|

市場調查報告書

商品編碼

1405370

視訊管理服務:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Video Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

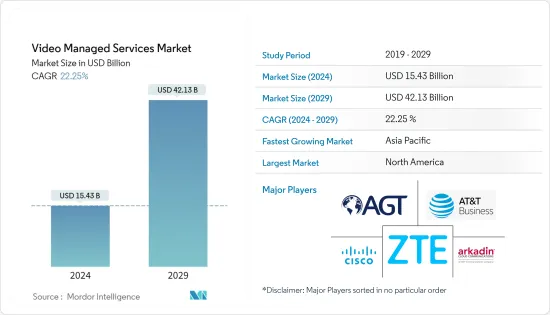

視訊管理服務市場規模預計到 2024 年為 154.3 億美元,預計到 2029 年將達到 421.3 億美元,在預測期內(2024-2029 年)複合年成長率為 22.25%。

託管服務使中小型企業能夠提高業務效率並降低營運成本,使他們能夠專注於自己的核心競爭力。託管服務可實現最佳資源分配和利用,提高整體盈利和業務效率。可擴展的基礎設施和託管服務模型使組織更容易採用新技術。預計這些變數將在未來的預測期內推動市場成長。

主要亮點

- 託管視頻會議服務市場增長的主要驅動力之一是對基本功能和提高效率的關注。 為了提高運營效率,公司專注於其業務流程的核心,並通過管理服務和資訊技術外包來接管 IT 運營。使用託管服務提供者來滿足與IT相關的需求,例如應用程式和基礎設施管理。 這將員工的技能和資源引導到核心業務上,説明公司實現他們的目標和願景。

- 視訊託管服務產業促進視訊託管服務市場成長的主要趨勢之一是託管服務的自動化程度不斷提高。視訊管理服務的自動化大大提高了業務流程的效率。透過管理複雜的IT基礎設施和簡化營運工作流程來增強您的業務能力。企業中託管基礎設施服務的自動化改善了作業流程,同時降低了成本。整合眾多的組織部門與職能,消除重複的 IT 流程。

- BYOD、巨量資料分析、人工智慧和機器學習環境是大型企業依賴影片MSP 的關鍵促進因素,因為它們專注於在數位轉型時代增強業務。大型企業選擇整合服務供應商,尤其是大型 MSP 的託管服務。這些供應商提供更好的技術支援、減少停機時間、強大的安全性以及先進的網路和技術解決方案,這些解決方案對於這些公司維持不間斷的業務流程至關重要。

- 託管服務提供者面臨的最大問題之一是網路安全。網路犯罪分子的目標是當今威脅生態系統中的小型和大型企業。較大的公司可能擁有更多的財務資源,但他們也有更多的資金用於先進防禦、遠端監控和網路安全解決方案,這使得它們更難以被攻破。同時,小型企業往往缺乏網路安全工具和保障措施。此外,安全問題可能會損害小型和大型企業的成功。因此,視訊 MSP 必須將網路安全作為其客戶的首要任務。

- 新冠疫情後在家工作趨勢的持續預計將推動所研究的市場。根據 Zippia 的 2022 年調查,到 2022 年,26% 的美國員工將進行遠距工作。到 2025 年,將有 3,620 萬美國員工遠距工作。

視訊管理服務市場趨勢

軟體部門推動成長

- 託管服務提供者 (MSP) 依靠許多專用的工具來集中客戶資訊。為了管理客戶的網路,MSP 主要依靠 RMM 軟體、PSA 軟體、防毒軟體和安全軟體以及復原和備份軟體。

- MSP 軟體旨在透過自動化在客戶設備上執行的任務來減少重複性任務和人為錯誤。此外,託管服務提供者需要專注於促進日常 IT 流程、提高用戶滿意度、提供更高品質的服務並降低營運成本的核心功能。這些是自訂MSP 軟體的一些優點。

- 此外,人們日益認知到節省成本和資源的重要性,也推動了採用雲端基礎的解決方案和依需安全服務的需求。公司正在意識到透過將資料移至雲端而不是建置和維護新的資料儲存來節省成本和資源的重要性。由於其多重優勢,雲端平台和生態系統有望成為未來幾年數位創新快速成長的關鍵跳板。

- 此外,實施公有雲端服務會在組織外部引入一層信任,這對於雲端基礎設施安全至關重要。然而,隨著雲端解決方案的使用越來越多,企業實施影片託管服務變得越來越容易。隨著 Google Drive、Dropbox 和 Microsoft Azure 等雲端服務成為業務流程的一部分,必須解決敏感資料失去控制等安全性問題。

北美預計將佔據很大佔有率

- 美國小型企業發展管理局報告稱,2022年美國小型企業數量將達到3,320萬家,99.99%的企業將位於美國。 2022年美國小型企業數量的成長反映穩定成長,較與前一年同期比較成長2.2%,較2017年至2022年成長12.2%。

