|

市場調查報告書

商品編碼

1273499

碳化鎢市場 - 增長、趨勢、COVID-19 影響和預測 (2023-2028)Tungsten Carbide Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

在預測期內,碳化鎢市場預計將以每年約 3.5% 的速度溫和增長。

COVID-19 疫情對碳化鎢市場產生了各種影響。 一方面,來自醫療行業的需求拉動了市場的大幅增長,而另一方面,其他行業也受到了全州停工和嚴格限制的負面影響。

主要亮點

- 由於全球製造業的發展,對 c 的需求也在增加。 碳化鎢廢料也是可回收的,作為一種可用於所有應用的高價值合金,對市場產生了積極影響。

- 另一方面,碳化鎢的使用帶來的毒性限制了市場的擴張。

- 商業領域對自動閥門不斷增長的需求可能會支持所研究市場的增長。

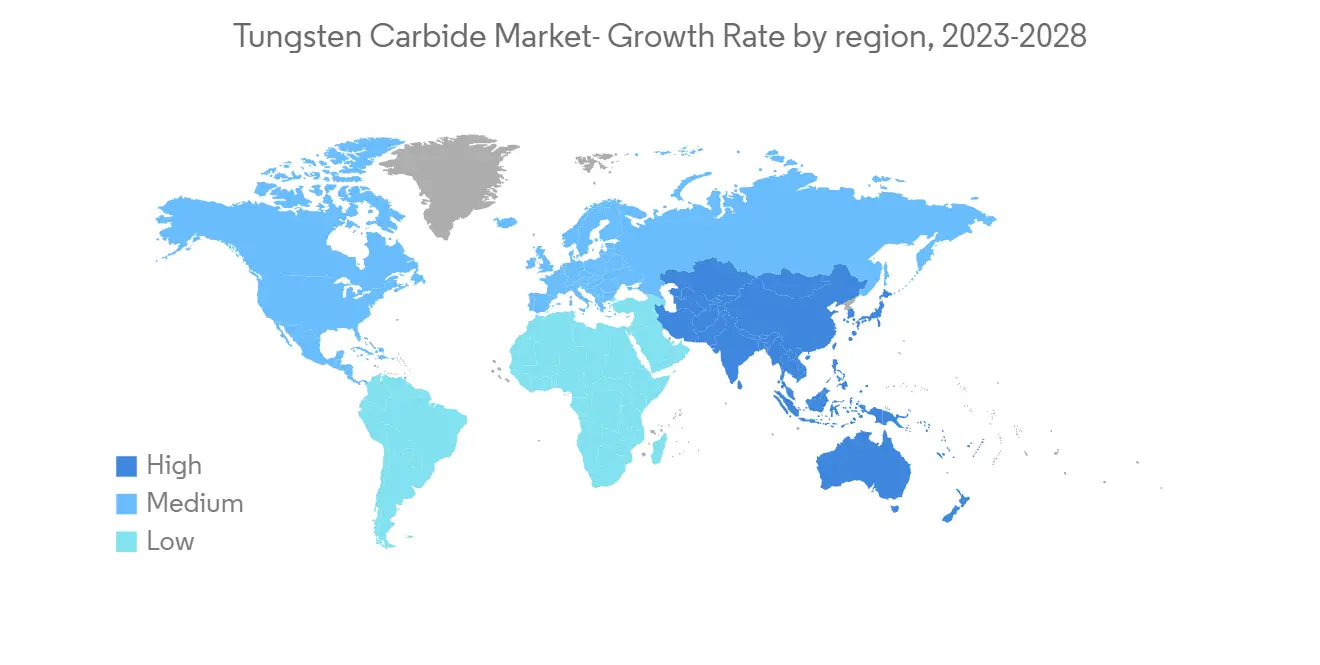

- 預計亞太地區在未來五年內將佔據最大份額和最高複合年增長率。

碳化鎢市場趨勢

硬質合金推動市場增長

- 硬質合金是一種粉末冶金材料,由碳化鎢顆粒和富含金屬鈷的粘合劑組成。

- 硬質合金具有耐磨、耐撓曲、抗拉、抗壓、高溫耐磨等獨特的物理機械性能,我來了。

- 用於製造玻璃瓶、鋁罐、塑料管、鋼絲、銅絲等的工具都是由硬質合金製成的。 其他應用包括切削金屬、加工木材、塑料、複合材料、軟陶瓷、無屑成型(熱和冷)、採礦和建築、結構件、耐磨件和軍用零件。

