharge of high energy offered by ultra-capacitors drove the vehicle manufacturers to deploy them in the start/stop systems and regenerative braking systems. Primary energy sources, like internal combustion engines, fuel cells, and batteries in vehicles, were identified to be inefficient in handling peak power demand or recapturing energy during the applications above.

Automotive Ultra-capacitor Market Trends

Growing Stringent Emission Regulations and Increase in demand for Electric Vehicles

Governments around the world are setting ambitious targets to reduce emissions, and promoting the use of electric vehicles is seen as one way to achieve these goals. For instance, the European Union aims to reduce its greenhouse gas emissions by 55% by 2030, and China set a target of having 25% of new cars sold by 2025 to be electric.

Lithium-ion batteries, which are used in most electric vehicles, saw a significant improvement in terms of energy density, charging time, and overall performance. It made electric vehicles more practical and appealing to consumers.

The growing demand for EVs will lead to technological advancements in battery chemistry and materials. It will require more sophisticated and efficient automotive batteries to ensure safety and performance. Many prominent automobile manufacturers are focusing on building long-term business relationships with automotive battery manufacturing companies. For instance,

- In June 2023, according to a Panasonic Holdings representative, the Japanese corporation intends to increase the output of electric vehicle batteries at a Nevada factory jointly managed with Tesla by 10% within three years. Panasonic Energy plans to add a 15th production line to the Gigafactory Nevada. At a meeting, Panasonic Energy announced a proposal to boost the Nevada factory's manufacturing capacity by 10% by March 2026.

The United States Environmental Protection Agency (EPA) and the National Highway Traffic Safety Administration (NHTSA) are taking initiatives to support the production of eco-friendly vehicles (both passenger vehicles and commercial vehicles) to ensure improved fuel economy and reduced carbon emissions. Through these initiatives, the government is planning to reduce about 3,100 million metric tons of CO2 emissions and save about 6 billion barrels of oil by 2025.

Additionally, the European Union (EU) set emission standards to regulate the CO2 emission levels of passenger cars and commercial vehicles. Transport emissions increased in recent years and now account for a quarter of the EU's total GHG emissions.

As a result, the European Commission, European Parliament, and EU member states are preparing to extend the light-duty vehicles' CO2 regulation to 2025-2030. Furthermore, to meet the standards above, the adoption of the ultra-capacitor is increasing and is expected to witness the same trend during the forecast period.

With the development mentioned above across the globe, the market is likely to witness major growth during the forecast period.

Asia-Pacific and Europe to Dominate the Automotive Ultra-capacitor Market

With the rapidly growing hybrid and electric vehicle sales in the European region, the demand for ultra-capacitors is anticipated to grow to meet the optimal utilization of electric energy in vehicles.

Automotive manufacturers and ecosystem stakeholders in each region began to adapt to the changing regional patterns based on customer needs and preferences. The market studied is expected to expand due to rising vehicle demand and rising living standards around the globe. Furthermore, increased urbanization and an increasing population created a demand for automobiles.

The Asia-Pacific market is expected to grow at a faster pace during the forecast period, owing to development in infrastructure and increased vehicle sales. Furthermore, China is leading the market in terms of revenue due to its massive use of electronic components in vehicles, followed by Japan, Korea, and India.

China is the largest manufacturer and consumer of electric vehicles in the world. Sales targets, favorable laws, and municipal air-quality targets are supporting domestic demand. For instance,

- China imposed a quota on manufacturers of electric or hybrid vehicles, which must represent at least 10% of total new sales. Also, the city of Beijing only issues 10,000 permits for the registration of combustion engine vehicles per month to encourage its inhabitants to switch to electric vehicles.

China is already using supercapacitors in hybrid buses. These buses are equipped with stop-start engines, in which supercapacitors reduce the load on the battery, which increases the lifetime of the batteries.

