|

市場調查報告書

商品編碼

1273476

特種氣體市場 - 增長、趨勢和預測 (2023-2028)Specialty Gas Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

在預測期內,特種氣體市場預計將以超過 4% 的複合年增長率增長。

主要亮點

- COVID-19 對 2020 年的市場產生了負面影響。 不過,預計市場將在2022年達到疫情前的水平,並繼續保持穩定增長。

- 特種氣體市場的增長預計將受到以下因素的推動:半導體設備和平板顯示器的製造需求增加,以及它們用作高科技薄膜等離子增強化學氣相沉積 (PECVD) 的清潔氣體.

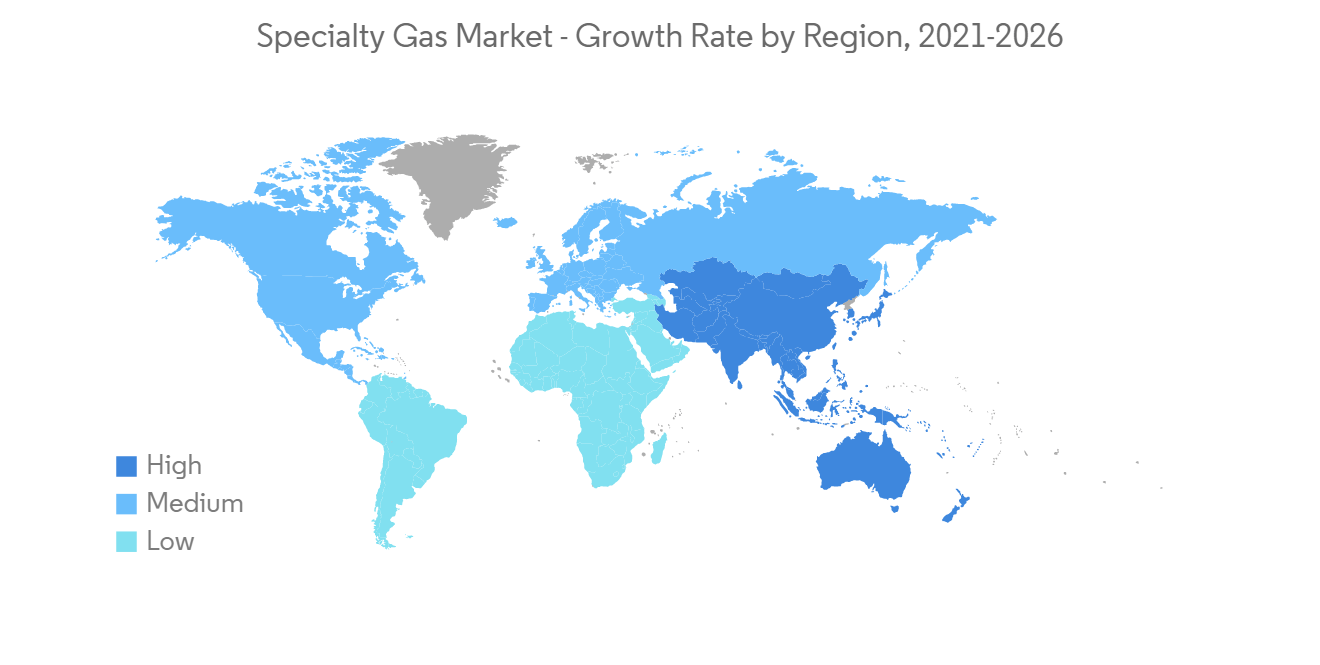

- 嚴格的環境法規以及特種氣體生產和質量控制方面的法規預計會阻礙市場增長。 預計在預測期內,製藥或生物技術領域的應用將成為市場機遇。 亞太地區主導著全球市場,中國、印度和日本等國家的消費量最大。

特種氣體市場趨勢

電子驅動特種氣體市場

- 在電子行業中,發光二極管 (LED) 是特種氣體的主要應用之一,與傳統照明相比,具有能耗更低、使用壽命更長等優勢。需求不斷增長。 氨用於氮化物基薄膜和外延晶體。 超高純度外延晶體對於 LED 應用很重要。

- 此外,用於製造個人電腦和智能手機的半導體數量持續增加,推動了特種氣體市場的增長。 多年來,由於對移動電話、便攜式計算設備、遊戲機和其他個人電子產品的需求不斷增長,全球消費電子行業經歷了快速增長。

- 中國擁有世界上最大的電子產品生產基地。 電線、電纜、計算設備和其他個人設備等電子產品的電子產品增長最快。 該國滿足國內對電子產品的需求,並向其他國家出口電子產品,導致市場增長顯著。

- 此外,印度的電子行業是世界上發展最快的行業之一。 根據電子和 IT 部的一項名為 "擴大和深化電子製造業的行動呼籲" 的研究,印度希望到 2026 年從電子製造業中賺取 3000 億美元。

- 根據印度品牌資產基金會 (IBEF) 的數據,印度在 2022 年 9 月出口了價值 20.907 億美元的電子產品,同比增長 71.99%。 該行業的主要出口項目包括手機、消費電子(電視、音響)、IT硬件(筆記本電腦、平板電腦)、工業電子、汽車電子等,支撐著市場的增長。。

- 上述所有因素預計將在預測期內推動特種氣體市場。

亞太地區主導市場

- 亞太地區預計將成為預測期內增長最快的特種氣體市場,因為該地區蓬勃發展的電子、汽車和醫療保健行業等廣泛使用特種氣體。.

