|

市場調查報告書

商品編碼

1404307

智慧水錶:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Smart Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

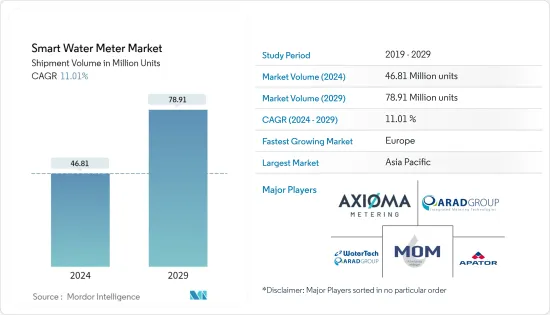

根據出貨量計算,智慧水錶市場規模預計將從2024年的4,681萬台擴大到2029年的7,891萬台,出貨期間(2024-2029年)複合年成長率為11.01%。

智慧水錶是一種準確監測用水量的電子設備。這些智慧電錶可以透過行動電話、射頻電磁 (RF) 和通訊傳輸使用資料,幫助公用事業公司有效管理能源消費量。智慧電錶具有許多好處,包括降低抄表成本、防止停水、消除申請效率低以及降低企業和消費者的重新連接成本。

主要亮點

- 由於人口成長、都市化和工業化的快速發展以及人均消費量的增加,消費量每年都在大幅增加。例如,根據美國草坪養護服務供應商LawnStarter的數據,2022年美國人均消費量位居榜首(2,842立方公尺),其次是加拿大、紐西蘭和哥斯大黎加等國家。

- 近年來,隨著消費量的增加,一些地區開始面臨水資源短缺的問題,需要最大限度地減少水的浪費。預計節水需求的成長將成為預測期內調查市場的主要促進因素。此外,技術進步和政府、私人消費者和企業加大節水力度也促進了市場成長。

- 最近的創新也增強了智慧水錶的功能,使其能夠測量水的特性,例如使用情況、流量、pH 平衡和水質。許多現代智慧水錶還能夠計算每月水費,為消費者提供有關消費量和申請模式的詳細資訊。

- 然而,智慧水錶的高成本和由於認知度低而導致的低安裝率對所研究市場的成長構成了重大挑戰。此外,缺乏支援智慧水錶的基礎設施(例如高速連接)也阻礙了成長,特別是在新興市場。

- 由於新冠肺炎 (COVID-19) 疫情的爆發,智慧水錶業務的許多產品已停止生產。然而,隨著 2022 年報告的 COVID-19 病例減少,供應鏈恢復動力,市場預計將成長,導致水錶公司滿載營運。此外,COVID-19大流行對消費者對環境和數位技術的普遍認知產生了重大影響,大流行期間對數位技術的依賴顯著增加。因此,此類趨勢預計將產生長期影響,為預測期內的智慧水錶市場創造良好前景。

智慧水錶市場趨勢

住宅應用領域預計將佔據主要市場佔有率

- 智慧水錶在住宅領域的需求不斷增加,因為它們可以準確、及時地測量消費量,使消費者能夠有效地監控和管理他們的消費量。透過監測消費量,消費者可以確定在哪裡減少消費量並改變他們的習慣以節約用水。

- 智慧水錶技術徹底改變了水的申請方式。傳統水錶根據預計用量向客戶申請,這可能會導致申請不準確和糾紛。智慧水錶可提供準確的讀數,因此住宅只需支付水費,從而實現更公平、更有效率的申請方式。

- 智慧水錶還解決了另一個問題:向公寓中的所有家庭收取相同的申請。這種做法是不公平的,因為有些居民在節約用水,而有些居民則不太重視。如果使用單獨的電錶,每個家庭將根據使用情況單獨申請。

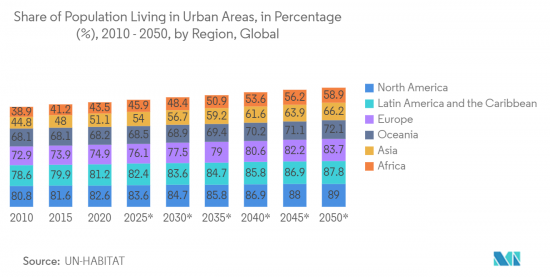

- 此外,大多數國家供水基礎設施的改善正在增加住宅消費量。隨著都市化的加快,住宅消費是智慧水錶未來成長的重大機會。根據聯合國人居署預測,到 2050 年,都市化將增加至 89%。預計到 2050 年,世界全部區域的都市化將提高。