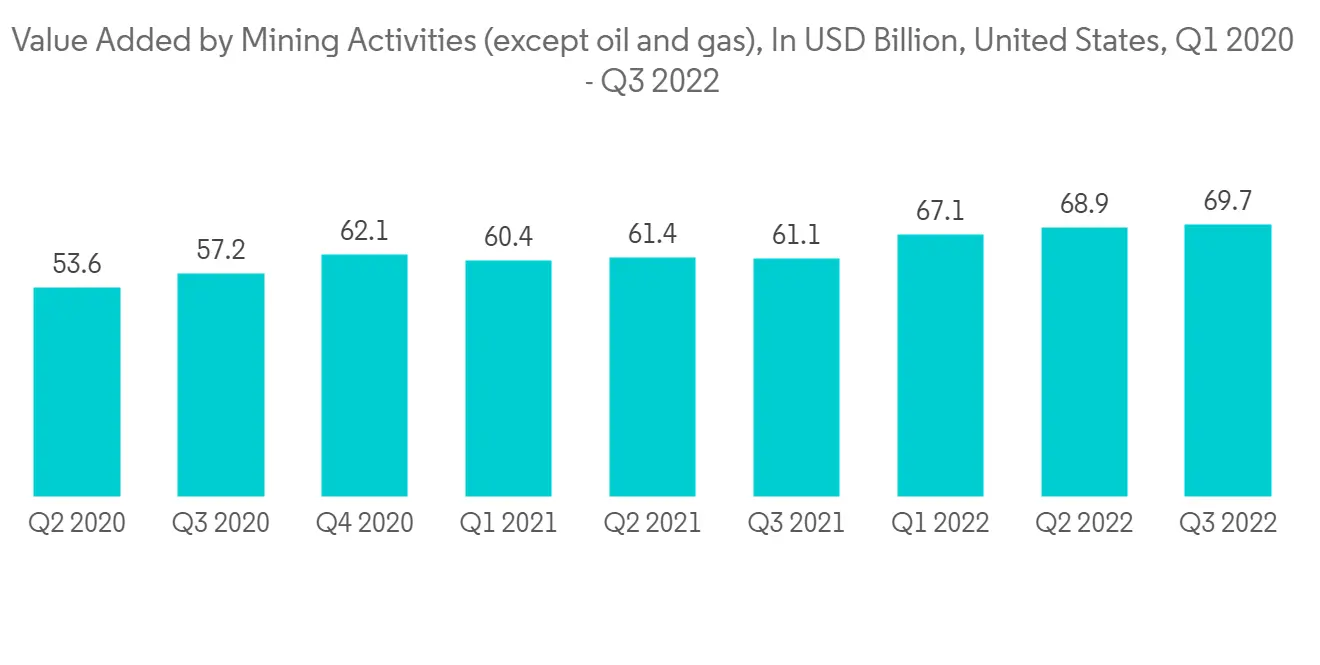

- 根據經濟分析局的數據,2022 年前三季度美國的建築業總增加值約為 2.98 萬億美元,比去年同期增長約 5%。 硬質合金的主要功能是用於工業工具,提供其他材料所沒有的特性。

- 此外,採礦業的增加值在 2022 年前三季度強勁增長約 30%,與去年同期相比達到約 1.49 萬億美元。

- 硬質合金市場預計在預測期內會增長,因為硬質合金所擁有的特性使其比其他工具更具優勢,從而導致各種應用的需求增加。

亞太地區主導市場

- 亞太地區是全球碳化鎢市場中最大的區域市場。 由於中國、印度和日本等國家的汽車、建築和金屬加工行業的需求不斷增長,該市場對碳化鎢有需求。

- 亞太地區主導著全球市場份額。 中國、印度和日本等國家運輸活動的增加增加了該地區碳化鎢的使用。

- 中國是最大的汽車生產國和消費國。 中國汽車工業協會報告稱,與上年相比,2022年中國汽車銷量將增長2.1%左右。 2022 年售出約 2686 萬輛汽車,而 2021 年售出 2627 萬輛汽車。

