|

市場調查報告書

商品編碼

1404080

非接觸式付款終端:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Contactless Payment Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

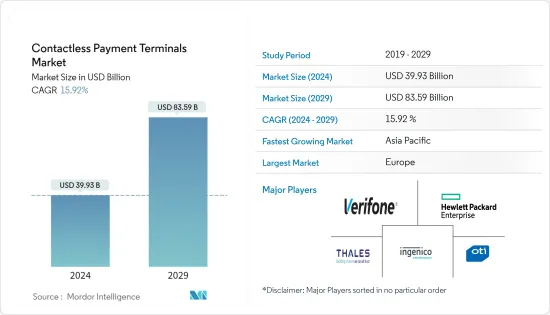

非接觸式付款終端市場規模預計到 2024 年為 399.3 億美元,預計到 2029 年將達到 835.9 億美元,在預測期內(2024-2029 年)複合年成長率為 15.92%。

由於企業和消費者數位轉型的趨勢不斷增強以及智慧型手機的普及,全球付款和交易格局正在迅速變化。智慧型手機、數位付款卡和零售 POS 終端的技術進步正在推動市場成長。

主要亮點

- 越來越多的國家正在尋求向無現金經濟轉型,透過激勵消費者進行數位付款來推動數位付款提供者的獎勵。此外,全球非接觸感應卡交易的擴展正在推動各個最終用戶產業對非接觸式付款終端的需求。

- 非接觸式付款因其便利性和偏好而廣受歡迎。因此,各種穿戴式裝置製造商正在將近場通訊(NFC)技術整合到他們的大多數裝置中,透過消除擺弄錢包、錢包和行動電話的需要來增加便利性。

- 此外,全球消費者對基於智慧型手機的付款方式的趨勢正在以銷售點系統上的非接觸式付款方式的形式增加,因此卡片和金融服務提供者·我們提供解決方案或透過第三方供應商提供解決方案。

- 此外,近年來全球金融詐騙的增加促使政府監管機構推動提高付款交易的安全性。客戶要求安全可靠的數位交易,增加了使用安全付款流程的需求。因此,這些監管機構對 POS 終端的採用有正面影響。隨著全球行動趨勢的興起,行動 POS 系統越來越受歡迎。隨著無現金交易技術的出現,POS 的採用率預計將會提高。

- 此外,技術進步正在塑造非接觸式付款終端市場的未來。市場開拓供應商專注於開發敏捷、高效的付款管道,同時也努力提高非接觸式付款的普及和普及。例如,去年 2 月,數位付款公司 Infibeam Avenues Limited (IAL) 宣布將推出無硬體非接觸式行動 POS(資訊點系統),擴大其付款解決方案組合。

- 在 COVID-19大流行期間,世界各地的消費者開始尋找避免人際接觸的方法,以保護自己免受感染。為此,非接觸式付款的需求不斷增加,許多產業對非接觸式POS終端機等各種非接觸式付款終端的需求不斷增加。此外,即使在大流行之後,由於新興國家數位付款的普及,對非接觸式付款終端的需求預計將迅速增加。

非接觸式付款終端的市場趨勢

零售業預計將佔據主要市場佔有率

- 非接觸式付款終端在零售業的使用越來越多,引入非接觸式付款終端可以帶來好處,例如促銷和提高客戶滿意度,因此市場佔有率,預計會很高。透過提供非接觸式付款選項,零售商正在提高結帳流程的速度和效率,並透過更順暢、更快的交易來培養客戶忠誠度。

- 此細分市場的主要驅動力是經銷店以及在零售店結帳時使用行動錢包的偏好。基於行動的 POS (mPOS) 的發展包括連接到平板電腦或智慧型手機上的基本 ePOS 應用程式的讀卡器,雖然商家入門很簡單,但該服務是「計量收費模式」提供的。在零售業,這些案例很可能導致非接觸式付款終端的引入。