- 此外,一些政府和當局正在推廣智慧水錶在節水和永續性工作中的使用。在一些地區,政府法規強制要求在住宅和重建中安裝智慧水錶,進一步推動市場成長。

歐洲預計將出現顯著成長

- 在預測期內,政府為改善水資源管理而採取的越來越多的舉措正在創造對智慧水錶的需求。此外,由於水資源短缺問題,許多歐洲國家需要更好的水資源管理解決方案,預計將推動市場成長。

- 英國供應商正在推出各種計劃來快速部署智慧水錶。例如,2023 年 2 月,英國水務公司 Anglian Water 宣布已開始探索「端到端」智慧電錶交付解決方案,以繼續推出其安裝計畫。此次合作將使智慧電錶的安裝成為可能。這將使客戶能夠透過使用智慧電錶減少用水量。

- 2023 年 1 月,約克郡水務公司宣佈在智慧電錶技術領域進行重大投資,作為其網路策略承諾的一部分。此次合作預計將支援先進的客戶計量計劃,旨在改善服務並減少洩漏。此外,2023 年 3 月,牛津通過立法,要求在整個牛津安裝智慧水錶。

- 高額水費推動了對智慧水錶的需求。英格蘭和威爾斯的家庭面臨著自 2022 年 4 月以來水費近 20 年來首次大幅上漲,這給已經經歷了生活成本危機的家庭預算帶來了進一步的壓力。據英國水務局稱,從 4 月開始,典型的水費將上漲至平均每年 448 英鎊(565.56 美元),增幅為 7.5%。

- 在歐洲地區新興經濟體之一的法國,飲用水供應的管理部分與傳統水錶相關,例如處理營運成本、因洩漏和其他系統故障而導致的水損失和未計費水量水以及水錶。我們正面臨重大挑戰。法國自來水公司正在安裝智慧水錶,並向客戶免費提供。

智慧水錶產業概況

智慧水錶市場高度分散,主要參與者包括 Watertech SPA (Arad Group)、Mom Zrt、Apator SA、Arad Group 和 Axioma Metering。市場參與者正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 3 月,德國水務公司 ThuWa ThuringenWasser 宣布與代傲表計 (Diehl Metering) 建立策略夥伴關係,安裝新水錶並利用代傲表計 (Diehl Metering) 的 LPWAN mioty 技術。 ThuWa 現在憑藉安全的資料、精確的測量技術和數位化流程變得更加高效和更具成本效益。

- 2023 年 3 月 - Itron Inc. 與 PT. Megalopolis Manunggal Industrial Development (PT. MMID) 簽署協議,以收集 MM2100工業城的資料並提高業務效率。作為協議的一部分,PT.MMID 將實施 Itron 的下一代電錶資料收集和管理解決方案 Temetra。透過這個解決方案,PT.MMID透過統一平台收集頻繁、準確的水錶使用資料,最大限度地減少申請錯誤,並創新和節省資金,符合印尼工業4.0時代的藍圖,我們將予以推廣。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- 智慧水錶類型技術簡介

- 智慧電錶投資報酬率分析

- 使用的主要協議及其比較

- LoraWAN 部署步驟/關鍵使用案例/長期影響

- 公共產業透過實施智慧電錶/數位化所獲得的好處

第5章市場動態

- 市場促進因素

- 政府支持法規

- 需要提高用水量和效率

- 減少無收益水損失的需求不斷增加

- 市場抑制因素

- 高成本和安全問題

- 與智慧電錶整合困難

- 營運商轉換成本

第6章市場區隔

- 依技術

- 自動抄表

- 高度測量基礎設施

- 按用途

- 住宅

- 商業的

- 產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章競爭形勢

- 公司簡介

- Watertech SPA(Arad Group)

- Mom Zrt

- Apator SA

- Arad Group

- Axioma Metering

- Badger Meter Inc.

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Suntront tech Co., Ltd.

- Maddalena SPA

- Waviot

- Itron Inc.

- BETAR Company

- Kamstrup A/S

- Landis+GYR Group AG

- Integra Metering AG

- G. Gioanola Srl

- Sensus Usa Inc.(Xylem Inc.)

- Zenner International Gmbh & Co. KG

第8章投資分析

第9章 市場機會及未來趨勢

The Smart Water Meter Market size in terms of shipment volume is expected to grow from 46.81 Million units in 2024 to 78.91 Million units by 2029, at a CAGR of 11.01% during the forecast period (2024-2029).

Smart water meters are electronic devices that accurately monitor water usage. These smart meters can transmit usage data via cellular, radiofrequency electromagnetic radiation (RF), and power line communication, assisting the utility company in efficiently managing energy consumption. Smart meters provide many advantages, including lower meter reading costs, prevention of disconnection, elimination of billing inefficiencies, and lower reconnection costs for businesses and consumers.

