|

市場調查報告書

商品編碼

1433771

照明控制系統:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Lighting Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

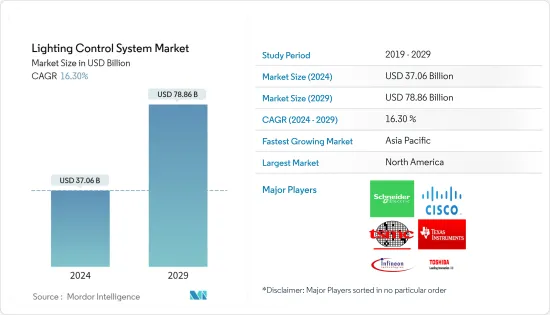

2024 年照明控制系統市場規模估計為 370.6 億美元,預計到 2029 年將達到 788.6 億美元,在預測期間(2024~2029 年)以 16.30% 的複合年增長率增長。

隨著智慧型手機和平板電腦等智慧型裝置的使用增加,市場正朝著採用物聯網 (IoT) 的方向發展。隨著照明控制市場在物聯網連接設備中的應用,其採用正在影響市場的正面成長。

主要亮點

- 連接性的增強和技術解決方案的進步正在增加全球智慧照明控制系統的採用。 ZigBee 和藍牙等無線技術使得在各種空間無縫安裝智慧照明控制系統成為可能。

- 此外,智慧城市的概念也在各個地區不斷興起,這項運動得到了許多政府措施的支持。由於智慧城市由互聯系統組成,因此智慧城市中的常見照明應用需要自動化照明系統。這些自動照明系統使用基於感測器的控制系統。

- 例如,2018年4月,澳洲政府能源部長理事會宣布將以LED燈取代鹵素燈,以提高能源效率。

- 然而,另一方面,無線連接可能不可靠,持續的維護是阻礙整體市場成長的因素。初始安裝成本也很高,這是大規模實施照明控制系統時的一個主要問題。

照明控制系統市場趨勢

智慧城市發展措施將推動智慧照明市場

- 根據聯合國人類居住規劃署的數據,城市消耗了全球78%的能源,飛利浦也預測,由於都市化,到2050年,66%的人口將居住在城市。這些都使得智慧城市依賴物聯網,一切都相互依存的智慧城市。從路燈到交通燈等等。智慧照明可以成為智慧城市網路的支柱。

- 如今,大多數城市安裝新的智慧照明或維修現有設施都選擇已經配備感測器技術或可以輕鬆升級以利用物聯網應用的系統。

- 例如,2018 年 2 月,倫敦致力於實施創新照明策略,利用智慧照明來減少能源和光污染,管理一天中不同時間的光照水平和顏色。

亞太地區複合年成長率最快

- 亞太地區的成長得益於該地區(主要是中國)快速的基礎設施建設活動,其中照明控制系統正在為基礎設施現代化鋪平道路。不斷成長的能源需求,尤其是來自中國和印度等新興國家的能源需求,長期來看預計將消耗更多的能源。照明部分通常消耗商業建築中的大部分電力以及私人住宅中的大量能源。

- 另外,中國、印度和台灣等新興國家也越來越意識到連網型照明系統的效率,透過最佳化能源消耗來大幅節省成本。

- 印度正積極從使用傳統照明轉向LED和節能智慧燈。隨著這項變化,印度被國內外製造商視為一個具有巨大潛力的市場。

- 根據ELCOMA報告,照明產業將透過引入更多節能產品以及與政府更緊密地合作開展各種規劃和宣傳電力消耗量,預計將減少18%到2020 年,這一比例將達到 13%。

照明控制系統產業概況

照明控制系統市場高度分散,各大公司林立。市場的主要企業包括德州儀器 (TI)、施耐德電機 (Schneider Electric SE)、飛利浦 (Philips NV) 和英飛凌 (Infineon Technologies)。產品推出、高額研發投入、合作與收購等是這些公司維持智慧照明控制市場激烈競爭的主要成長策略。

