|

市場調查報告書

商品編碼

1433525

全球導航衛星系統(GNSS)晶片全球市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Global Navigation Satellite System Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

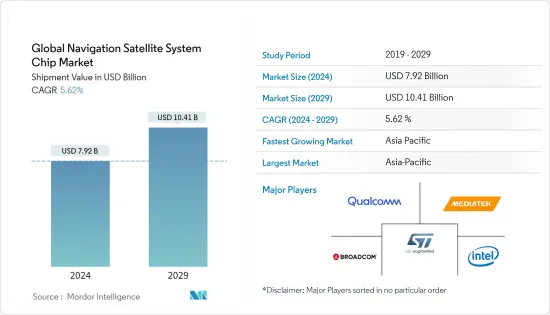

出貨收益,全球全球導航衛星系統(GNSS)晶片市場規模預計到 2024 年為 79.2 億美元,到 2029 年將達到 104.1 億美元,在預測期內不斷成長(2024 年預計將以2029年至2029年年複合成長率為5.62%。

COVID-19 大流行的爆發嚴重擾亂了 2020 年初的半導體供應鏈和生產。對於幾家晶片製造商來說,影響更為嚴重。由於人手不足,亞太地區許多封裝測試工廠已減少或關閉營運。這也造成了依賴半導體的最終產品公司瓶頸。

全球導航衛星系統(GNSS)基本上是指從太空提供訊號並向 GNSS接收器傳輸定位和資料定時的衛星衛星群。接收器使用這些資料並結合多個感測器來確定位置、速度和高度等各種因素。

此類晶片的精度和準確度主要取決於可見範圍內的衛星。因此,多個國家渴望部署區域衛星群以實現更好的導航和測繪。然而,只有中國、俄羅斯、美國、印度、日本和歐盟(EU)五個國家引入了GNSS系統。

GNSS 使用者期望近乎即時的位置共用速度。這對於標準定位來說通常是不可能的,因為它需要識別至少四顆衛星並接收其完整資料。在訊號條件不利或環境惡劣的情況下,資料傳輸和接收可能需要幾分鐘、幾小時甚至失敗。然而,將 GNSS接收器資料與行動網路單元的資訊整合可以提高效能,並使物聯網產業的許多應用受益。

2021 年 1 月,U-Blox 推出了 ALEX-R5 模組,在系統級封裝中整合了低功耗廣域 (LPWA) 蜂窩通訊和 GNSS 技術。這兩個關鍵要素是該公司具有安全雲端功能的 UBX-R5 LTE-M/NB-IoT 晶片組和 U-Blox M8 GNSS 晶片,可為醫療保健應用提供足夠的定位精度。

由於配備導航和定位功能的消費性電子產品數量不斷增加,對低功耗 GNSS 晶片的需求預計將大幅增加。目前,技術先進的穿戴式設備的需求呈趨勢。目前,全球近 50% 的人口使用技術先進的穿戴式設備,例如健身手環和智慧型手錶。 GNSS 晶片主要嵌入在這些設備中,為使用者提供精確的位置訊息,並在跑步、步行或駕駛時與親人保持聯繫。

2020年8月,SONY發布了一款用於物聯網和穿戴式裝置的高精度GNSS接收LSI。新LSI支援傳統的L1頻段接收和L5頻段接收,目前正在GNSS衛星群之間擴展,使其適合雙頻段定位。

全球GNSS晶片市場趨勢

智慧型手機領域可望佔據較大市場佔有率

儘管歐盟 28 國、北美和中國等成熟市場已高度飽和,但智慧型手機出貨仍持續超過使用 GNSS 晶片的設備。智慧型手機使用 GNSS 晶片已經有一段時間了。在大多數情況下,這些晶片支援所有常用的衛星網路,包括 GPS、GLONASS 和 Galileo。然而,與專用導航設備相比,這些解決方案的準確性較低。

此外,智慧型手機硬體市場的一定程度的壟斷也限制了GNSS晶片的實現範圍。在大多數情況下,高通硬體沒有 Broadcom GNNS 晶片,反之亦然。但近年來,這種情況正在改變。

