|

市場調查報告書

商品編碼

1433900

3D TSV 和 2.5D:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)3D TSV And 2.5D - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

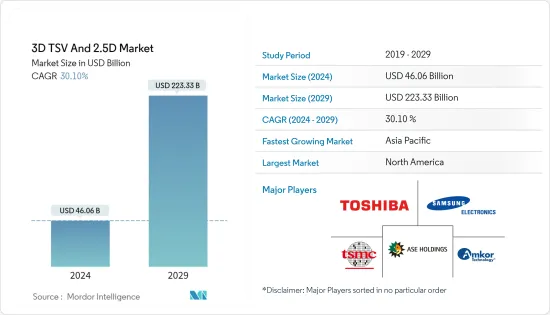

3D TSV和2.5D市場規模預計到2024年為460.6億美元,預計到2029年將達到2233.3億美元,在預測期內(2024-2029年)複合年成長率為30.10%。

半導體產業的封裝正在經歷不斷的變革。隨著半導體應用的成長,CMOS 尺寸縮小和價格上漲迫使該產業依賴IC封裝的進步。 3D堆疊技術是滿足AI、ML和資料中心等應用效能需求的解決方案。因此,在整個預測期內,對高效能運算應用的需求不斷成長將主要推動 TSV(矽穿孔)市場。

主要亮點

- 3D TSV封裝技術也備受關注。這減少了晶片和當前焊線技術之間的資料傳輸時間,從而實現更快的速度並顯著降低功耗。 2022 年 10 月,台積電推出創新3DFabric 聯盟,這是對台積電開放創新平台 (OIP) 的重要介紹,該平台使客戶能夠克服半導體和系統級設計課題中快速增加的障礙。它還可以幫助您使用 TSMC 的 3DFabric 技術快速整合下一代 HPC 和行動技術進步。

- 消費者對電子產品的需求不斷成長,推動了對能夠實現各種新功能的先進半導體裝置的需求。隨著對半導體消費性電子產品的需求持續成長,先進的封裝技術提供了當今數位化世界所需的外形尺寸和處理能力。例如,根據半導體產業協會的數據,2022年8月全球半導體產業銷售額為474億美元,較2021年8月的總合小幅成長0.1%。

- 此外,根據 GSM 協會的數據,到 2025 年,美國預計將擁有世界上最高的智慧型手機普及(連線數的 49%)。根據美國物聯網協會的數據,消費者每個家庭擁有智慧家庭設備的比例最高,並且最有可能擁有跨越兩個或三個用例(能源、安全、電器)的設備。

- 此外,拜登政府將於2022年9月將美國必不可少的全球最先進晶片的產量削減至零,並消耗其中的25%,並宣布將投資500億美元用於研發安全。拜登總統於 2022 年 8 月簽署了價值 2800 億美元的 CHIPS 法案,旨在促進國內高科技製造業,作為其政府推動提高美國對華競爭力的一部分。對半導體產業的如此堅實的投資可能會為所研究市場的成長提供利潤豐厚的機會。

- MEMS 和感測器的成長是由於汽車、工業自動化等多種應用中對感測器和顯示器的需求快速成長。 MEMS製造商和全球半導體產業的主要參與者意法半導體將於2022年8月推出第三代MEMS感測器,專為消費智慧產業、行動裝置、醫療保健和零售業而設計。強大的晶片大小的動作感測器和環境感測器為當今智慧型手機的方便用戶使用和情勢感知功能提供動力,而穿戴式裝置則採用 MEMS 技術製造。 ST 最新一代 MEMS 感測器突破了輸出精度和功耗的技術界限,將性能提升到了新的水平。

- 此外,製造 TSV 裝置的高成本限制了市場的成長。這不僅包括設備的成本,還包括設備正常運作所需的配件和耗材的成本。此外,管理 TSV 裝置製造的嚴格準則和法規也增加了成本。

- 此外,全球半導體短缺促使企業在疫情後專注於擴大產能。例如,中芯國際宣布了雄心勃勃的計劃,透過在多個城市建立自己的晶片製造工廠,到2025年將產能加倍。此外,亞太地區許多地方政府正在透過長期計劃為半導體產業提供資金,市場成長預計將恢復。例如,中國政府已為2030年國家積體電路投資基金第二期引入約230億美元至300億美元資金。

