|

市場調查報告書

商品編碼

1444350

太陽能逆變器:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Solar PV Inverters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

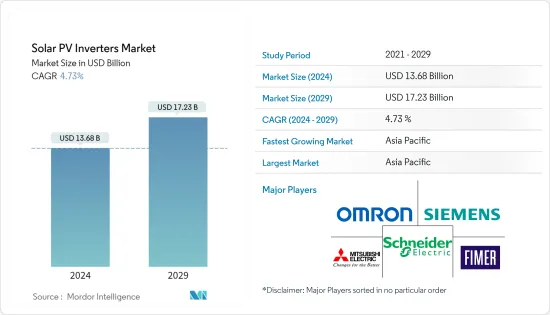

太陽能逆變器市場規模預計到2024年為136.8億美元,預計到2029年將達到172.3億美元,在預測期內(2024-2029年)年複合成長率為4.73%。

所研究的市場在 2020 年受到了 COVID-19 疾病的影響,但現在已恢復並達到大流行前的水平。

太陽能發電需求的成長預計將在預測期內刺激太陽能逆變器市場的成長。不斷增加的投資和雄心勃勃的太陽能目標預計將推動所研究市場的成長。然而,串列型逆變器的技術缺陷預計將阻礙預測期內太陽能逆變器市場的成長。

太陽能逆變器的產品創新和最新技術的採用預計將在預測期內為太陽能逆變器市場創造有利的成長機會。亞太地區在市場上佔據主導地位,預計在預測期內仍將保持最高的年複合成長率。這一成長得益於該地區國家(包括印度、中國和澳大利亞)的投資增加和政府支持政策。

太陽能逆變器市場趨勢

中央逆變器領域預計將主導市場

中央逆變器是一個大型電網饋線。常用於額定輸出100kWp以上的光電發電系統。安裝在地板或地面上的逆變器將從太陽能電池陣列收集的直流電轉換成交流電用於併網。這些設備的容量範圍約為 50kW 至 1MW,可在室內或室外使用。

中央逆變器由一個直流-交流轉換級組成。一些逆變器還具有 DC-DC 升壓級,以擴展 MPP(最大功率點)電壓範圍。低頻變壓器有時用於升壓交流電壓並在輸出端提供隔離。然而,這會降低效率並增加逆變器的尺寸、重量和成本。

中央逆變器的最大輸入電壓通常為 1,000V。然而,一些新的中央逆變器已經配備了 1,500 V 的輸入電壓。這些逆變器支援電壓高達 1,500V 的光伏陣列,並且需要更少的 BOS(系統平衡)組件。

中央逆變器可以是單片式的(使用單一動力傳動系統和多 MPPT 追蹤器),也可以是模組化的(使用多個動力傳動系統)。模組化逆變器更為複雜,但即使一個或多個模組發生故障,也可以維持較低的功率輸出,並且可以使用多 MPPT 或主/從控制方法。多 MPPT 系統對每個浮動子陣列使用單獨的轉換器和 MPPT,以改善部分遮蔽條件下的整體能源採集。在主/從方式中,控制器模組始終開啟。當陣列提供更多電力時,命令從屬模組開啟,從而在低太陽輻射環境下最大限度地提高逆變器效率。

中央逆變器用於公用事業規模的應用,因此它們必須產生與所使用的電網相同的電壓和頻率。世界各地有大量不同的電網標準,製造商可以客製化這些參數,以滿足他們對相數的特定要求。大多數製造的集中式逆變器都是三相逆變器。

2022年1月,陽光電源在阿布達比世界未來能源高峰會上發表了新型1+X中央模組化逆變器,輸出容量為1.1MW。這款1+X模組化逆變器可組合成8個單元,達到8.8MW功率,並具有用於連接能源儲存系統(ESS)的DC/ESS介面。

因此,電力需求的增加、政府對電力產業脫碳的努力以及中央逆變器成本的下降預計將在預測期內推動該產業的成長。

亞太地區主導市場

2021 年,亞太地區在太陽能逆變器市場佔據主導地位,預計在未來幾年將保持其主導地位。預計大部分需求將來自中國,中國也是世界上最大的太陽能生產國。

在中國,人們對提供零電壓穿越 (ZVRT) 方案的太陽能逆變器越來越感興趣。為了滿足系統的標準,太陽能發電廠必須持續運作而不會故障。這一點更為重要,因為該國生產的太陽能比世界上任何其他國家都多。

隨著工業化在世界各地引起人們對污染的擔憂,特別是在亞洲和太平洋地區,區域太陽能發電獲得了相當大的發展勢頭。作為《巴黎協定》承諾的一部分,印度政府制定了在 2022 年實現 175 吉瓦可再生能源裝置容量的雄心勃勃的目標。在175GW中,100GW分配給太陽能光伏產能,其中40GW(40%)分配給太陽能光伏產能。預計將透過分佈式和屋頂規模的太陽能發電工程來實現。為了實現這一雄心勃勃的目標,政府在 2019 年啟動了多項新計劃,包括開發屋頂太陽能發電二期、PM-KUSUM 和超大型可再生能源發電園區 (UMREPP)。