- 2018 年 6 月 - 霍尼韋爾推出一套下一代能源管理軟體、智慧照明、語音控制和安全通訊系統。這些技術使酒店業能夠完全整合能源管理、安全和安保系統、資產管理和品牌網路營運,以實現世界一流的客房和建築自動化。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究成果

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素與市場約束因素介紹

- 市場促進因素

- 對節能照明系統的需求不斷成長

- 現代化和基礎設施發展取得進展

- 市場限制因素

- 安裝成本高

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 依類型

- LED驅動器

- 開關和調光器

- 繼電器單元

- 閘道

- 依通訊協定

- 有線

- 無線的

- 依用途

- 室內的

- 戶外的

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第6章 競爭形勢

- 公司簡介

- General Electric Company

- Philips Lighting NV

- Eaton Corporation PL

- Honeywell International Inc.

- Acuity Brands Inc.

- Cree Inc.

- Lutron Electronics Co. Inc.

- Leviton Manufacturing Company Inc.

- Digital Lumens Inc.

- WAGO Corporation

- Infineon Technologies

- Schneider Electric

- Cisco Systems Inc.

- Taiwan Semiconductor

- Toshiba

第7章 投資展望

第8章 市場機會及未來趨勢

The Lighting Control System Market size is estimated at USD 37.06 billion in 2024, and is expected to reach USD 78.86 billion by 2029, growing at a CAGR of 16.30% during the forecast period (2024-2029).

The market is moving toward the adoption of the Internet of Things (IoT), with the increasing usage of smart devices, such as smartphones, tablets, etc. As the lighting control market is finding its applications in IoT-connected devices, the increase in adoption is influencing a positive growth of the market.

Key Highlights

- The improved connectivity and advancements in technologies solutions have increased the adoption of smart lighting controlling system, globally. Wireless technologies, such as ZigBee and bluetooth, have made installations of smart lighting controlling system seamless across various spaces.

- Moreover, the concept of smart cities is also increasing in different regions and this movement is supported by many government initiatives. As a smart city consists of a connected system, the general lighting application in the smart city requires automated lighting systems. These automated lighting systems use sensor-based control systems.

- For instance, in April 2018, the Council of Australian Governments Energy Ministers have announced to replace halogen lamps with LED lamps to improve energy efficiency.

- However, on the flip side, wireless connections can be unreliable at times and ongoing maintenance are the factors hampering the overall growth of the market. The initial set up cost is also high, which is a major challenge in the large-scale adoption of lighting control systems.

Lighting Control System Market Trends

Smart City Development Initiatives to Drive the market for Smart Lighting

- According to the United Nations Human Settlements Program, cities consume 78% of the world's energy and Philips also predicted that by 2050, 66% of the population may live in cities, due to urbanization. These have resulted in smart cities, where smart cities rely on IoT, where everything is dependent on each other. From streets lights to traffic signals and beyond. Smart lighting can be a backbone for a smart city network.

- Nowadays, most cities that install new smart lighting or retrofit existing fixtures choose systems that already are equipped with sensor technology or that can be upgraded easily to utilize the advantages of IoT applications.

- For instance, in February 2018, London worked on an innovative lighting strategy that would use smart lighting to cut energy and light pollution, and manage light levels and color at different times of the day.

Asia-Pacific to Witness the Fastest CAGR

- The growth in Asia-Pacific is attributed to the rapid infrastructure building activities being undertaken in the region, mainly in China where lighting control systems pave the way for the modernization of infrastructure. It is anticipated to consume more energy resources in the longer run, especially with the growing energy demand from the developing countries, such as China and India. The lighting segment usually consumes the majority of the electricity in a commercial building and draws substantial energy levels for a private residence.

- Apart from this the increasing awareness regarding the efficiency of the connected lighting system in the emerging countries, like China, India, and Taiwan, is enabling significant cost savings through optimal energy consumption.

- India is making an affirmative shift from using conventional lighting to LED and energy efficient smart lights. Due to this change, India is perceived as a market with great potential for international and domestic manufacturers alike.