- 此外,俄羅斯和烏克蘭之間持續的衝突預計將對電子產業產生重大影響。這場衝突已經影響該行業一段時間,加劇了半導體供應鏈問題和晶片短缺。這種干擾可能以鎳、鈀、銅、鈦、鋁和鐵礦石等關鍵原料的價格波動的形式出現,導致材料短缺。這給 3D 堆疊記憶體的製造帶來了問題。

3D TSV 和 2.5D 市場趨勢

LED構裝預計將顯著成長

- LED 在產品中的使用越來越多,推動了高功率、高密度、低成本設備的發展。與 2D 封裝不同,採用矽通孔 (TSV) 技術的3D(3D) 封裝可實現高密度垂直互連。

- TSV 積體電路減少了連接長度。因此,如果要有效地結合單晶片和多功能整合以提供高速、低功耗互連,則需要更小的寄生電容、電感和電阻。根據IEA預測,LED在國際照明市場的普及預計在2025年達到約76%,並在2030年進一步達到87.4%。

- 此外,政府採用節能 LED 的措施和法規正在推動所研究的市場。根據國際能源總署(IEA)預測,2025年LED在照明市場的成長率預計為75.8%。

- LED構裝要求可能會進一步提高。如果LED晶片在封裝內放置不準確,會直接影響整個封裝治具的發光效率。任何偏離既定位置的情況都會導致LED光線無法從反光杯完全反射,進而影響LED的亮度。

- 美國能源局最近宣布,將投資 6,100 萬美元實施 10 個先導計畫,利用尖端技術將數千個家庭和企業改造為最先進的節能網路。這也適用於更換白熾燈或鹵素燈泡而採用更節能的 LED 照明時。因此,隨著LED的擴張,美國對LED構裝的需求預計在預測期內將會增加。

- 此外,市場上的各個參與者正在研究的市場中開發新產品。 2022 年 5 月,Lumileds LLC 推出高功率CSP(晶片級封裝)LED。 LUXEON HL1Z 是一款無圓頂單面發送器,可透過尺寸僅 1.4 平方毫米的小盒子提供高發光效率(超過 137 lm/W)。

- LED構裝應用的快速發展預計將在未來幾年增加創新和消費,從而推動所研究市場的成長。另一方面,高飽和度會限制產品的接受度,進而限制市場的成長。

預計亞太地區將佔據主要市場佔有率

- 亞太地區是所研究市場中成長最快的地區。主要由於人口演變和都市化加快,智慧型手機普及不斷上升,使該地區成為世界主要行動市場之一。

- 根據GSM協會統計,智慧型手機寬頻網路覆蓋亞太地區96%的人口,有12億人使用行動網路服務。全部區域的5G 勢頭持續加速,目前已在 14 個市場提供者使用 5G 服務。包括印度和越南在內的其他幾個國家預計也將在未來幾年加入。到 2025 年,全部區域,佔人口的 14% 以上。此外,工業4.0也是亞太地區最新興的趨勢之一。物聯網設備和小型化是利用 3D TSV 的工業 4.0 的主要趨勢。該地區正在大力投資物聯網,以支援智慧城市基礎設施。

- 不斷發展的技術促進了消費性電器產品、電訊、醫療設備、通訊設備和汽車的發展。隨著5G福利在日本的推出,對智慧型手機和其他產品的需求不斷增加。

- 據工信部稱,中國希望在2022年安裝200萬個5G基地台,以發展下一代行動網路。根據工信部統計,目前中國當地已安裝5G基地台142.5萬個,支援全國超過5億用戶,是全球網路最完善的國家。該地區 5G 部署的不斷增加預計也將推動對 5G 設備的需求,從而增加對 2.5D 和 3D 半導體封裝的需求。

- 此外,根據中國資訊通訊研究院的數據,5G智慧型手機出貨量佔國內出貨的75.9%,高於全球平均40.7%。到2022年7月,5G智慧型手機預計將達到中國所有行動電話出貨的74%。到2022年7月,5G行動電話出貨總量將達到1,24mm,中國已推出121款最新5G行動電話。這些趨勢將加速該地區對2.5D和3D半導體封裝解決方案的需求。