- 菲律賓統計局還在其 2022 年年度報告中表示,該國 GDP 同比增長 7.6% 很大程度上得益於汽車和摩托車的維修。 該行業是最重要的貢獻者,貢獻了約 8.7% 的整體增長。

- 根據日本電子信息技術產業協會 (JEITA) 的估計,截至 2022 年 11 月,日本電子行業的總產值將達到約 10.1 萬億日元(845 億美元),同比增加了 100.7.%。 與上一年相比,截至 11 月,日本的電子產品出口增長了近 15%。

- 此外,日本的礦業包括規模不大的煤炭和有色金屬採礦部門、重要的工業礦物採礦部門以及黑色金屬/有色金屬和工業礦物初級礦物加工部門。

- 因此,製造活動的增加、汽車行業的增加以及電子行業的興起都促進了硬質合金和其他應用的增長,預計在預測期內將推動硬質合金市場的增長。

碳化鎢行業概況

全球碳化鎢市場是分散的。 主要公司包括(排名不分先後)Umicore、CERATIZIT S.A.、Extramet Products, LLC、Kennametal Inc. 和 American Elements。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第一章介紹

- 調查結果

- 本次調查的假設

- 本次調查的範圍

第二章研究方法論

第 3 章執行摘要

第四章市場動態

- 主持人

- 擴大碳化鎢在各個最終用戶行業中的應用

- 碳化鎢的可重現特性

- 約束因素

- 碳化鎢毒性

- 其他抑製劑

- 工業價值鏈分析

- 波特的五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章市場細分

- 申請

- 硬質合金

- 塗層

- 合金

- 最終用戶

- 航空航天與國防

- 汽車

- 採礦和建築

- 電子產品

- 其他(醫療、運動等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 意大利

- 法國

- 其他歐洲

- 世界其他地方

- 南美洲

- 中東和非洲

- 亞太地區

第六章競爭格局

- 併購、合資、合作、合同等。

- 市場份額/排名分析

- 主要公司採用的策略

- 公司簡介

- American Elements

- Buffalo Tungsten Inc.

- CERATIZIT S.A.

- China Tungsten

- CY Carbide Mfg. Co., Ltd.

- Extramet Products, LLC.

- Federal Carbide Company

- Guangdong Xianglu Tungsten Co., Ltd.

- H.C. Starck Tungsten GmbH

- Jiangxi Yaosheng Tungsten Co., Ltd.

- Kennametal Inc.

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

- Umicore

第七章市場機會與未來趨勢

- 對自動閥門的需求不斷擴大

During the forecast period, the market for tungsten carbide is expected to register a moderate rate of about 3.5% per year.

The COVID-19 epidemic had a mixed influence on the tungsten carbide market. On the one hand, demand from the medical sector caused a significant increase in the market, but on the other hand, the market suffered a negative influence from other industries due to statewide lockdowns and stringent limitations.

Key Highlights

- Growth in manufacturing activities across the globe is generating demand for tungsten carbide. Along with it, tungsten carbide scrap can be recycled, making it an extremely valuable alloy for all sorts of applications and thus positively influencing the market.

- On the other hand, toxicity brought on by the use of tungsten carbide restricts market expansion.

- The increasing demand for automatic valves in the business world is probably going to support the growth of the market under study.

- The Asia-Pacific region is expected to have the biggest share of the market and the highest CAGR over the next five years.

Tungsten Carbide Market Trends

Cement Carbide to Drive the Market Growth

- Cemented carbide is a powdered metallurgical material composed of tungsten carbide particles and a binder rich in metallic cobalt.