Due to continuous innovation, Chinese manufacturers are expanding their supercapacitor portfolio. The CRRC, the Chinese state-owned rolling stock manufacturer and the world's largest train builder developed graphene-based supercapacitors that may power electric buses with higher efficiency and for a longer period.

Automotive Ultra-capacitor Industry Overview

The automotive ultra-capacitor market is dominated by several key players, such as Maxwell Technologies, Skeleton Technologies, Kemet Corporation, and Panasonic Corporation, among others. The rapid expansion of manufacturing facilities and an increase in partnership between the vehicle manufacturer and the component manufacturer is likely to witness major growth for the market during the forecast period. For instance,

- In March 2023, Invest Estonia and Skeleton Technologies received USD 53.74 million from the German government and the state of Saxony for its second production unit to be built in Leipzig. Through this fund, the company expanded its products, including ultra-capacitor.

- In October 2022, Skeleton Technologies introduced its SuperBattery and unveiled Shell as a partner. SuperBattery is an innovative technology combining the characteristics of supercapacitors and batteries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in demand for Electric Vehicles

- 4.2 Market Restraints

- 4.2.1 High Cost Associated With Product

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 By Application

- 5.1.1 Start-stop Operation

- 5.1.2 Regenerative Braking System

- 5.1.3 Other Applications

- 5.2 By Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Commercial Vehicle

- 5.3 By Sales Channel

- 5.3.1 Original Equipment Manufacturer (OEM)

- 5.3.2 Aftermarket

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Maxwell Technologies

- 6.2.2 Skeleton Technologies

- 6.2.3 Panasonic Corporation

- 6.2.4 Nesscap Battery

- 6.2.5 Nippon Chem-Con Corporation

- 6.2.6 Hitachi AIC Inc.

- 6.2.7 ELNA America Inc.

- 6.2.8 LOXUS Inc.

- 6.2.9 Yunasko Ltd

- 6.2.10 Nichicon Corporation

- 6.2.11 LS Mtron Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年汽車超級電容器全球市場報告

2024 年汽車超級電容器全球市場報告 汽車超級電容器全球市場規模、佔有率、趨勢分析報告:按應用、按推進類型、按車輛類型、按地區、展望和預測,2023-2030 年

汽車超級電容器全球市場規模、佔有率、趨勢分析報告:按應用、按推進類型、按車輛類型、按地區、展望和預測,2023-2030 年 到 2030 年汽車超級電容器市場預測:按類型、車輛類型、電動車、應用和地區進行的全球分析

到 2030 年汽車超級電容器市場預測:按類型、車輛類型、電動車、應用和地區進行的全球分析 超級電容器市場、份額、規模、趨勢、行業分析報告:按功率;按類型;按最終用戶;按地區;按細分市場預測,2023-2032 年

超級電容器市場、份額、規模、趨勢、行業分析報告:按功率;按類型;按最終用戶;按地區;按細分市場預測,2023-2032 年 2023-2030年全球超級電容器市場規模研究與預測,按類型(雙層電容器、擬電容器、混合電容器)、按應用(汽車、消費電子、能源、工業及其他)和區域分析。

2023-2030年全球超級電容器市場規模研究與預測,按類型(雙層電容器、擬電容器、混合電容器)、按應用(汽車、消費電子、能源、工業及其他)和區域分析。 超級電容器的全球市場

超級電容器的全球市場 全球超級電容器市場:按類型(雙層電容器、贗電容器、混合電容器)按應用(汽車、消費電子產品、能源、工業、其他):2021-2031 年全球機會分析和行業預測

全球超級電容器市場:按類型(雙層電容器、贗電容器、混合電容器)按應用(汽車、消費電子產品、能源、工業、其他):2021-2031 年全球機會分析和行業預測 車載用超級電容器的全球市場 2023-2027

車載用超級電容器的全球市場 2023-2027 超級電容器的全球市場 (2022~2030年):成長、未來展望、競爭分析

超級電容器的全球市場 (2022~2030年):成長、未來展望、競爭分析