- 自動駕駛和電動車的使用不斷增加也增加了全部區域對先進半導體的需求,進一步支持了所研究市場的成長。特斯拉計劃於 2022 年 2 月在中國建造第二座電動車工廠,以滿足國內和出口市場不斷成長的需求。短期內,特斯拉打算將其在中國的產能提高到每年至少1毫米,並計劃在上海臨港自貿區目前的展廳周圍建造第二家工廠。此外,中國政府的目標是到 2025 年電動車佔汽車銷售量的 20%,其中包括採用新能源車作為下一代政府用車。

- 此外,增加對半導體製造和封裝廠的投資也為所研究的市場創造了有利的成長前景。例如,領先的半導體晶片製造商英特爾最近宣布投資70億美元在馬來西亞建造先進的晶片封裝工廠。同樣,2022年11月,日月光半導體工程公司(ASE)宣布投資3億美元擴大在馬來西亞的生產基地。

3D TSV 和 2.5D 產業概述

3D TSV 和 2.5D 市場競爭激烈且多元化,由眾多主要企業組成。市場上小型、大型和本地供應商的存在提供了極好的競爭。這些公司利用策略協作來擴大市場佔有率並提高盈利。市場上的公司也正在收購致力於企業網路設備技術的新興企業,以增強其產品能力。

2022 年 8 月,英特爾公佈了獨特的架構和封裝突破,支援基於 2.5D 和 3D 的晶片設計,開創了晶片製造技術及其重要性的非凡時代。英特爾的系統晶圓代工廠模型採用增強型封裝。該組織的目標是到 2030 年將封裝上的電晶體數量從 1,000 億個增加到 1 兆個。

2022 年 3 月,Apple 採用 2.5D 方法,促進了最新 M1 Ultra 設備的創建,這為未來基於小晶片的設計打開了大門。這種名為 UltraFusion 的封裝架構將矽中介層上的兩個 M1 Max 晶片的晶粒互連起來,創建了系統晶片(SoC)。它利用矽基基板和中介層支援兩個具有 10,000 個互連的晶粒,具有低延遲和 2.5 TB/s 的晶片間頻寬。這也將晶粒連接到以 800 GB/s 介面運行的 128 GB 低延遲統一記憶體。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

- 宏觀經濟走勢對市場的影響

第5章市場動態

- 市場促進因素

- 擴大高效能運算應用市場

- 資料中心和儲存設備的擴展

- 市場課題

- IC封裝單價較高

第 6 章 技術概覽

第7章市場區隔

- 依包裝類型

- 3D堆疊內存

- 2.5D內插器

- 帶有 TSV 的 CIS

- 3D SoC

- 其他封裝類型(LED、MEMS 和感測器等)

- 依最終用戶使用情況

- 消費性電子產品

- 車

- 高效能運算 (HPC) 和網路

- 其他最終用戶用途

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 東南亞

- 其他亞太地區

- 世界其他地區

- 北美洲

第8章 競爭形勢

- 公司簡介

- Toshiba Corp.

- Samsung Electronics Co. Ltd.

- ASE Group

- Taiwan Semiconductor Manufacturing Company Limited

- Amkor Technology, Inc.

- Pure Storage Inc.

- United Microelectronics Corp.

- STMicroelectronics NV

- Broadcom Ltd.

- Intel Corporation

- Jiangsu Changing Electronics Technology Co. Ltd.

第9章投資分析

第10章市場的未來

The 3D TSV And 2.5D Market size is estimated at USD 46.06 billion in 2024, and is expected to reach USD 223.33 billion by 2029, growing at a CAGR of 30.10% during the forecast period (2024-2029).

Packaging in the semiconductor industry has noticed a continuous transformation. As the semiconductor applications are growing, the slowdown in CMOS scaling and escalating prices have forced the industry to rely on the advancement in IC packaging. 3D stacking technologies are the solution that meets the required performance of applications like AI, ML, and data centers. Therefore, the growing requirement for high-performance computing applications mainly drives the TSV (Through Silicon Via) market over the forecast period.

