|

市場調查報告書

商品編碼

1432853

資料中心結構:市場佔有率分析、產業趨勢、成長預測(2024-2029)Data Center Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

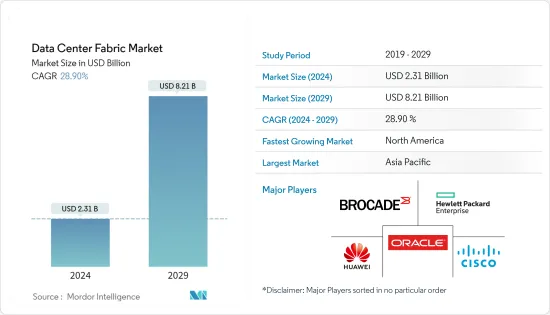

資料中心結構市場規模預計2024年為23.1億美元,預計到2029年將達到82.1億美元,在預測期內(2024-2029年)成長28.90%,以複合年成長率成長。

複雜互動式應用程式使用量的增加、網際網路服務和活動的擴展以及技術的不斷進步,需要更快的資料速率、更多的計算資源和存儲來管理生成的資料量,這凸顯了對增加容量的需求。此外,自動化智慧資料中心網路必須適應分散式應用的動態處理要求。資料中心結構的概念由網格計算預示並由交換結構提出。

主要亮點

- 雖然最新、效能最高的資料中心硬體和軟體對於高速、關鍵事務處理仍然至關重要,但安全性、軟體定義網路 (SDN)、混合雲端和巨量資料等趨勢正在推動更高水準的資料中心提供基礎設施。金融服務。為您的客戶提供服務,同時降低風險並節省成本。

- 利用資料中心結構將實體資源虛擬化為邏輯池,讓應用程式可以從這些池中取得所需的資源,從而最佳化 IT 資源利用率。

- 由於基礎設施的擴張,特別是在中國和印度等新興國家,高速資料傳輸技術的使用增加以及複雜互動應用的研發專業知識的增加,市場價值預計將面臨挑戰。儘管如此,組織資料量和半導體產業的不斷擴大,特別是在新興國家,將為市場的進一步成長鋪平道路。

- 由於人工智慧、機器學習和 AR/VR 等新技術的使用,雲端基礎的應用程式正在經歷顯著成長。當今龐大且不斷成長的雲端建構者社群需要網路元件具有獨特程度的客製化和彈性來操作和監控龐大的資料中心。

- COVID-19感染疾病對人們的生活、人口、生存手段和經濟產生了意想不到的、不確定的影響。全球經濟衰退和失業的可能性增加。隨著公司在市場波動的情況下採取最佳化利潤的策略,預測不確定性的程度就變得有必要。封鎖措施的經濟影響對資料中心光纖產業產生了重大影響,供應鏈頻繁中斷阻礙了其發展。

資料中心布料市場趨勢

對光纖交換器的需求不斷成長推動了市場

- 光纖交換器透過整合資料中心在降低基礎設施成本方面發揮關鍵作用。乙太網路切換器和光纖通道是共用通用基礎設施的資料中心中整合伺服器和儲存網路的基礎。

- Fabric 基礎架構具有高度擴充性,可讓資料中心隨著組織未來需求的增加而成長。與傳統網路相比,扁平化網路的網路營運成本顯著降低,使得結構產品對於希望降低資料中心整體營運成本同時增加容量的組織來說成為有吸引力的選擇。

- 不斷上升的電力成本、雲端服務的採用以及對巨量資料儲存的需求正在促使組織在其資料中心部署結構產品。這樣做可以顯著降低電力和冷卻設備的管理費用。隨著公司擴大尋求透過向客戶提供即時應用程式解決方案來提高效能,扁平網路架構對於分析伺服器上儲存的資訊變得非常重要。

- 此外,雲端和內容服務供應商的網路支出預計將從核心資料中心到邊緣資料資料增加。從本地部署到主機代管設施的轉變將減少開發中國家在 1/10GbE 交換器上的支出,從而導致現代資料中心系統中 25/100GbE 交換器的顯著增加。

預計北美將佔據重要市場佔有率

- 由於行動寬頻、巨量資料分析和雲端運算的成長,資料中心基礎設施解決方案在北美經歷了令人矚目的成長。這種成長正在推動該地區對新資料中心基礎設施的需求。

- 北美正在大力投資研發,從而創造出技術更先進、資訊管理更有效的下一代設施。此外,該地區是許多資料中心基礎設施提供者的所在地,這極大地有助於其快速成長和市場佔有率。