- 事實上,以任何標準衡量,簽訂管理服務協議並讓來自各個領域的專家填補整個 IT 部門的空缺都更具成本效益。根據 CompTIA 研究,近一半使用 MSP 的公司將其年度 IT 成本降低了高達 25%。內部網路支援技術人員的年薪可能超過 10 萬美元,如果考慮到社會福利、培訓、設備、額外報酬和其他成本,則幾乎翻了兩番。透過與 MSP 合作,企業只需支付固定的月費即可獲得所需的 IT 服務,同時免除這些成本。

- 據Cisco稱,資料的增加和設備的成長正在增加網路的壓力。預計該地區的這一趨勢將在預測期內推動託管網路服務的發展。

- 此外,該地區OTT平台的成長也為市場帶來了巨大的成長機會。例如,2023 年第二季度,Netflix 在加拿大和美國的付費串流訂閱用戶達到 7,557 萬,高於上一季的 7,440 萬。

- 特別是,視訊會議託管服務市場正在不斷擴大,不僅包括視訊點播 (VOD) 的視訊工作流程和管理,還包括直接面對消費者的即時視訊 (D2C) 和 OTT (OTT) 內容。隨著該地區越來越多的內容提供者認知到外包的好處,預計該業務將繼續成長。

影片管理服務產業概述

隨著全球參與者不斷創新其服務以向用戶提供具有成本效益的服務,視訊管理服務市場變得碎片化,為市場上的競爭對手提供了高度競爭優勢。擁有重要市場佔有率的領先公司正致力於擴大海外基本客群,並利用策略合作舉措來提高市場佔有率和盈利。主要參與者包括 Arkadin Cloud Communications、AGT(Applied Global Technologies)和Cisco。

- 2023 年 5 月 - NTT 宣布 SPEKTRA 成為 NTT 託管網路解決方案的下一代全球服務平台。該平台利用 NTT 的管理服務經驗、專業知識和廣泛的技術力,為客戶提供網路轉型的直接途徑。

- 2023 年 1 月 - PV Lumens LLP 是一家快速成長的安全、保全、連接和生產力解決方案銷售商,宣布與視訊管理系統領導者 Digifort 合作,在印度提供其監控解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場動態

- 市場促進因素

- BYOD(自備設備)簡介

- 透過減少不必要的時間來提高生產力

- 市場抑制因素

- 初始投資和實施成本高

第6章市場區隔

- 依類型

- 軟體

- 硬體

- 依公司規模

- 主要企業

- 中小企業

- 依用途

- 公司間交易

- 企業與個人

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第7章 競爭形勢

- 公司簡介

- Arkadin Cloud Communications(NTT Communications)

- Applied Global Technologies

- Cisco Systems, Inc.

- ZTE Enterprise

- AT&T Business

- Polycom, Inc.

- BT Conferencing, Inc.

- Telus Communications

- Dimension Data

- AVI-SPL Inc.

- Vega Global

- Macro Technologies Inc.

第8章投資分析

第9章 市場機會及未來趨勢

The Video Managed Services Market size is estimated at USD 15.43 billion in 2024, and is expected to reach USD 42.13 billion by 2029, growing at a CAGR of 22.25% during the forecast period (2024-2029).

SMEs will be able to concentrate only on this their core competencies through managed services improving operational efficiency and cutting operating costs. Managed services give optimal resource allocation and utilization, which improves overall profitability and operational efficiency. New technologies are more easily adopted by organizations thanks to a number ofScalable Infrastructures and Management Services Models. In the coming forecast period, these variables are expected to fuel market growth.

Key Highlights

- The requirement to focus on fundamental capabilities and increase efficiency is one of the main drivers for this market growth in managed videoconferencing services. In order to increase operating efficiency, businesses are focusing on the core of their business processes and taking over IT operations through Management Services and Information Technology Outsourcing. They use a managed service provider to handle IT-related needs like application and infrastructure management. This is assisting businesses in achieving their goal and vision by directing employee skills and resources toward their core business.

- One of the important video-managed services industry trends contributing to video-managed services market growth is more automation in managed services. The automation of video-managed services greatly improves business process efficiencies. It assists businesses in managing complicated IT infrastructures and streamlining operational workflow. Automation of managed infrastructure services in enterprises improves operational procedures while decreasing costs. It integrates numerous organizational divisions and functions and eliminates the need for repetitive IT processes.

- BYOD, Big data analytics, AI, and ML Environments are the major drivers for large enterprises to rely on video MSPs as they focus on stepping up their operations in the digital transformation era. Large enterprises opt for managed services from integrated service providers, especially large MSPs. These providers offer better technology support, lower downtime, robust security, and advanced network and technology solutions, vital for such enterprises to maintain uninterrupted business processes.

- One of the biggest problems facing managed service providers is cybersecurity. Cybercriminals target both small and large businesses in the threat ecosystem of today. Larger businesses may have more financial resources, but they are more difficult to compromise because they also have more money to spend on advanced defenses, remote monitoring, and cybersecurity solutions. On the other hand, smaller firms frequently lack cybersecurity tools and safeguards. Furthermore, security problems can ruin the success of both small and large businesses equally. As a result, video MSPs must provide cybersecurity top priority to their customers.