Key Highlights

- The 3D TSV packaging technology is also achieving traction. It reduces data transmission time between chips and the current wire bonding technology, resulting in significantly lower power consumption with faster speed. In October 2022, TSMC announced the launch of the creative 3DFabric Alliance, a considerable introduction to TSMC's Open Innovation Platform (OIP) to help customers overcome the surging hurdles of semiconductor and system-level design challenges. It will also help in gaining rapid integration of advancements for next-generation HPC and mobile technologies using TSMC's 3DFabric technologies.

- Increasing consumer demand for electronics has sparked the need for advanced semiconductor devices that enable various new capabilities. As the demands for semiconductor appliances intensify consistently, advanced packaging techniques deliver the form factor and processing power required for today's digitized world. For instance, according to the Semiconductor Industry Association, during August 2022, global semiconductor industry sales were USD 47.4 billion, a slight boost of 0.1% over the August 2021 total of USD 47.3 billion.

- In addition, according to the GSM Association, by 2025, the United States is expected to have the highest smartphone adoption globally (49% of connections). As per the United States IoT Association, it has the highest smart home device ratio per household and the most significant consumer tendency to own appliances across two or three use cases (energy, security, and appliances).

- Moreover, in September 2022, the Biden administration announced that it would invest USD 50 billion in building up the domestic semiconductor industry to counter dependency on China, as the US produces zero and consumes 25% of the world's leading-edge chips vital for its national security. President Joe Biden signed a USD 280 billion CHIPS bill in August 2022 to boost domestic high-tech manufacturing, part of his administration's push to increase US competitiveness over China. Such robust investments in the semiconductor sector would present lucrative opportunities for the growth of the studied market.

- The growth of MEMS and Sensors is attributed to the rapidly increasing demand for sensors and displays in various applications such as automotive, industrial automation, and many others. In August 2022, STMicroelectronics, a maker of MEMS and a significant player in the worldwide semiconductor industry, launched its third generation of MEMS sensors designed for consumer smart industries, mobile devices, healthcare, and retail sectors. The robust, chip-sized motion and environmental sensors power the user-friendly, context-aware features of today's smartphones, and wearables are made on MEMS technology. ST's most recent MEMS sensor generation drives technical boundaries regarding output accuracy and power consumption, elevating performance to a new level.

- Furthermore, the high costs associated with TSV device manufacturing restrict market growth. This includes not only the cost of devices but also the cost of accessories and consumables needed for their proper functioning. Moreover, the stringent guidelines and regulations governing TSV device manufacturing also add to the charges.

- Furthermore, the worldwide semiconductor shortage encouraged players to focus on expanding production capacity during a post-pandemic. For instance, the SMIC announced aggressive plans to double its production capacity by 2025 by constructing unique chip fabrication plants in different cities. Also, many Asian-Pacific local governments have funded the semiconductor industry in a long-term program, hence anticipated to regain market growth. For instance, the Chinese government introduced roughly USD 23-30 billion to pay for the second stage of its National IC Investment Fund 2030.

- Moreover, the ongoing conflict between Russia and Ukraine is expected to impact the electronics industry significantly. The conflict has already exacerbated the semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may come in the form of volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, aluminum, and iron ore, resulting in material shortages. This would obstruct the manufacturing of 3D Stacked Memory.

3D TSV And 2.5D Market Trends

LED Packaging Expected to Witness the Significant Growth

- The increasing use of LED in products has promoted the expansion of higher power, greater density, and lower-cost devices. Using three-dimensional (3D) packaging through silicon via (TSV) technology authorizes a high density of vertical interconnects, unlike 2D packaging.

- TSV integrated circuits reduce connection lengths; thus, smaller parasitic capacitance, inductance, and resistance are required where a combination of monolithic and multifunctional integration is done efficiently, providing high-speed, low-power interconnects. According to IEA, the penetration rate of LEDs into the international lighting market is expected to reach some 76% in 2025 and further to 87.4% in 2030.

- Further, government initiatives and rules to adopt energy-efficient LEDs drive the studied Market. According to the International Energy Agency (IEA), the growth rate of LEDs in the lighting market is anticipated to be 75.8% in 2025.

- The requirements for LED packaging could be much better. If LED chips are not positioned into the package precisely, the luminescence efficiency of the overall packaging appliance might be affected directly. Any deviation from the established position will prevent LED light from being fully reflected from the reflective cup, affecting the LED's brightness.