印度的太陽能發電潛力超過 750 吉瓦,該國的 2047 年能源安全情境顯示,到 2047 年,太陽能裝置容量可望達到約 479 吉瓦。印度太陽能發電由於太陽輻射強度高,已經實現市電平價,將太陽能光伏發電作為主流能源來源,加大公用事業規模和屋頂光伏發電的裝機容量,我們正在大力推廣。

截至2021年11月,陽光電源自2014年以來在印度的太陽能逆變器出貨已超過10GW。這是由於印度各地對太陽能的需求不斷增加。 2022年3月,陽光電源將印度工廠產能提高至每年10GW。製造業的如此巨大發展預計將推動預測期內調查市場的成長。

因此,由於中國、印度、馬來西亞等政府發起的各種舉措,亞太地區預計將在預測期內主導太陽能逆變器市場。

太陽能逆變器產業概況

太陽能逆變器市場本質上是分散的。市場主要企業包括(排名不分先後)FIMER SpA、施耐德電氣、西門子股份公司、三菱電機公司和Omron Corporation。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查範圍

- 市場定義

- 調查先決條件

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2027 年之前的市場規模與需求預測

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 按逆變器類型

- 中央逆變器

- 組串式逆變器

- 微型逆變器

- 按用途

- 住宅

- 商業和工業

- 公共事業規模

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 南美洲

- 中東和非洲

第6章 競爭形勢

- 併購、合資、合作與協議

- 主要企業採取的策略

- 公司簡介

- FIMER SpA

- Schneider Electric SE

- Siemens AG

- Mitsubishi Electric Corporation

- Omron Corporation

- General Electric Company

- SMA Solar Technology AG

- Delta Energy Systems Inc.

- Enphase Energy Inc.

- SolarEdge Technologies Inc.

- Huawei Technologies Co. Ltd

第7章市場機會與未來趨勢

The Solar PV Inverters Market size is estimated at USD 13.68 billion in 2024, and is expected to reach USD 17.23 billion by 2029, growing at a CAGR of 4.73% during the forecast period (2024-2029).

Although the market studied was affected by COVID-19 in 2020, it has recovered and reached pre-pandemic levels.

The growing demand for solar power is expected to stimulate the growth of the solar PV inverters market during the forecast period. Increasing investments and ambitious solar energy targets are expected to drive the growth of the market studied. However, technical drawbacks of string inverters are expected to hamper the growth of the solar PV inverters market during the forecast period.

Product innovation and adaptation of the latest technologies in solar PV inverters are anticipated to create lucrative growth opportunities for the solar PV inverters market during the forecast period. Asia-Pacific dominates the market, and it is expected to record the highest CAGR during the forecast period. This growth is attributed to the increasing investments and supportive government policies in the countries of this region, including India, China, and Australia.

Solar PV Inverter Market Trends

Central Inverters Segment Expected to Dominate the Market

A central inverter is a large grid feeder. It is often used in solar photovoltaic systems with rated outputs over 100 kWp. Floor or ground-mounted inverters convert DC power collected from a solar array into AC power for grid connection. These devices range in capacity from around 50kW to 1MW and can be used indoors or outdoors.

A central inverter consists of one DC-AC conversion stage. Some inverters also have a DC-DC boost stage to increase their MPP (maximum power point) voltage range. Low-frequency transformers are sometimes used to boost the AC voltage and provide isolation at the output. However, this reduces efficiency and increases the inverter's size, weight, and cost.

A central inverter typically has a maximum input voltage of 1,000V. However, some newer central inverters already come with 1,500V input voltage. These inverters allow PV arrays based on a maximum voltage of 1,500V, requiring fewer BOS (balance of system) components.

Central inverters can be monolithic (using a single power train and multi-MPPT tracker) or modular (using multiple power trains). Modular inverters are more complex but can maintain reduced power output if one or more modules fail and can use either a multi-MPPT or a master-slave control approach. The multi-MPPT system uses a separate converter and MPPT for each floating sub-array, increasing the overall energy harvest under partial shading conditions. In the master-slave approach, the controller module is always on. It commands the slave modules to switch on when more power is available from the array, which maximizes inverter efficiency in low-insolation environments.

As central inverters are used for utility-scale applications, they should produce the same voltage and frequency as that of the electric grid where they are used. As there are a lot of different electric grid standards worldwide, manufacturers are allowed to customize these parameters to match the specific requirements in terms of the number of phases; most central inverters manufactured are three-phase inverters.

In January 2022, Sungrow launched its new 1+X central modular inverter with an output capacity of 1.1MW at the World Future Energy Summit in Abu Dhabi. This 1+X modular inverter can be combined into eight units to reach a power of 8.8MW and features a DC/ESS interface for the connection of energy storage systems (ESS).