- According to a report by ELCOMA, the lighting industry is expected to reduce energy consumption for lighting from the present 18% of total power consumption to 13% by 2020, by introducing more energy efficient products and working more closely with the government to execute various schemes and awareness programs.

Lighting Control System Industry Overview

The lighting control system market is highly fragmented because of the presence of major players. Some of the key players in the market areTexas Instruments Incorporated,Schneider Electric SE,Philips NV,and Infineon Technologies, among others. Product launches, high expense on research and development, partnerships and acquisitions, etc. are the prime growth strategies adopted by these companies to sustain the intense competition in the intelligent lighting controls market.

- June 2018 -Honeywelllaunched a suite of next-generation energy management software, smart lighting, voice controls, and secure cloud communication systems. With these technologies, the hospitality industry can fully integrate energy management, safety and security systems, property management, and brand network operations for world-class guestroom and building automation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Growing Demand For Energy-efficient Lighting Systems

- 4.3.2 Growing Modernization And Infrastructural Development

- 4.4 Market Restraints

- 4.4.1 High Cost of Installation

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 LED Drivers

- 5.1.1.2 Sensors

- 5.1.1.3 Switches and Dimmers

- 5.1.1.4 Relay Units

- 5.1.1.5 Gateways

- 5.1.2 Software

- 5.1.1 Hardware

- 5.2 By Communication Protocol

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.3 By Application

- 5.3.1 Indoor

- 5.3.2 Outdoor

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Latin America

- 5.4.4.2 Middle-East & Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 General Electric Company

- 6.1.2 Philips Lighting NV

- 6.1.3 Eaton Corporation PL

- 6.1.4 Honeywell International Inc.

- 6.1.5 Acuity Brands Inc.

- 6.1.6 Cree Inc.

- 6.1.7 Lutron Electronics Co. Inc.

- 6.1.8 Leviton Manufacturing Company Inc.

- 6.1.9 Digital Lumens Inc.

- 6.1.10 WAGO Corporation

- 6.1.11 Infineon Technologies

- 6.1.12 Schneider Electric

- 6.1.13 Cisco Systems Inc.

- 6.1.14 Taiwan Semiconductor

- 6.1.15 Toshiba

7 INVESTMENT OUTLOOK

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年照明控制系統全球市場報告

2024 年照明控制系統全球市場報告 燈具和照明控制市場(產品:燈具和照明控制;以及光:LED、鹵素燈、螢光燈和 HID)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

燈具和照明控制市場(產品:燈具和照明控制;以及光:LED、鹵素燈、螢光燈和 HID)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 全球燈具和照明控制市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測

全球燈具和照明控制市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測 調光器市場報告:至2030年的趨勢、預測與競爭分析

調光器市場報告:至2030年的趨勢、預測與競爭分析 照明控制:評估 10 家非住宅照明控制製造商的策略和執行 - Guidehouse Insights 排行榜報告

照明控制:評估 10 家非住宅照明控制製造商的策略和執行 - Guidehouse Insights 排行榜報告 無線照明控制解決方案市場:按組件、安裝和應用分類 - 2023-2030 年全球預測

無線照明控制解決方案市場:按組件、安裝和應用分類 - 2023-2030 年全球預測 2023-2030 年按類型(硬體、軟體)、通訊協議(有線、無線)、應用(室內、室外)和地區分析的全球照明控制系統市場規模研究與預測

2023-2030 年按類型(硬體、軟體)、通訊協議(有線、無線)、應用(室內、室外)和地區分析的全球照明控制系統市場規模研究與預測 照明控制系統全球市場規模、份額和行業趨勢分析報告:2023-2030年按應用、組件、技術和地區劃分的展望和預測

照明控制系統全球市場規模、份額和行業趨勢分析報告:2023-2030年按應用、組件、技術和地區劃分的展望和預測 商業·產業建築物照明控制

商業·產業建築物照明控制 照明控制系統市場:各零件,各技術,各用途:全球機會分析與產業預測,2023-2032年

照明控制系統市場:各零件,各技術,各用途:全球機會分析與產業預測,2023-2032年