歐盟委員會已核准法規,要求投放市場的新智慧型手機包含衛星和 Wi-Fi定位服務。根據該規定,具有全球導航衛星系統(GNSS)功能的晶片組可能會存取歐盟的伽利略衛星系統,該系統提供精確的定位和授時資訊。八個歐盟國家遵循這項規定並使用與伽利略相容的晶片組。

根據歐洲GNSS機構統計,超過95%的衛星導航晶片組供應市場都支援伽利略的新產品,其中包括博通、高通和聯發科等智慧型手機晶片組製造商。隨著主要 GNSS 晶片組供應商製造支援伽利略的晶片組,以及全球智慧型手機品牌已經將這些晶片組整合到其最新的智慧型手機型號中,預計市場將在預測期內看到進一步的成長機會。

此外,新一代Android智慧型手機配備了高效能全球導航衛星系統(GNSS)晶片,可追蹤雙頻多衛星群資料。從 Android 版本 9 開始,用戶現在可以停用佔空比節能選項,從而提供更高品質的偽距和載波相位原始資料。此外,您現在可以更享受應用 PPP(精確點定位)演算法。本研究旨在評估小米首款搭載博通 BCM47755 的雙頻 GNSS 智慧型手機的 PPP 效能。將小米獲得的效能與單頻智慧型手機三星S8進行比較,凸顯了取得雙頻資料的優勢。小米實現的垂直和水平精度分別為0.51m和6m,而三星實現的精度為水平5.64m和垂直15m。

亞太地區預計將佔據主要市場佔有率

北斗衛星導航系統於 2000 年首次發射,由中國國家太空總署 (CNSA) 營運。 20年後,北斗已有48顆衛星在軌運行。 B1I(1561.098MHz)、B1C(1575.42MHz)、B2a(1175.42MHz)、B2I和B2b(1207.14MHz)、B3I等是北斗衛星(1268.52MHz)發射的訊號。

中國對GNSS的態度與歐洲不同。雖然歐洲有 11 個支持 GNSS 的技術集團得到廣泛認可,涵蓋從消費產品到關鍵基礎設施的各個領域,但中國的情況要複雜得多。主要分為三大領域:工業市場、大眾消費市場、特定市場。

2021年3月11日,中國公佈了「十四五」規劃。該計劃涵蓋未來五年發展的各個方面,展現中國2035年的願景。 「十四五」規劃持續注重研發創新,對中國GNSS產業產生了重大影響。 《規劃》將「深化北斗系統普及利用,推動產業高品質發展」作為國家重要指南計劃提出。此策略將強力推動GNSS產業研發,促進北斗產業化應用,加速關鍵核心技術進步。

此外,韓國太空技術委員會表示,他們希望在2021年之前建立地面測試,在2022年之前建立衛星導航基礎技術,並在2024年之前實現實際的衛星製造。兩顆衛星將被放置在朝鮮半島上空的地球靜止軌道上,使 KPS 成為由七顆衛星星系。

2021 年 2 月,科學、資訊和通訊部累計了6,150 億韓元(5.531 億美元)的太空活動預算,以提高國家製造衛星、火箭和其他關鍵設備的能力。

全球衛星定位系統(GNSS)晶片產業概況

GNSS晶片市場由多家公司組成。從市場佔有率來看,沒有一家公司能夠壟斷市場。重要的公司包括高通科技公司、聯發科技公司和義法半導體公司。市場參與企業正在考慮建立策略夥伴關係和聯盟,以增加市場佔有率。最新進展包括:

- 2021年12月,聯發科宣布,其面向下一代旗艦智慧型手機的5G智慧型手機晶片「天璣9000」已獲得OPPO、Vivo、小米、榮耀等多家智慧型手機品牌作為設備製造商的認可和買入。首款搭載天璣9000的旗艦智慧型手機預計將於2022年第一季上市。處理器支援最新的Wi-Fi、藍牙和GNSS標準,讓智慧型手機用戶體驗無縫通訊。