- 就需求而言,該地區的電子產品在消費電子產品領域的增長率最高。 隨著中產階級可支配收入的增加,對電子產品的需求預計將穩步增長,從而推動所研究的市場。

- 根據中國國家統計局 (NBS) 的數據,2021 年中國電子製造業整體利潤同比增長 38.9%,這對市場增長產生了積極影響。

- 此外,根據日本電子資訊技術產業協會 (JEITIA) 的數據,日本電子行業的總產值到 2021 年將增長約 10%,達到約 1000 億美元。 該領域包括電子產品和組件,以及消費電子和工業電子產品。

- 此外,中國汽車行業的擴張預計將有利於特種氣體的需求。 根據國際汽車製造商組織 (OICA) 的數據,中國是最大的汽車生產國。 2021 年僅中國就將生產 26,082,220 輛汽車。

- 因此,預計在預測期內,各行業不斷增長的需求將推動該地區的市場。

特種氣體行業概況

特種氣體市場本質上是部分整合的。 市場參與者包括 Linde plc、Air Liquide、Messer Group GmbH、Showa Denko K.K. 和 Air Products and Chemicals, Inc.。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第 1 章介紹

- 調查先決條件

- 本次調查的範圍

第 2 章研究方法論

第 3 章執行摘要

第 4 章市場動態

- 促進因素

- 電子行業的廣泛應用

- 醫療保健領域的需求不斷擴大

- 抑制因素

- 嚴格的環境法規、對特種氣體生產和質量控制的限制

- 其他限制

- 工業價值鏈分析

- 波特的五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章市場細分

- 類型

- 高純度氣體

- 惰性氣體

- 碳基氣體

- 鹵素氣體

- 其他類型

- 最終用戶行業

- 汽車相關

- 電子產品

- 醫療/保健

- 食物和飲料

- 石油和天然氣

- 其他最終用戶行業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 意大利

- 法國

- 其他歐洲

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙特阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第 6 章競爭格局

- 併購、合資、合作、合同等。

- 市場份額 (%)/排名分析

- 主要公司採用的策略

- 公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Coregas

- Iwatani Corporation of America

- Linde plc

- MESA Specialty Gases & Equipment

- Messer Group GmbH

- Mitsui Chemicals, Inc.

- Norco Inc.

- SHOWA DENKO K.K.

- YUEYANG KAIMEITE ELECTRONIC AND SPECLALTY RARE GASES CO.

- ILMO Products Company

第 7 章市場機會與未來趨勢

- 在製藥和生物技術領域的應用

簡介目錄

Product Code: 68249

The specialty gas market is projected to register a CAGR of more than 4% during the forecast period.

Key Highlights

- COVID-19 negatively impacted the market in 2020. However, the market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The growth of the specialty gas market is anticipated to be driven by the increasing demand in manufacturing semiconductor devices and flat panel displays and its usage as a cleaning gas for plasma-enhanced chemical vapor deposition (PECVD) for high-tech thin films.

- Stringent environmental regulations and restrictions on specialty gas production and quality control are expected to hinder the market growth. Applications in the pharmaceutical or biotechnology sector are expected to act as opportunities for the market during the forecast period. The Asia-Pacific region dominates the global market, with the largest consumption from countries such as China, India, and Japan.

Specialty Gas Market Trends

Electronics Sector to Drive the Specialty Gas Market

- In the electronics industry, light-emitting diodes (LEDs) are one of the major applications of specialty gas, which find major consumer demand due to their advantages like lower energy consumption and longer operating life than other traditional lighting sources. Ammonia is used in nitride-based thin films and epitaxial crystals. In the application of LEDs, ultra-high purity of epitaxial crystals is critical.

- Furthermore, semiconductors utilized in the production of personal computers (PCs) and smartphones are constantly increasing, thus propelling the growth of the specialty gas market. The global consumer electronics industry has been growing rapidly worldwide over the years, owing to the consistently increasing demand for cellular phones, portable computing devices, gaming systems, and other personal electronic devices.

- China has the world's largest electronics production base. Electronic products, such as wires, cables, computing devices, and other personal devices, recorded the highest growth in electronics. The country serves the domestic demand for electronics and exports electronic output to other countries, thus providing huge market growth.

- Also, the Indian electronics industry is one of the fastest-growing industries globally. According to "A Call to Action for Broadening and Deepening Electronics Manufacturing," a study by the Ministry of Electronics and IT, India wants to make USD 300 billion from electronics manufacturing by 2026.