- 市場參與者正在為零售商提供創新和智慧的解決方案,預計這將推動非接觸式付款終端在零售領域的採用。例如,去年,金融服務平台 Square 宣布向美國數百萬商家推出適用於 iPhone 的 Tap to Pay 服務。此外,新推出的 iPhone 上的 Tap to Pay 功能讓您可以直接從 iPhone 接受非接觸式付款,無需任何硬體或額外費用。

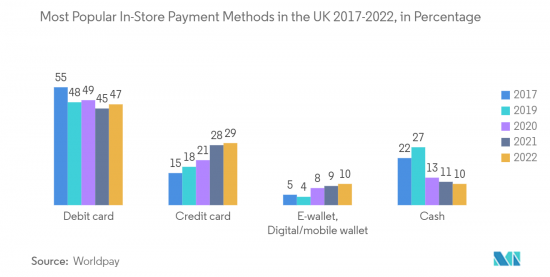

- 此外,零售店和商店的非接觸式簽帳金融卡和信用卡付款的增加預計將在預測期內推動零售業對非接觸式終端的市場需求。例如,Worldplay統計數據顯示,簽帳金融卡是去年英國最常使用的付款方式,分別佔POS終端所有付款的45%和28%。

預計歐洲將佔據非接觸式付款終端市場的較大佔有率

- 由於消費者習慣變化、監管環境不斷變化、技術創新和市場形勢等大流行原因,付款格局正在發生變化,預計歐洲地區將在未來一段時間內佔據重要的市場佔有率。此外,非接觸式付款終端在各個最終用戶行業的廣泛採用是一個主要的成長要素,並可能在未來幾年進一步推動市場發展。

- 在歐洲,隨著消費者將這種相對較新的付款方式融入他們的日常生活,穿戴式付款設備繼續普及。例如,戒指、穿戴式裝置、手環和智慧型手錶都具有近場通訊(NFC)功能。穿戴式裝置有兩種類型:「主動」和「被動」。如果您穿著像戒指一樣的被動手錶,則可以透過在付款終端輸入 PIN 碼來核准交易,就像塑膠卡一樣。如果您穿戴的是活動手錶(例如智慧型手錶),PIN 碼會插入裝置本身,讓您只需輕輕一按即可付款。

- 此外,在新冠肺炎 (COVID-19) 疫情期間,非接觸式付款在歐洲推廣,非接觸式卡片限額也大幅增加。大流行後,該地區越來越多的消費者轉向非接觸式付款,預計將進一步推動市場。例如,根據歐洲央行(ECB)的報告,POS上的非接觸式卡片付款在三年內大幅成長,從2019年佔所有卡片付款的41%上升到去年的62%。

- 此外,該地區市場供應商的持續產品創新預計將在預測期內推動市場發展。例如,PayPal Holdings Inc. 去年 5 月為英國的小型企業推出了 Tap to Pay with Zettle by PayPal。這項新功能使個人賣家和小型企業能夠直接在其 Android 行動裝置上接受非接觸式面對面付款,無需任何額外的硬體或費用。

非接觸式付款終端產業概況

非接觸式付款終端市場已整合,因為只有一些參與者擁有重要的市場佔有率。此外,消費者對非接觸感應卡的認知以及對安全問題的擔憂使得新參與企業難以進入該市場。市場的主要企業包括 Thales Group、OTI、VeriFone Systems Inc.、Hewlett Packard 和 Ingenico Group SA。

- 2022 年 9 月 - 萬事達卡、泰雷茲集團、ProvidusBank 和 Interswitch 宣佈在奈及利亞推出新的觸碰支付服務。觸碰支付服務讓持卡人透過非接觸式付款終端輕觸支援 NFC 的智慧型設備,即可快速、安全且方便地進行商店付款。