- 2021年1月-高通科技公司和阿爾卑斯阿爾派宣布推出ViewPose,這是一款基於攝影機的感測和定位設備,支援車道級絕對車輛定位。阿爾卑斯阿爾派採用了Qualcomm Technologies的多種解決方案,包括支援多頻GNSS的Qualcomm Snapdragon汽車5G平台,以及處理多個攝影機影像和視覺增強精確定位(VEPP)軟體的Snapdragon汽車座艙平台。這使得電動前鏡、後鏡、側視鏡、高清地圖群眾外包、蜂窩車聯網 (C-V2X) 的車道級導航以及高級駕駛員輔助系統 (ADAS) 和自動駕駛的車道級導航成為可能。它提供了一種經濟有效的精度解決方案。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

- COVID-19 大流行的市場影響評估

第5章市場動態

- 市場促進因素

- 採用環保運輸解決方案、永續農業和天氣監測

- 對準確即時資料的需求不斷成長

- GNSS 基礎設施的演變,包括新訊號和頻率的出現

- 市場挑戰

- GNSS 無法提供準確的地下、水下和室內導航

- 與高功耗相關的複雜性

第6章 GNSS主要統計數據

- GNSS接收器出貨:依價格類別

- 高階接收器出貨:依價格類別

- GNSS 設備出貨:依軌道子區隔

- 安裝的 GNSS 設備數量:依最終使用者分類

第7章市場區隔

- 設備類型

- 智慧型手機

- 平板電腦和穿戴式裝置

- 個人追蹤裝置

- 低功耗資產追蹤器

- 汽車系統

- 無人機

- 其他設備類型

- 最終用途產業

- 車

- 家用電器

- 航空

- 其他最終用途產業

- 地區

- 北美洲

- 美國

- 歐洲

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 韓國

- 拉丁美洲

- 中東/非洲

- 北美洲

第8章 競爭形勢

- 公司簡介

- Qualcomm Technologies Inc.

- Mediatek Inc.

- STMicroelectronics NV

- Broadcom Inc.

- Intel Corporation

- U-blox Holdings AG

- Thales Group

- Quectel Wireless Solutions Co. Ltd

- Skyworks Solutions Inc.

- Furuno Electric Co. Ltd

- Hemisphere GNSS

- Trimble Inc.

- Sony Group Corporation

第9章投資分析

第10章市場的未來

The Global Navigation Satellite System Chip Market size in terms of shipment value is expected to grow from USD 7.92 billion in 2024 to USD 10.41 billion by 2029, at a CAGR of 5.62% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic significantly disrupted the supply chain and production of semiconductors in the initial phase of 2020. For multiple chipmakers, the impact was more severe. Due to labor shortages, many packages and testing plants in the Asia-Pacific region reduced or even suspended operations. This also created a bottleneck for end-product companies that depend on semiconductors.

Global navigation satellite system (GNSS) essentially refers to the constellation of satellites that provide signals from space, transmit positioning, and data timing to the GNSS receivers. The receivers then use such data to determine various factors, such as location, speed, and altitude, combined with several sensors.

The precision and accuracy of such chips are primarily dependent on the satellites in the visibility range. As a result, multiple countries are eagerly trying to deploy regional constellations for better navigation and mapping. However, in the market, only five countries (China, Russia, the United States, India, and Japan) and the European Union have their GNSS systems.

GNSS users expect near-instantaneous position sharing speeds. This is often impossible with standard positioning as at least four satellites must be identified, and their complete data should be received. In adverse signal conditions or harsh environments, transmitting and receiving data can take minutes, hours, or even fail. However, the performance can be improved by integrating the GNSS receiver data with information from mobile network cells to benefit numerous applications in the IoT industry.

In January 2021, U-Blox announced its ALEX - R5 module, which integrates low-power wide-area (LPWA) cellular communication and GNSS technology into the system-in-package. The two key elements are the company's UBX - R5 LTE - M/NB-IoT chipset with a secure cloud functionality and the U-Blox M8 GNSS chip for adequate location accuracy for healthcare applications.

The increasing volume of consumer electronics equipped with navigation and positioning features is expected to create a considerable demand for low-power GNSS chips. Technologically advanced wearable devices are in the demand trend currently. At present, almost 50% of the global population has been using tech-advanced wearable devices, such as fitness bands and smartwatches. GNSS chips are majorly being integrated into these devices to give precise locations to the user even while running, walking, or driving, allowing them to stay connected with their close ones.