Key Highlights

- Over the years, water consumption has increased significantly due to population growth, rapid urbanization and industrialization rates, and growing per capita consumption. For instance, according to LawnStarter, an American lawn maintenance service provider, the United States was the leading country in per-capita water consumption (2,842 cubic meters) in 2022, followed by countries such as Canada, New Zealand, Costa Rica, etc.

- As a result of the growing consumption, several regions have started facing water shortage issues in recent years, giving rise to the need to minimize water wastage. The growing demand for water preservation is anticipated to be a key driver for the market studied during the forecast period. Moreover, technological advancements and rising efforts by governments, individual consumers, and businesses to save water also contribute to the market's growth.

- Recent innovations have also enhanced the capabilities of smart water meters, enabling them to measure the characteristics of the water, such as the quantity used, its speed of flow, its pH balance, and quality, among others. Many smart water meters nowadays are also capable of calculating monthly water bills, giving consumers detailed information about consumption and billing patterns.

- However, factors such as the higher cost of smart water meters and a lower installation rate, owing to lower awareness, are among the major challenges to the growth of the market studied. Additionally, the lack of supporting infrastructure for smart water meters, such as high-speed connectivity, also hampers the market's growth, especially across developing regions.

- The COVID-19 outbreak halted the production of many items in the smart water meter business. However, as fewer COVID-19 cases were reported in 2022, which resulted in a return of water meter companies operating at total capacity, the market is anticipated to grow as the supply chain regains momentum. Furthermore, a major impact of the COVID-19 pandemic has been on the general awareness of consumers about the environment and digital technologies, as during the pandemic, the reliance of people on digital technologies grew significantly. Hence, such trends are anticipated to have a long-term impact, creating a favorable outlook for the smart water meter market during the forecast period.

Smart Water Meter Market Trends

Residential Application Segment is Expected Hold Significant Market Share

- The demand for smart water meters in the residential segment is increasing as they can accurately and timely measure water consumption, allowing consumers to monitor and manage their water consumption effectively. Consumers can identify areas to reduce consumption and change their habits to save water by monitoring their consumption.

- Smart water meter technology has revolutionized the way water is billed. Traditional water meters bill customers based on estimated usage, which can lead to inaccurate billing and disputes. Smart water meters provide accurate readings, so homeowners only pay for their water, leading to fairer and more efficient billing practices.

- Smart water meters also solve another problem: charging all households in an apartment the same bill. This practice is unfair because some residents conserve water while others pay less attention. With separate meters, each family is billed separately based on usage.

- Moreover, in most countries, residential water consumption is increasing due to improvements in water infrastructure. With the increasing urbanization trend, residential consumption represents a great opportunity for the future growth of smart water meters. According to the UN-HABITAT, urbanization will increase to 89 percent by 2050. Across all major world regions, urbanization is projected to be rising in 2050.

- Additionally, several governments and authorities promote using smart water meters in their water conservation and sustainability efforts. In some regions, there are government regulations mandating the installation of smart water meters in new homes or renovations, further driving market growth.

Europe is Expected to Witness Significant Growth

- The increasing government initiatives for better water management are creating a demand for smart water meters over the forecast period. Moreover, many European countries need better water management solutions due to water scarcity issues, which is expected to drive market growth.

- Vendors in the United Kingdom are launching various programs for faster deployment of smart water meters. For instance, in February 2023, Anglian Water, a water company in the United Kingdom, announced that it started to explore an 'end to end' smart metering delivery solution to continue the rollout of its installation program. The collaboration would deliver the installation of a smart meter installation. This would allow customers to use less water by using smart meters.

- In January 2023, Yorkshire Water announced its significant venture in smart meter technology, a part of the company's strategic commitment throughout its network. The partnership is anticipated to help with its advanced customer metering program to improve services and reduce leakage, in addition to helping customers save some money on their bills. Furthermore, in March 2023, Oxford passed legislation stating that smart water meters are set to be fitted throughout Oxford, and the change is compulsory; residents can not refuse the fitting or modification of the existing meters.

- The hefty water bills drive the demand for smart water meters. Households in England and Wales are facing a rapid increase in water bills in almost two decades since April 2022, putting further pressure on budgets already weathering the cost-of-living crisis. According to Water UK, the typical water bill will increase to an average of GBP 448 (USD 565.56) a year from April, an upsurge of 7.5%.

- One of the developed economies of the European region is France, where the management of drinking water supply is facing critical challenges partly related to a traditional water meter, such as handling operational costs, water loss or non-revenue water due to leaks and other system failures, and water conservation. Smart water meters are increasingly being installed by French water utility companies and made available to users free of charge.