- Cement carbide is considered the best material choice and is often used because of its unique physical and mechanical properties, such as abrasion resistance, deflection resistance, tensile strength, compressive strength, and high-temperature wear resistance.

- The tools that are used to make glass bottles, aluminum cans, plastic tubes, steel wires, and copper wires are made of cemented carbide.Some of the other uses include metal cutting, machining of wood, plastics, composites, soft ceramics, chipless forming (hot and cold), mining and construction, structural parts, wear parts, and military components.

- According to the Bureau of Economic Analysis, the total value added by the construction industry in the United States in the first three quarters of 2022 was around USD 2,980 billion, which was roughly 5% higher than the previous year for the same period. The primary function of cement carbide is in the tools used in industry to provide properties that no other material can provide.

- The mining industry also saw a major upsurge of approximately 30% in the value added by the industry in the first three quarters of 2022, which was about USD 1,490 billion compared with the previous year for the same period.

- Due to the properties that it possesses, which give it an edge over other tools and thus increase demand from various applications, the market for cement carbide is projected to grow over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific represents the largest regional market for the global tungsten carbide market. There is demand for tungsten carbide in the market as a result of the growing demand for the automotive, construction, and metalworking industries in countries like China, India, and Japan.

- The Asia-Pacific region dominated the global market share. With growing transportation activities in countries such as China, India, and Japan, the usage of tungsten carbide is increasing in the region.

- China is the largest producer and consumer of automotive vehicles. The China Association of Automobile Manufacturers reports that, compared to the prior year, China's automobile sales increased by about 2.1% in 2022. In comparison to the 26.27 million automobiles sold in 2021, around 26.86 million were sold in 2022.

- In its annual report for 2022, the Philippine Statistics Authority also said that the country's 7.6% GDP growth over the previous year was helped a lot by the maintenance of cars and motorbikes. The sector was the most important contributor, providing approximately 8.7% of overall growth.

- The overall production value of the electronics sector in Japan was estimated by the Japan Electronics and Information Technology Industries Association (JEITA) to be around JPY 10.1 trillion (84.5 billion USD) as of November 2022, which is roughly 100.7% of the value from the previous year. When compared to the previous year, Japanese electronics exports increased by nearly 15% up until November.

- Furthermore, the mineral industry in Japan comprises a modest coal and nonferrous metals mining sector, a significant mining sector of industrial minerals, and a primary minerals-processing sector of ferrous and nonferrous metals and industrial minerals.

- Thus, the growing manufacturing activities, the increasing automobile industry, and the rising electronics sector are instrumental in the growth of cemented carbide and other applications, which in turn would boost the market for tungsten carbide during the forecast period.

Tungsten Carbide Industry Overview

The global tungsten carbide market is fragmented. The major companies include (not in any particular order) Umicore, CERATIZIT S.A., Extramet Products, LLC, Kennametal Inc., and American Elements, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Applications of Tungsten Carbide in Various End-user Industries

- 4.1.2 Recylable Property of Tungsten carbide

- 4.2 Restraints

- 4.2.1 Toxicity of Tungsten carbide

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Cemented carbide

- 5.1.2 Coatings

- 5.1.3 Alloys

- 5.2 End-user

- 5.2.1 Aerospace & Defense

- 5.2.2 Automotive

- 5.2.3 Mining & Construction

- 5.2.4 Electronics

- 5.2.5 Others (Medical, Sports, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Elements

- 6.4.2 Buffalo Tungsten Inc.

- 6.4.3 CERATIZIT S.A.

- 6.4.4 China Tungsten

- 6.4.5 CY Carbide Mfg. Co., Ltd.

- 6.4.6 Extramet Products, LLC.

- 6.4.7 Federal Carbide Company

- 6.4.8 Guangdong Xianglu Tungsten Co., Ltd.

- 6.4.9 H.C. Starck Tungsten GmbH

- 6.4.10 Jiangxi Yaosheng Tungsten Co., Ltd.

- 6.4.11 Kennametal Inc.

- 6.4.12 Sandvik AB

- 6.4.13 Sumitomo Electric Industries, Ltd.

- 6.4.14 Umicore

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand for Automatic Valves