In August 2020, Sony Corporation announced the release of high-precision GNSS receiver LSIs for IoT and wearable devices. The new LSIs support the conventional L1 band reception and L5 band reception, which are currently being expanded across GNSS constellations, making them suitable for dual-band positioning.

Global Navigation Satellite System (GNSS) Chip Market Trends

The Smartphones Segment is Expected to Hold a Significant Market Share

Despite considerable saturation of mature markets, such as EU28, North America, and China, the shipments of smartphones still outnumber devices using GNSS chips. Smartphones have been using GNSS chips for a considerable time. In most cases, these chips support all publicly available satellite networks, such as GPS, GLONASS, Galileo, etc. However, compared to dedicated navigation devices, these solutions were less accurate.

Additionally, a degree of monopoly in the smartphone hardware market limited the scope for GNSS chip installations. Most of the time, Qualcomm hardware does not include Broadcom GNNS chips and vice versa, as they are prime competitors. However, in recent years, this scenario has been changing.

The European Commission has approved a regulation mandating that new smartphones launched in the market will have to include satellite and Wi-Fi location services. According to the regulation, chipsets enabled with the global navigation satellite system (GNSS) capabilities are likely to have access to the EU's satellite system Galileo, which provides accurate positioning and timing information. Eight EU countries have been following this regulation and are using Galileo-compatible chipsets.

According to the European GNSS Agency, over 95% of the satellite navigation chipset supply market supports Galileo in new products, including various manufacturers of smartphone chipsets like Broadcom, Qualcomm, and Mediatek. With leading GNSS chipset providers producing Galileo-ready chipsets and global smartphone brands already integrating these chipsets in their latest smartphone models, the market is expected to have further growth opportunities during the forecast period.

Further, the new generation of Android smartphones is equipped with high-performance global navigation satellite system (GNSS) chips capable of tracking dual-frequency multi-constellation data. Starting from Android version 9, users can disable the duty cycle power-saving option; thus, better quality pseudo-range and carrier phase raw data are available. Also, the application of the Precise Point Positioning (PPP) algorithm has become more enjoyable. This work aims to assess the PPP performance of the first dual-frequency GNSS smartphone produced by Xiaomi equipped with a Broadcom BCM47755. The advantage of acquiring dual-frequency data is highlighted by comparing the performance obtained by Xiaomi with that of a single-frequency smartphone, the Samsung S8. The vertical and horizontal accuracy achieved by Xiaomi is 0.51 m and 6 m, respectively, while those achieved by Samsung is 5.64 m for 15 m for horizontal and vertical.

Asia-Pacific is Expected to Account for a Significant Market Share

BeiDou, first launched in 2000 and operated by the China National Space Administration, is based in China (CNSA). BeiDou has 48 satellites in orbit after 20 years. B1I (1561.098 MHz), B1C (1575.42 MHz), B2a (1175.42 MHz), B2I and B2b (1207.14 MHz), and B3I are among the signals being transmitted by BeiDou satellites (1268.52 MHz).

China's attitude to GNSS differs from that of Europe. While there are 11 widely acknowledged GNSS-enabled technical groupings in Europe, ranging from consumer products to vital infrastructure, the situation in China is far more complicated. There were three broad sectors - industrial market, mass consumer market, and specific market.

On March 11, 2021, China rolled out its 14th five-year plan. It is a plan that touches on all aspects of development over the next five years and presents China's 2035 vision. The 14th Five-Year Plan's persistent emphasis on R&D and innovation substantially impacts China's GNSS industry. "Deepen the promotion and use of BeiDou systems; Promote the industry's high-quality growth" is advocated as a policy guideline in the plan as an important national strategic project. The strategy is expected to signify a boost in the GNSS industry's research and development, promote BeiDou's industrial application and accelerate significant core technology advancements.

Further, the Korean Committee of Space Technology hopes to build a ground test by 2021, fundamental satellite navigation technology by 2022, and actual satellite manufacturing by 2024, according to the Korean Committee of Space Technology. Three satellites will be put in the geostationary orbit above the Korean Peninsula, making the KPS a seven-satellite constellation.