- 2022 年 3 月 - Softpay.io 是一款使用非接觸式卡和行動錢包以及全新創新 SoftPOS 解決方案 Softpay 的行動付款應用程式,允許商家在 Android 手機或平板電腦上使用相同的付款終端,而無需額外的硬體Nets(Nexi 集團成員) ,已推出非接觸式付款。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 減少等待時間並加快結帳速度

- 非接觸式付款帶來的便利與輕鬆

- 市場抑制因素

- 數位付款的安全問題

第6章市場區隔

- 依技術

- Bluetooth

- 紅外線的

- 職業基礎

- Wi-Fi

- 其他技術

- 按付款方式

- 基於帳戶

- 信用卡/簽帳金融卡

- 儲值

- 智慧卡

- 其他付款方式

- 按設備

- 綜合銷售點

- mPOS

- PDA

- 無人值守終端

- 非接觸式讀卡機

- 其他設備

- 按最終用戶產業

- 零售

- 運輸

- 銀行

- 政府機關

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 北美洲

第7章競爭形勢

- 公司簡介

- Thales Group

- On Track Innovation LTD.(OTI)

- VeriFone Inc.

- Hewlett Packard Enterprise Development LP

- Ingenico Group SA

- Visiontek Products LLC

- PayPal Holdings Inc.

- Castles Technologies

- ID Tech Solutions

- NEC Corporation

第8章投資分析

第9章市場的未來

The Contactless Payment Terminals Market size is estimated at USD 39.93 billion in 2024, and is expected to reach USD 83.59 billion by 2029, growing at a CAGR of 15.92% during the forecast period (2024-2029).

The global landscape of payments and transactions is changing rapidly, owing to the growing enterprises and consumer propensity toward digital transformation and the proliferation of smartphones. Technological advancements in smartphones, digital payment cards, and retail POS terminals fuel market growth.

Key Highlights

- More and more countries are moving toward becoming cashless economies, thus encouraging digital payment providers by incentivizing their consumers' digital forms of payments. In addition, growing contactless card transactions worldwide drive the demand for contactless payment terminals in various end-user industries.

- Contactless payments are gaining significant traction due to their convenience and preference. As a result, various wearable device manufacturers are incorporating near-field communication (NFC) technology as a standard into most devices to provide greater convenience by removing the need to fumble with a wallet, purse, or phone.

- In addition, the global consumer inclination toward payment methods involving smartphones is increasing in the form of contactless payment methods at POS systems, owing to which card and financial service providers are either offering their card solutions on smartphones or via third-party vendors.

- Additionally, the rising financial frauds worldwide have influenced government regulatory bodies to secure payment transactions over the past few years. With customers demanding safe and reliable digital transactions, the need for using secure payment processes has increased. Therefore, these regulatory bodies have positively impacted the adoption of POS terminals. With the increasing mobility trends worldwide, mobile POS systems are gaining traction. With the advent of cashless transactional technologies, POS is expected to witness an increase in adoption rates.

- Moreover, technological advancements are shaping the future of the contactless payment terminals market. Market vendors are focusing on developing payment platforms that are agile and efficient and also increase the penetration and reach of contactless payments. For instance, in February last year, digital payments player Infibeam Avenues Limited (IAL) announced to broaden its payment solutions portfolio by launching a no-hardware contactless mobile point of sale (POS), which will facilitate card payment transactions for small vendors through a tap-on-phone technology.

- During the COVID-19 pandemic, consumers worldwide started finding ways to avoid human contact in order to protect themselves from getting affected. Due to this, the demand for contactless payments has increased, boosting the demand for various contactless payment terminals, such as contactless POS terminals, in multiple industries. In addition, even after the pandemic, the demand for contactless payment terminals is expected to grow rapidly, owing to the proliferation of digital payments in emerging economies.

Contactless Payment Terminals Market Trends

Retail Industry is Expected to Hold Major Market Share

- With the increased use of contactless payment terminals in retail, together with benefits arising from placing them on offer like promotion of sales at merchants and improved customer satisfaction, it is expected to have a strong market share. Retailers provide a contactless payment option to enhance the speed and efficiency of the checkout process, fostering customer loyalty through smoother and quicker transactions.