Smart Water Meter Industry Overview

The smart water meter market is highly fragmented, with the presence of major players like Watertech S.P.A (Arad Group), Mom Zrt, Apator SA, Arad Group, and Axioma Metering. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2023, German water utility ThuWa ThuringenWasser announced a strategic collaboration with Diehl Metering to install new water meters and leveraged Diehl Metering's LPWAN mioty technology. ThuWa now benefits from secure data, precise measurement techniques, and digitized processes that increase efficiency and cost-effectiveness.

- March 2023 - Itron Inc. signed an agreement with PT. Megalopolis Manunggal Industrial Development (PT. MMID) to improve data collection and operational efficiencies in MM2100 Industrial Town. As a part of the contract, PT MMID will deploy Temetra, Itron's next-generation meter data collection and management solution. The solution will allow PT. MMID to collect frequent and accurate water meter usage data through a unified platform, minimizing billing errors and driving innovation and conservation that aligns with Indonesia's roadmap to enter the Industry 4.0 era.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot for types of Smart Water Meter

- 4.5 ROI Analysis for Smart Meters

- 4.6 Prominent Protocols Used and their Comparison

- 4.7 Steps Involved in Implementing LoraWAN/Prominent Use-cases/Long-term Implications

- 4.8 Advantages/Digitalization Achieved by Utilities by Smart Meter Implementations

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations

- 5.1.2 Need for Improvement in Water Utility Usage and Efficiency

- 5.1.3 Increasing Demand to Reduce Non-revenue Water Losses

- 5.2 Market Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Utility Supplier Switching Costs

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Automatic Meter Reading

- 6.1.2 Advanced Metering Infrastructure

- 6.2 By Application

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Watertech S.P.A (Arad Group)

- 7.1.2 Mom Zrt

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Axioma Metering

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Honeywell International Inc.

- 7.1.9 Suntront tech Co., Ltd.

- 7.1.10 Maddalena SPA

- 7.1.11 Waviot

- 7.1.12 Itron Inc.

- 7.1.13 BETAR Company

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+GYR Group AG

- 7.1.16 Integra Metering AG

- 7.1.17 G. Gioanola Srl

- 7.1.18 Sensus Usa Inc. (Xylem Inc.)

- 7.1.19 Zenner International Gmbh & Co. KG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

到 2030 年漏水偵測系統市場預測:按類型、模式、應用和地區分類的全球分析

到 2030 年漏水偵測系統市場預測:按類型、模式、應用和地區分類的全球分析 2024-2032 年智慧水錶市場報告(按產品、儀表類型、配置類型(自動抄表、先進計量基礎設施)、組件、應用和區域)

2024-2032 年智慧水錶市場報告(按產品、儀表類型、配置類型(自動抄表、先進計量基礎設施)、組件、應用和區域) 智慧水錶市場報告:2030 年趨勢、預測與競爭分析

智慧水錶市場報告:2030 年趨勢、預測與競爭分析 全球智慧水錶市場

全球智慧水錶市場 美國漏水偵測和維修服務市場規模、佔有率和趨勢分析報告:按技術、按用途、按最終用戶和細分趨勢,2023-2030年

美國漏水偵測和維修服務市場規模、佔有率和趨勢分析報告:按技術、按用途、按最終用戶和細分趨勢,2023-2030年 歐洲智能水錶市場規模:按應用(住宅、商業、公用事業)、按技術(AMI、AMR)、副產品(熱水錶、冷水錶),全球預測:2023-2032 年

歐洲智能水錶市場規模:按應用(住宅、商業、公用事業)、按技術(AMI、AMR)、副產品(熱水錶、冷水錶),全球預測:2023-2032 年 全球智能水錶市場:到 2028 年的預測——按水錶類型、技術(自動抄表、高級計量基礎設施)、組件、水質、應用和區域分析

全球智能水錶市場:到 2028 年的預測——按水錶類型、技術(自動抄表、高級計量基礎設施)、組件、水質、應用和區域分析 智慧自來水儀表的全球市場 - 產業分析,規模,佔有率,成長,趨勢,預測(2022年~2031年)

智慧自來水儀表的全球市場 - 產業分析,規模,佔有率,成長,趨勢,預測(2022年~2031年) 智慧自來水儀表的全球市場:成長,未來展望,競爭分析(2022年~2030年)

智慧自來水儀表的全球市場:成長,未來展望,競爭分析(2022年~2030年) 智慧城市的智慧供水系統

智慧城市的智慧供水系統