- According to India Brand Equity Foundation (IBEF), India exported USD 2,009.07 million worth of electronics in September 2022, up 71.99% year-over-year. Key export items in this industry include mobile phones, consumer electronics (TV and audio), IT hardware (laptops, tablets), industrial electronics, and auto electronics, supporting the market growth.

- All the aforementioned factors are expected to drive the specialty gas market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to be the fastest-growing specialty gas market during the forecast period due to the wide consumption of specialty gases in the electronics, automotive, healthcare industries, etc., which are among the booming sectors in the region.

- Electronic products in the region have the highest growth rates in the consumer electronics segment of the market in terms of demand. With the increase in the disposable incomes of the middle-class population, the demand for electronic products is projected to increase steadily, thereby driving the market studied.

- According to the National Bureau of Statistics (NBS) of China, the overall profit of China's electronics manufacturing businesses increased by 38.9% year-on-year in 2021, thus positively impacting the market's growth.

- Furthermore, according to Japan Electronics and Information Technology Industries Association (JEITIA), the overall production value of the Japan electronics sector increased by almost 10% to around USD 100 billion in 2021. The sector includes electronic devices and components, as well as consumer and industrial electronic equipment.

- Additionally, the expansion of the automotive segment in China is anticipated to benefit the demand for specialty gas. According to the International Organization of Motor Vehicle Manufacturers (French: Organisation Internationale des Constructeurs d'Automobiles) (OICA), China is the largest producer of automobiles. The country alone produced 2,60,82,220 units of vehicles in 2021.

- Thus, the rising demand from various industries is expected to drive the market in the region during the forecast period.

Specialty Gas Industry Overview

The specialty gas market is partially consolidated in nature. Some of the players in the market are Linde plc, Air Liquide, Messer Group GmbH, Showa Denko K.K., and Air Products and Chemicals, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Wide Applications in the Electronics Industry

- 4.1.2 Increasing Demand from the Healthcare Sector

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations and Restrictions on Specialty Gas Production and Quality Control

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 High-purity Gases

- 5.1.2 Noble Gases

- 5.1.3 Carbon Gases

- 5.1.4 Halogen Gases

- 5.1.5 Other Types

- 5.2 End-User Industry

- 5.2.1 Automotive

- 5.2.2 Electronics

- 5.2.3 Medical and Healthcare

- 5.2.4 Food and Beverage

- 5.2.5 Oil and Gas

- 5.2.6 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Aregentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Coregas

- 6.4.4 Iwatani Corporation of America

- 6.4.5 Linde plc

- 6.4.6 MESA Specialty Gases & Equipment

- 6.4.7 Messer Group GmbH

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Norco Inc.

- 6.4.10 SHOWA DENKO K.K.

- 6.4.11 YUEYANG KAIMEITE ELECTRONIC AND SPECLALTY RARE GASES CO.

- 6.4.12 ILMO Products Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use in the Pharmaceutical or Biotechnology Sector

02-2729-4219

+886-2-2729-4219

特種氣體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區、競爭細分,2019-2029F

特種氣體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區、競爭細分,2019-2029F 2024 年溴化氫全球市場報告

2024 年溴化氫全球市場報告 2030 年溴化氫市場預測:按細分市場和地區分類的全球分析

2030 年溴化氫市場預測:按細分市場和地區分類的全球分析 特種氣體市場:2023-2028 年全球行業趨勢、佔有率、規模、成長、機遇和預測

特種氣體市場:2023-2028 年全球行業趨勢、佔有率、規模、成長、機遇和預測 特殊氣體的全球市場

特殊氣體的全球市場 特種氣體市場、份額、規模、趨勢、產業分析報告:按產品、應用、地區、細分市場預測,2023-2032 年

特種氣體市場、份額、規模、趨勢、產業分析報告:按產品、應用、地區、細分市場預測,2023-2032 年 特種氣體市場:按類型(碳氣體、鹵素氣體、稀有氣體)、按等級(高純度、研究級、超高純度)、按用途- COVID-19、俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響-世界2023-2030 年預測

特種氣體市場:按類型(碳氣體、鹵素氣體、稀有氣體)、按等級(高純度、研究級、超高純度)、按用途- COVID-19、俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響-世界2023-2030 年預測 到 2028 年的特種氣體市場預測 - 按產品(鹵素氣體、超高純氣體、碳氣體、稀有氣體、其他產品)、應用和地區分列的全球分析

到 2028 年的特種氣體市場預測 - 按產品(鹵素氣體、超高純氣體、碳氣體、稀有氣體、其他產品)、應用和地區分列的全球分析 特種氣體市場規模、份額和趨勢分析報告:按產品(惰性氣體、碳氣體)、按應用(製造、電子、醫療保健)、按地區、細分趨勢,2023-2030 年

特種氣體市場規模、份額和趨勢分析報告:按產品(惰性氣體、碳氣體)、按應用(製造、電子、醫療保健)、按地區、細分趨勢,2023-2030 年 高純度溴化氫 (HBr) 的全球市場的分析 (2022年)

高純度溴化氫 (HBr) 的全球市場的分析 (2022年)

▼