In February 2021, the Ministry of Science and ICT announced a budget of KRW 615 billion (USD 553.1 million) for space activities to increase the country's capacity to create satellites, rockets, and other critical equipment.

Global Navigation Satellite System (GNSS) Chip Industry Overview

The GNSS chip market consists of several players. In terms of market share, none of the players dominate the market. Significant players include Qualcomm Technologies Inc., Mediatek Inc., and STMicroelectronics NV, among others. The market players are considering strategic partnerships and collaborations to expand their market shares. Some of the recent developments in the market are:

- December 2021 - MediaTek announced device maker acceptance and endorsements from some smartphone brands, including OPPO, Vivo, Xiaomi, and Honor, for its Dimensity 9000 5G smartphone chip for next-generation flagship smartphones. The first flagship smartphones powered by the Dimensity 9000 will hit the market in the first quarter of 2022. Since the processor supports the newest Wi-Fi, Bluetooth, and GNSS standards, smartphone users can experience seamless communication.

- January 2021 - Qualcomm Technologies Inc. and Alps Alpine Co. Ltd announced a camera-based sensing and positioning device called ViewPose to support absolute lane-level vehicle positioning. Alps Alpine is leveraging multiple solutions from Qualcomm Technologies like the Qualcomm Snapdragon Automotive 5G platform, which supports Multi-Frequency GNSS and a Snapdragon Automotive Cockpit Platform for processing multiple camera images and Vision Enhanced Precise Positioning (VEPP) software. This provides a cost-effective solution to lane-level accuracy for the electric front, rear- and side-view mirrors, high-definition map crowdsourcing, lane-level navigation for cellular vehicle-to-everything (C-V2X), and advanced driving assistance systems (ADAS) and autonomous driving applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Environment-friendly Transport Solutions, Sustainable Agriculture, and Meteorological Monitoring

- 5.1.2 Increasing Demand for Accurate Real-time Data

- 5.1.3 Evolution of GNSS Infrastructure, such as the Appearance of New Signals and Frequencies

- 5.2 Market Challenges

- 5.2.1 Inability of GNSS to Offer Accurate Underground, Underwater, and Indoor Navigation

- 5.2.2 Complexity Regarding High Power Consumption

6 KEY GNSS STATISTICS

- 6.1 GNSS Receiver Shipments (in billion units), by Price Categories

- 6.2 High-end Receiver Shipments (in million units), by Price Categories

- 6.3 Shipment of GNSS Devices (in thousand units), by Orbital Sub-segment

- 6.4 Installed Base of GNSS Devices (in billion Units) by End User

7 MARKET SEGMENTATION

- 7.1 Device Type

- 7.1.1 Smartphones

- 7.1.2 Tablets and Wearables

- 7.1.3 Personal Tracking Devices

- 7.1.4 Low-power Asset Trackers

- 7.1.5 In-vehicle Systems

- 7.1.6 Drones

- 7.1.7 Other Device Types

- 7.2 End-user Industry

- 7.2.1 Automotive

- 7.2.2 Consumer Electronics

- 7.2.3 Aviation

- 7.2.4 Other End-user Industries

- 7.3 Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.2 Europe

- 7.3.2.1 Russia

- 7.3.3 Asia-Pacific

- 7.3.3.1 China

- 7.3.3.2 Japan

- 7.3.3.3 South Korea

- 7.3.4 Latin America

- 7.3.5 Middle-East and Africa

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Qualcomm Technologies Inc.

- 8.1.2 Mediatek Inc.

- 8.1.3 STMicroelectronics NV

- 8.1.4 Broadcom Inc.

- 8.1.5 Intel Corporation

- 8.1.6 U-blox Holdings AG

- 8.1.7 Thales Group

- 8.1.8 Quectel Wireless Solutions Co. Ltd

- 8.1.9 Skyworks Solutions Inc.

- 8.1.10 Furuno Electric Co. Ltd

- 8.1.11 Hemisphere GNSS

- 8.1.12 Trimble Inc.

- 8.1.13 Sony Group Corporation