- Point-of-sale terminals (POS) across retail stores and The primary drivers for this segment are outlets and a preference of mobile wallets to check out from retail stores. The evolution of mobile-based POS (mPOS) includes an card reader connected to a basic ePOS app on a tablet or smartphone, and while Merchant onboarding is simple, where the service is delivered on a 'pay-as-you-go model. In the retail sector, these cases are likely to lead to deployment of Contactless Payment Terminals.

- Market players offer innovative and smart solutions for retailers, expected to drive the adoption of contactless payment terminals in the retail segment. For instance, the previous year, Square, a financial services platform, It's announced to its millions of sellers in the United States that it will be launching a Tap To Pay service for iPhone. In addition, the newly launched Tap to Pay on iPhone enables all sizes of vendors Accepting contactless payments directly from their iPhones without any hardware or additional costs is also available as an application in Square Point Of Sale'siOS point of sale applications.

- Moreover, the growth in contactless debit card and credit card transactions in retail stores and outlets is anticipated to drive the market demand for contactless terminals in the retail sector over the forecast period. For example, the most popular payment method in the UK last year was debit cards which accounted for 45 % and 28 % respectively of all payments made at POS terminals according to statistics from Worldplay.

Europe is Expected to Hold Significant Share in the Contactless Payment Terminals Market

- The European region is expected to hold a significant market share over the upcoming period, owing to the changing payment landscape for various reasons: changing consumer habits, regulatory developments, innovation, and the COVID-19 pandemic. Moreover, the broader adoption of contactless payment terminals in different end-user industries is witnessing significant growth, further driving the market in the coming years.

- In Europe, consumers' wearable devices for payments continue to take off as they grate this relatively new payment method into their daily lives. For example, a ring, a wearable device, a bracelet, or a smartwatch, has Near-field Communication (NFC) capabilities. There exists 'active' and 'passive' wearables. The transaction which can be authorized by entering the PIN code on the payment terminal, just as with a plastic card, if you have your passive wristwatch that is like a ring. When you wear an active watch, such as a smartwatch, the PIN is inserted on your device itself and payments can be made using one tap.

- Additionally, amidst the COVID-19 situation, contactless card limits across Europe grew substantially as contactless payments were promoted across the continent. More and more consumers in the region are moving toward contactless payments after the pandemic, which is further expected to drive the market. For instance, according to European Central Bank (ECB) report, contactless card payments at the POS increased considerably in three years, from 41% of all card payments in 2019 to 62% in the last year.

- In addition, continuous product innovation by market vendors in the region is expected to drive the market over the forecast period. For instance, in May last year, PayPal Holdings Inc. launched Tap to Pay with Zettle by PayPal for small businesses in the United Kingdom. The new function will enable individual sellers and small businesses to accept contactless in-person payments directly on Android mobile devices without additional hardware and fees.

Contactless Payment Terminals Industry Overview

The contactless payment terminals market is consolidated because only some players have a significant market share. Moreover, consumers' need for more awareness toward contactless cards and concern over security issues make market entry challenging for new players. Some of the key players in the market include Thales Group, OTI, VeriFone Systems Inc., Hewlett Packard, and Ingenico Group SA.

- September 2022 - Mastercard, Thales Group, ProvidusBank, and Interswitch announced a new Tap-to-Pay service in Nigeria. The Tap-to-Pay service allows cardholders to make fast, secure, and convenient in-store payments by tapping their NFC-enabled smart device at any contactless-enabled payment terminal.