- The US Department of Energy recently announced investing USD 61 million in 10 pilot projects using the latest technologies to turn thousands of homes and businesses into cutting-edge, energy-efficient networks. This applies to switching out incandescent and halogen bulbs for better energy-efficient LED lighting. As a result, with the expansion in LEDs, the LED packaging need in the United States will grow in the forecasted period.

- Furthermore, various players in the market are developing new products in the studied Market. In May 2022, Lumileds LLC launched high-power CSP (chip-scale package) LED. The LUXEON HL1Z is an un-domed, single-sided emitter that delivers high luminous efficacy (137lm/W or more) from a tiny box, just 1.4mm square.

- Rapid advancements in LED package applications are projected to raise innovation and consumption in the coming years, propelling the studied market growth. On the other hand, high saturation may limit product acceptance, which, in turn, limits market growth.

Asia-Pacific is Expected to Hold the Significant Market Share

- Asia-Pacific is the significant-growing region in the Market studied. The rising smartphone adoption rates have made the region one of the major mobile markets in the world, primarily due to the increasing population evolution and urbanization.

- As per the GSM Association, smartphone broadband networks cover 96% of the population of APAC, with 1.2 billion people accessing mobile internet services. 5G momentum continues revving across the region, with commercial 5G services currently available across 14 markets. Several others, including India and Vietnam, are expected to board in the coming years. By 2025, there will be 400 million 5G connections across the region, over 14% of the population. Further, industry 4.0 is also one of Asia-Pacific's most emerging trends. IoT devices and miniaturization are important trends in Industry 4.0, utilizing 3D TSV. The region is investing heavily in IoT to support smart city infrastructure.

- Advancing technologies have contributed to the development of consumer electronics, telecom, medical devices, communication devices, and automotive. With the launch of 5G benefits in the country, the demand for smartphones, among other things, has been rising.

- According to the MIIT, China desired 2 million installed 5G base stations in 2022 to develop the country's next-generation mobile network. The Chinese mainland presently has 1.425 million installed 5G base stations that support more than 500 million 5G users nationally, making it the most comprehensive network in the world, as per MIIT. The growing implementation of 5G in the region is also expected to promote the demand for 5G-enabled devices, thereby increasing the need for 2.5D and 3D semiconductor packaging.

- Further, according to CAICT, 5G smartphone shipments are recorded for 75.9% of domestic shipments, more significant than a global average of 40.7%. By July 2022, 5G smartphones will have reached 74% of all cellphone shipments in China. The total number of 5G cell phone shipments by July 2022 was 124mm units, and China introduced 121 latest 5G mobile phone models. Such trends would accelerate the region's demand for 2.5D and 3D semiconductor packaging solutions.

- The increasing use of autonomous and electric vehicles has also increased the demand for advanced semiconductors across the region, further supporting the studied Market's growth. In February 2022, Tesla plans to build a 2nd EV facility in China to keep up with rising demand locally and in export markets. In the short term, Tesla intends to increase capacity in China to at least 1mm cars yearly, with a second plant planned around its present exhibition in Shanghai's Lingang free trade zone. In addition, the Chinese government seeks 20% of all vehicle sales to be electric by 2025, including adopting NEVs as the next generation of government vehicles.

- Moreover, the growing investments in semiconductor manufacturing and packaging plants also create a favorable growth scenario for the studied Market. For instance, Intel, a significant semiconductor chip manufacturer, recently announced a USD 7 billion investment to build an advanced chip packaging facility in Malaysia. Similarly, in November 2022, Advanced Semiconductor Engineering (ASE) announced a USD 300 million investment to expand its production site in Malaysia.

3D TSV And 2.5D Industry Overview

The 3D TSV and 2.5D market is highly competitive and consists of various significant performers as it is diversified. The existence of small, large, and local vendors in the Market creates excellent competition. These firms leverage strategic collaborative endeavors to expand their market share and increase profitability. The companies in the Market are also acquiring start-ups performing on enterprise network equipment technologies to strengthen their product capabilities.

In August 2022, Intel showcased the unique architectural and packaging breakthroughs that help 2.5D and 3D-based chip designs, ushering in a remarkable era in chipmaking technologies and their importance. Intel's system foundry model features enhanced packaging. The organization intends to improve the number of transistors on a package from 100 billion to 1 trillion by 2030.