- 然而,資料中心基礎設施的增加正在增加對資料中心結構市場的需求。由於擴大採用基於多核心處理器的伺服器、對有助於在單一伺服器上運行多個應用程式的虛擬伺服器的需求不斷增加以及對頻寬資料傳輸系統的需求,對高頻寬的需求也在不斷增加。網路布料市場。

- 美國目前擁有全球最多的資料中心,超大規模資料中心數量的不斷增加使得巨量資料量和流量顯著增加。

資料中心架構產業概況

資料中心結構市場是半整合的,由幾家中等集中度的大公司組成。這些公司正在相互競爭,以佔領不斷成長的市場,尤其超級資料中心市場。採取策略合作舉措,提高市場佔有率和盈利。市場上一些主要的參與者包括思科系統公司、甲骨文公司和惠普企業公司。

2023 年 8 月,Cyxtera 宣布與 (HPE) 建立合作夥伴關係,協助客戶簡化 IT 營運、提高敏捷性並大幅節省成本。 Cyxtera Enterprise Bare Metal 上的 HPE ProLiant 伺服器使客戶能夠受益於雲端的營運彈性,以及在 Cyxtera 全球資料中心運作的專用基礎設施的效能、控制和成本可預測性,並且具有安全性。

2022 年 7 月,Digital Realty 推出了 ServiceFabric,這是一個互連解決方案和編配平台,旨在支援更廣泛的全產業向以資料為中心的混合架構的過渡。此步驟是該公司計劃的一部分,旨在幫助客戶從其資料中釋放鎖定的價值。

2022 年 5 月,印度 NTT Ltd. 宣佈在新孟買開設一個新的超大規模資料中心設施,首先是 NAV1A資料中心。在此公告之前,Chandivali 設施開設了一個新的資料中心,這是印度第一個營運的超大規模資料中心園區。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 不斷成長的資料儲存需求和雲端運算採用

- 高速資料傳輸的需求

- 對光纖交換器的需求增加

- 市場限制因素

- 安全問題

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按解決方案

- 路由器

- 轉變

- 儲存區域網路

- 其他解決方案

- 按用途

- 資訊科技/通訊

- 銀行/金融服務

- 衛生保健

- 零售

- 其他

- 按最終用戶

- 雲端服務供應商

- 通訊服務供應商

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第6章 競爭形勢

- 公司簡介

- Cisco Systems Inc.

- Alcatel-Lucent Holdings Inc.

- Oracle Corporation

- Hewlett-Packard Enterprise Company

- Brocade Communications Systems

- Huawei Technologies Co. Ltd

- Extreme Networks Inc.

- Dell Inc.

- IBM Corporation

- Avaya Inc.

- Unisys Corporation

第7章 投資分析

第8章 市場機會及未來趨勢

The Data Center Fabric Market size is estimated at USD 2.31 billion in 2024, and is expected to reach USD 8.21 billion by 2029, growing at a CAGR of 28.90% during the forecast period (2024-2029).

The growing usage of complex interactive applications, the expansion of internet services and activities, and the constant advancement of technology have highlighted the need for faster data rates, more computing resources, and increased storage capacity to manage the volume of data being generated. Additionally, automated smart data center networks are required to adapt to the dynamic processing requirements of distributed applications. The data center fabric concept has been foreshadowed by grid computing and hinted at by switch fabric.

Key Highlights

- While the latest and highest-performing data center hardware and software are still essential for high-speed critical transaction processing, trends such as security, software-defined networks (SDN), hybrid cloud, and big data are crucial to delivering higher levels of financial services to clients while reducing risks and saving costs.

- The virtualization of physical resources into logical pools with the help of data center fabrics optimizes IT resource utilization by enabling applications to fetch required resources from these pools.

- The market value will face challenges due to the expansion of infrastructure, particularly in emerging economies like China and India, the growing use of high-speed data transmission technologies, and increased research and development expertise in relation to complex interactive applications. Nevertheless, the continued expansion of organizational data volumes and the semiconductor sector, especially in emerging nations, will pave the way for further market growth.

- Cloud-based applications are experiencing significant growth, driven by the use of new technologies such as AI, machine learning, and AR/VR. The current large and growing community of cloud builders requires a unique level of customization and flexibility from networking components to operate and monitor sprawling data centers.

- The COVID-19 pandemic had an unanticipated and undetermined impact on people's lives, groups, means of subsistence, and economies. The likelihood of a global economic downturn and employment losses increased. Given that businesses are now employing strategies to optimize profits despite market fluctuations, it has become necessary to forecast the degree of uncertainty. The financial ramifications of lockdown measures have significantly impacted the data center fabric industry, with frequent disruptions in the supply chain hindering its development.