- March 2022 -With Softpay.io, a mobile payment with contactless cards and mobile wallets application, and A new and innovative softPOS solution, Softpay, which enables merchants to accept contactless payments on Android phones and tablets in the same way as payment terminals without additional hardware, has been launched by Nets, part of Nexi Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 impact on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Reduction in Queuing Time and Quicker Checkout Time

- 5.1.2 Convenience and Ease Associated with Contactless Payments

- 5.2 Market Restraints

- 5.2.1 Security Concerns Regarding Digital Payment

6 MARKET SEGMENTATION

- 6.1 Technology

- 6.1.1 Bluetooth

- 6.1.2 Infrared

- 6.1.3 Carrier-based

- 6.1.4 Wi-Fi

- 6.1.5 Other Technologies

- 6.2 Payment Mode

- 6.2.1 Account-based

- 6.2.2 Credit/Debit Card

- 6.2.3 Stored Value

- 6.2.4 Smart Card

- 6.2.5 Other Payment Modes

- 6.3 Device

- 6.3.1 Integrated POS

- 6.3.2 mPOS

- 6.3.3 PDA

- 6.3.4 Unattended Terminal

- 6.3.5 Contactless Reader

- 6.3.6 Other Devices

- 6.4 End-user Industry

- 6.4.1 Retail

- 6.4.2 Transportation

- 6.4.3 Banking

- 6.4.4 Government

- 6.4.5 Healthcare

- 6.4.6 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Rest of Asia- Pacific

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Argentina

- 6.5.4.3 Mexico

- 6.5.4.4 Rest of Latin America

- 6.5.5 Middle-East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 Saudi Arabia

- 6.5.5.3 South Africa

- 6.5.5.4 Rest of Middle-East and Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thales Group

- 7.1.2 On Track Innovation LTD. (OTI)

- 7.1.3 VeriFone Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Ingenico Group SA

- 7.1.6 Visiontek Products LLC

- 7.1.7 PayPal Holdings Inc.

- 7.1.8 Castles Technologies

- 7.1.9 ID Tech Solutions

- 7.1.10 NEC Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

虛擬付款(POS)終端全球市場報告 2024年

虛擬付款(POS)終端全球市場報告 2024年 2030 年商業付款終端市場預測:按類型、最終用戶和地區分類的全球分析

2030 年商業付款終端市場預測:按類型、最終用戶和地區分類的全球分析 非接觸式付款終端市場報告:2030 年趨勢、預測與競爭分析

非接觸式付款終端市場報告:2030 年趨勢、預測與競爭分析 全球戶外支付終端市場研究報告 - 2023年至2030年行業分析、規模、佔有率、成長、趨勢和預測

全球戶外支付終端市場研究報告 - 2023年至2030年行業分析、規模、佔有率、成長、趨勢和預測 全球支付工具市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測

全球支付工具市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測 按類型和應用分類的戶外付款終端 (OPT) 市場:2023-2032年全球機會分析和產業預測

按類型和應用分類的戶外付款終端 (OPT) 市場:2023-2032年全球機會分析和產業預測 戶外付款終端市場:按類型、部署型態、最終用戶、用途- 全球預測 2023-2030

戶外付款終端市場:按類型、部署型態、最終用戶、用途- 全球預測 2023-2030 支付終端市場:按類型、組件、EMV 相容、最終用戶分類 - 2023-2030 年全球預測

支付終端市場:按類型、組件、EMV 相容、最終用戶分類 - 2023-2030 年全球預測 支付設備市場:按支付設備類型(信用卡、金融卡、直接簽帳金融卡)、類型(桌面、手持式、行動)、最終用戶 - 2023-2030 年全球預測

支付設備市場:按支付設備類型(信用卡、金融卡、直接簽帳金融卡)、類型(桌面、手持式、行動)、最終用戶 - 2023-2030 年全球預測 室外用付款終端(OPT)的全球市場:市場規模 - 各產品類型,各終端用戶,各用途,各部署模式,各地區展望,競爭策略,各市場區隔預測(~2032年)

室外用付款終端(OPT)的全球市場:市場規模 - 各產品類型,各終端用戶,各用途,各部署模式,各地區展望,競爭策略,各市場區隔預測(~2032年)