Therefore, the growing demand for electricity, the government's efforts to decarbonize the power sector, and the declining costs of central inverters are expected to drive the segment's growth during the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific dominated the solar PV inverter market in 2021, and it is expected to continue its dominance over the coming years. Most of the demand is expected to come from China, which is also the largest producer of solar energy in the world.

There has been an increased emphasis on solar inverters in China, providing a zero-voltage ride through (ZVRT) scheme. To meet the scheme norms, the solar PV power plants must continue to operate without breaking. This is even more significant as the country hosts the largest amount of solar power generation in the world.

With the rising concerns over pollution across the world due to industrialization, especially in Asia-Pacific, regional solar power generation gained considerable momentum. As part of the Paris Agreement commitments, the Government of India set an ambitious target of achieving 175 GW of renewable energy capacity by 2022. Out of the 175 GW, 100 GW was earmarked for solar capacity with 40 GW (40%), which was expected to be achieved through decentralized and rooftop-scale solar projects. To achieve this huge target, the government launched several new programs in 2019, like the solar rooftop phase-2, PM-KUSUM, and the development of ultra mega renewable energy power parks (UMREPPs).

India's solar potential is more than 750 GW, and the country's energy security scenario 2047 shows a possibility of achieving around 479 GW of solar PV installed capacity by 2047. Solar power in India, bestowed with high solar irradiance, has already achieved grid parity that encourages the adoption of solar power as a mainstream energy source, pushing forward the capacity installations in the utility-scale and rooftop solar segments.

As of November 2021, Sungrow Power Supply Co. Ltd has shipped more than 10 GW of solar inverters in India since 2014. This is due to the increased demand for solar energy across the country. In March 2022, Sungrow increased its fab capacity in India to 10GW/annum capacity. Such a large development in the manufacturing sector is expected to boost the growth of the market studied during the forecast period.

Therefore, with various government initiatives launched by China, India, Malaysia, etc., Asia-Pacific is expected to dominate the solar PV inverter market during the forecast period.

Solar PV Inverter Industry Overview

The solar PV inverters market is fragmented in nature. Some of the major players in the market (in no particular order) include FIMER SpA, Schneider Electric SE, Siemens AG, Mitsubishi Electric Corporation, and Omron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Inverter Type

- 5.1.1 Central Inverters

- 5.1.2 String Inverters

- 5.1.3 Micro Inverters

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial

- 5.2.3 Utility-scale

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FIMER SpA

- 6.3.2 Schneider Electric SE

- 6.3.3 Siemens AG

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 Omron Corporation

- 6.3.6 General Electric Company

- 6.3.7 SMA Solar Technology AG

- 6.3.8 Delta Energy Systems Inc.

- 6.3.9 Enphase Energy Inc.

- 6.3.10 SolarEdge Technologies Inc.

- 6.3.11 Huawei Technologies Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年按技術、電壓、應用和地區分類的太陽能光電逆變器市場報告

2024-2032 年按技術、電壓、應用和地區分類的太陽能光電逆變器市場報告 公用事業規模太陽能逆變器市場報告:2030 年趨勢、預測與競爭分析

公用事業規模太陽能逆變器市場報告:2030 年趨勢、預測與競爭分析 光電逆變器市場:依產品、最終用途分類 - 2024-2030 年全球預測

光電逆變器市場:依產品、最終用途分類 - 2024-2030 年全球預測 全球光伏逆變器市場規模、佔有率和行業趨勢分析報告:2023-2030年按產品、最終用途和地區分類的展望和預測

全球光伏逆變器市場規模、佔有率和行業趨勢分析報告:2023-2030年按產品、最終用途和地區分類的展望和預測 光電逆變器市場規模、佔有率、趨勢分析報告:按產品、按最終用途、按地區、細分市場預測,2024-2030 年

光電逆變器市場規模、佔有率、趨勢分析報告:按產品、按最終用途、按地區、細分市場預測,2024-2030 年 住宅太陽能光電逆變器市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測(按類型、階段、連接類型、地區、競爭細分)

住宅太陽能光電逆變器市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測(按類型、階段、連接類型、地區、競爭細分) 住宅太陽能微型逆變器市場 - 2018-2028 年按類型、連接性、組件、地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測。

住宅太陽能微型逆變器市場 - 2018-2028 年按類型、連接性、組件、地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測。 商業太陽能光電逆變器市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測(按類型、階段、連接類型、地區、競爭細分)

商業太陽能光電逆變器市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測(按類型、階段、連接類型、地區、競爭細分) 商用太陽能微型逆變器市場 - 2018-2028 年按類型、連接性、組件、地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測。

商用太陽能微型逆變器市場 - 2018-2028 年按類型、連接性、組件、地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測。 亞太地區光電逆變器市場規模 - 依產品(串式、微型、中央)、相(單相、三相)、連接方式(獨立式、併網)、標稱輸出功率、標稱輸出電壓、按應用與全球預測,2023 - 2032

亞太地區光電逆變器市場規模 - 依產品(串式、微型、中央)、相(單相、三相)、連接方式(獨立式、併網)、標稱輸出功率、標稱輸出電壓、按應用與全球預測,2023 - 2032