- The continuation of the work-from-home trend in the post-COVID scenario is expected to drive the studied market. According to the Zippia survey 2022, as of 2022, 26% of US employees worked remotely.By 2025, 36.2 million American employees are likely to work remotely.

Video Managed Services Market Trends

Software Segment to Witness the Growth

- Managed service providers (MSPs) are relying on a number of specialized tools tailored to manage all their client's information in one place. In order to manage their client's network, they have primarily relied on RMM software, PSA software, the antivirus and safety software as well as recovery and backup software.

- MSP software is designed to reduce repetitive work and human error through the automation of tasks carried out by clients' devices. In addition, there is a need for the management service providers to concentrate on core capabilities that facilitate everyday IT processes, increase user satisfaction, provide better quality of services and lower operating costs. These are a few of the benefits you'll find in your custom MSP software.

- In addition, the demand for cloud based solutions and the adoption of on demand security services is driven by the growing realization of the importance of saving money and resources are moving Instead of building and maintaining new data storage, data is transferred to the cloud which is why enterprises are increasingly realizing the importance of saving money and resources by moving data to the cloud. Due to multiple benefits, cloud platforms and ecosystems are expected to be key launching points for a rapid growth in Digital Innovation over the coming years.

- Furthermore, the deployment of public cloud services introduces a layer of trust outside an organisation which is crucial in terms of security for Cloud Infrastructures. Nevertheless, the adoption of video managed services practices by businesses is made considerably easier as a consequence of increasing use of cloud solutions. Enterprises must address security concerns, such as the loss of control over confidential data, because more people are moving towards cloud services like Google Drive, Dropbox and Microsoft Azure among other tools becoming a part of their business processes.

North America is Expected to Hold Major Share

- The American Small Business Administration Office for Advocacy reports that the number of US small businesses in 2022 will be 33.2 million, and In the country accounting for almost all 99,99 percent of companies. With a 2.2% increase over the previous year and 12.2% during the period from 2017 to 2022, the increase in the number of small businesses in the US in 2022 reflects steady growth.

- It is more cost effective to enter into a management service agreement, filling an entire IT department with various subject-matter specialists by practically any standard. According to a CompTIA survey, about half of all businesses using MSPs cut their annual IT costs by up to 25%. In-house network support technicians can earn over USD 100,000 per year, and when firms factor in benefits, training, equipment, supplemental compensation, and other costs, that amount can almost quadruple. By working with an MSP, firms can get necessary IT services for a fixed monthly charge while being relieved of those expenses.

- According to Cisco Systems, the growth of data and devices is increasing the network burden, and In this way, 95% of network changes are carried out on a manual basis which increases operating costs by between 2 and 3 times the value of the network. This trend in the region is expected to drive the managed network services over the forecast period.

- Moreover, growth in OTT platforms in the region also offers considerable growth opportnuities for the market. For instance, Netflix reported 75.57 million paid streaming subscribers across Canada and the United States in the second quarter of 2023, up from 74.4 million in the previous quarter.

- Particularly, the video conferencing managed services market is expected to continue growing as more content providers in the region realize the advantages of outsourcing video workflows or management for both video on demand (VOD) as well as live video direct-to-consumer (D2C) OTT (over-the-top) content.

Video Managed Services Industry Overview

The video-managed services market is fragmented as the global players are innovating their services to provide cost-benefit offers to the users, which gives a high rivalry to the market competitors. Major players with a prominent share in the market are focusing on expanding their customer base across foreign countries by leveraging strategic collaborative initiatives to increase their market share and profitability. Key players are Arkadin Cloud Communications, AGT (Applied Global Technologies), Cisco Systems, Inc., etc.

- May 2023 - NTT introduced SPEKTRA as the next generation of its global services platform for NTT Managed Networks solutions. The Platform is equipped with the company's management services experience, expertise and extensive technological capacity to provide customers with a direct path into network transformation.

- January 2023 - PV Lumens LLP, a rapidly growing distributor of safety, security, connectivity, and productivity solutions, announced a partnership with Digifort, a leader in video management systems, to offer their surveillance solutions in India.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of BYOD (Bring Your Own Device)

- 5.1.2 Higher Productivity Rate by Reducing Unnecessary Hours

- 5.2 Market Restraints

- 5.2.1 High Initial Investments and Installation Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Software

- 6.1.2 Hardware

- 6.2 By Enterprise Size

- 6.2.1 Large Enterprise

- 6.2.2 Small & Medium Enterprise

- 6.3 By Applications

- 6.3.1 Business to Business

- 6.3.2 Business to Consumer

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Arkadin Cloud Communications ( NTT Communications)

- 7.1.2 Applied Global Technologies

- 7.1.3 Cisco Systems, Inc.

- 7.1.4 ZTE Enterprise

- 7.1.5 AT&T Business

- 7.1.6 Polycom, Inc.

- 7.1.7 BT Conferencing, Inc.

- 7.1.8 Telus Communications

- 7.1.9 Dimension Data

- 7.1.10 AVI-SPL Inc.

- 7.1.11 Vega Global

- 7.1.12 Macro Technologies Inc.