In March 2022, Apple adopted a 2.5D approach to boost the enactment of its latest M1 Ultra device that unlocks the door to future designs utilizing chiplets. A packaging architecture called UltraFusion interconnects the die of two M1 Max chips on a silicon interposer to build a system on a chip (SoC) with 114bn transistors. This utilizes a silicon substrate and interposer that supports the two dies with 10,000 interconnects with 2.5 TB/s of low latency and inter-processor bandwidth between the die. This also connects the die to 128 GB of low-latency unified memory operating an 800 GB/s interface.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Expanding Market for High Performance Computing Application

- 5.1.2 Expanding Scope of Data Centers and Memory Devices

- 5.2 Market Challenges

- 5.2.1 High Unit Cost of IC Packages

6 TECHNOLOGICAL SNAPSHOT

7 MARKET SEGMENTATION

- 7.1 By Packaging Type

- 7.1.1 3D Stacked Memory

- 7.1.2 2.5D Interposer

- 7.1.3 CIS with TSV

- 7.1.4 3D SoC

- 7.1.5 Other Packaging Types ( LED, MEMS & Sensors, etc.)

- 7.2 By End User Application

- 7.2.1 Consumer Electronics

- 7.2.2 Automotive

- 7.2.3 High Performance Computing (HPC) and Networking

- 7.2.4 Other End User Applications

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 U.S.

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 United Kingdom

- 7.3.2.2 Germany

- 7.3.2.3 France

- 7.3.2.4 Italy

- 7.3.2.5 Rest of Europe

- 7.3.3 Asia-Pacific

- 7.3.3.1 China

- 7.3.3.2 India

- 7.3.3.3 Japan

- 7.3.3.4 Australia

- 7.3.3.5 South East Asia

- 7.3.3.6 Rest of Asia-Pacific

- 7.3.4 Rest of the World

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Toshiba Corp.

- 8.1.2 Samsung Electronics Co. Ltd.

- 8.1.3 ASE Group

- 8.1.4 Taiwan Semiconductor Manufacturing Company Limited

- 8.1.5 Amkor Technology, Inc.

- 8.1.6 Pure Storage Inc.

- 8.1.7 United Microelectronics Corp.

- 8.1.8 STMicroelectronics NV

- 8.1.9 Broadcom Ltd.

- 8.1.10 Intel Corporation

- 8.1.11 Jiangsu Changing Electronics Technology Co. Ltd.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2024-2032 年按類型、組件(矽通孔、玻璃通孔、矽中介層)、應用、最終用戶和地區分類的 3D IC 市場

2024-2032 年按類型、組件(矽通孔、玻璃通孔、矽中介層)、應用、最終用戶和地區分類的 3D IC 市場 ToF 3D 相機 IC 市場報告:2030 年趨勢、預測與競爭分析

ToF 3D 相機 IC 市場報告:2030 年趨勢、預測與競爭分析 3D TSV 市場:按產品、最終用戶分類 - 2024-2030 年全球預測

3D TSV 市場:按產品、最終用戶分類 - 2024-2030 年全球預測 全球 3D IC 市場規模研究與預測,按類型、組件(矽通孔、玻璃通孔、矽中介層)、應用、最終用戶和區域分析,2023-2030 年

全球 3D IC 市場規模研究與預測,按類型、組件(矽通孔、玻璃通孔、矽中介層)、應用、最終用戶和區域分析,2023-2030 年 3D IC 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、組件(矽通孔、玻璃通孔和矽中介層)、按應用、最終用戶、地區、競爭細分, 2018-2028

3D IC 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、組件(矽通孔、玻璃通孔和矽中介層)、按應用、最終用戶、地區、競爭細分, 2018-2028 3D IC的全球市場:趨勢,機會,競爭分析(2023年~2028年)

3D IC的全球市場:趨勢,機會,競爭分析(2023年~2028年) 3D IC 市場:按類型、按組件(TSV、TGV、Si 中介層)、按應用、按最終用戶、按地區,2023-2028 年

3D IC 市場:按類型、按組件(TSV、TGV、Si 中介層)、按應用、按最終用戶、按地區,2023-2028 年 3D晶片(3D IC的)全球市場 2023

3D晶片(3D IC的)全球市場 2023