Data Center Fabric Market Trends

Increasing Demand of Fabric Switches is Driving the Market

- Fabric switches play a critical role in reducing infrastructure costs by consolidating data centers. Ethernet switches and fiber channels serve as the foundation for bringing together server and storage networking in data centers that share a common infrastructure.

- The fabric infrastructure is highly scalable, allowing data centers to grow with the organization's increasing demands in the future. Compared to traditional networks, flattened networks' operational costs for networking decrease significantly, making fabric products an attractive option for organizations looking to reduce overall data center operation costs while increasing capacity.

- The rising cost of electricity, the adoption of cloud services, and the need for big data storage are motivating factors for organizations to install fabric products in their data centers. By doing so, they can reduce the overhead cost of power and cooling facilities by a considerable margin. As businesses increasingly seek to improve their performance by providing real-time application solutions to customers, flat network architecture becomes crucial for analyzing information stored in servers.

- Additionally, spending on networks by cloud and content service providers is expected to increase from core to edge data centers. On-premise migration to colocation facilities will decrease spending on 1/10GbE switches in developing nations and result in a significant increase in 25/100GbE switches in modern data center systems.

North America is Expected to Hold a Significant Market Share

- North America has experienced remarkable growth in data center infrastructure solutions due to the expansion of mobile broadband, the growth in big data analytics, and cloud computing. This growth is driving the demand for new data center infrastructures in the region.

- North America makes significant investments in research and development, which will result in the creation of next-generation facilities that are more technologically sophisticated and effective in terms of information management. Furthermore, the area is home to a number of data center infrastructure providers, which has greatly aided its quick growth and market share.

- However, the increase in data center infrastructures has led to high demand for the data center fabric market. The increased deployment of multi-core processor-based servers, the growing demand for virtualized servers that aid in running multiple applications on a single server, and the need for high-speed data transfer systems have led to an increased need for the high-bandwidth networking fabric market.

- The United States currently has the highest number of data centers globally and is witnessing robust growth in terms of the volume of big data and traffic due to the increase in the number of hyperscale data centers.

Data Center Fabric Industry Overview

The market for data center fabric is semi-consolidated and comprises several major players with moderate concentration. These companies are competing against each other to capture the growing market, particularly that of mega data centers. To increase their market share and profitability, they are employing strategic collaborative initiatives. Some of the significant players in the market are Cisco Systems Inc., Oracle Corporation, and Hewlett-Packard Enterprise Company, among others.

In August 2023, Cyxtera has announced its collaboration with (HPE) to help customers simplify their IT operations, improve agility, and realize significant cost savings, With HPE ProLiant servers on Cyxtera Enterprise Bare Metal, customers can benefit from the operational flexibility of the cloud with the performance, control, cost-predictability, and security of dedicated infrastructure running in Cyxtera's global data centers.

In July 2022, Digital Realty launched ServiceFabric, an interconnectivity solution and orchestration platform designed to support the industry's wider shift to a hybrid, data-centric architecture. This step is part of the company's plan to help customers unlock trapped value from their data.

In May 2022, NTT Ltd. in India announced the opening of its new hyperscale data center facility in Navi Mumbai, starting with the NAV1A data center. This announcement follows the opening of a new data center at its Chandivali facility, which is India's first operational hyperscale data center campus.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Data Storage and Adoption of Cloud Computing

- 4.2.2 Need for High Speed Data Transfer

- 4.2.3 Increasing Demand of Fabric Switches

- 4.3 Market Restraints

- 4.3.1 Security issues

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Solution

- 5.1.1 Router

- 5.1.2 Switches

- 5.1.3 Storage Area Networking

- 5.1.4 Other Solutions

- 5.2 By Application

- 5.2.1 IT & Communication

- 5.2.2 Banking & Financial Services

- 5.2.3 Healthcare

- 5.2.4 Retail

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Cloud Service Providers

- 5.3.2 Telecom Service Providers

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Alcatel-Lucent Holdings Inc.

- 6.1.3 Oracle Corporation

- 6.1.4 Hewlett-Packard Enterprise Company

- 6.1.5 Brocade Communications Systems

- 6.1.6 Huawei Technologies Co. Ltd

- 6.1.7 Extreme Networks Inc.

- 6.1.8 Dell Inc.

- 6.1.9 IBM Corporation

- 6.1.10 Avaya Inc.

- 6.1.11 Unisys Corporation