|

市場調查報告書

商品編碼

1432848

業務巨量資料分析:市場佔有率分析、產業趨勢與成長預測(2024-2029)Big Data Analytics In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

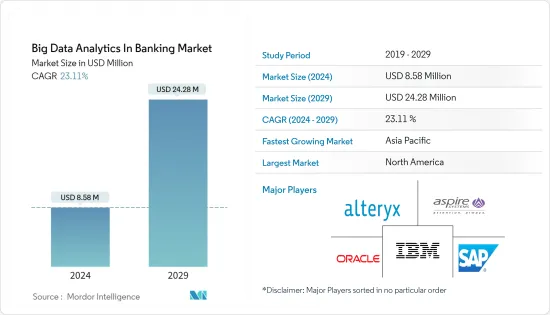

業務巨量資料分析市場規模預計到 2024 年為 858 萬美元,預計到 2029 年將達到 2,428 萬美元,在預測期內(2024-2029 年)複合年成長率為 23.11%。

巨量資料分析可幫助銀行根據多種見解的輸入來了解客戶行為,包括投資模式、購物趨勢、投資動機、個人或財務背景等。

主要亮點

- 產生的資料量的顯著增加和政府要求是銀行業採用巨量資料分析的主要驅動力。隨著科技的進步,消費者使用更多的設備(例如智慧型手機)來發起交易,這會影響交易量。鑑於目前的資料成長速度,需要更好的資料收集、組織、整合和分析。

- 政府法規和大量資料收集正在影響銀行業。隨著科技的發展,越來越多的消費者使用更多的設備(例如智慧型手機)來發起交易,增加了交易量。這推動了巨量資料分析,資料分析師可以在一處查看所有資料點並快速找到它們。借助這種統一的圖片,團隊成員可以交流可以加強銀行業的見解。

- 巨量資料分析解決方案提供發現新業務洞察所需的處理能力、持久性和分析能力,同時讓企業將所有資料儲存在靈活且經濟實惠的環境中。巨量資料分析工具提供了收集和追蹤結構化和非結構化資料以及組織資料各種來源的資料的技術。

- 大多數舊有系統無法處理不斷增加的負載。利用過時的基礎設施來收集、儲存和分析所需數量的資料可能會損害整個系統的穩定性。為了解決這個問題,組織必須提高處理能力或完全重新設計其系統。

- 由於銀行業擴大使用和採用資料分析來分析和探索消費者資料並實施有效的策略,COVID-19 的爆發對銀行業的數據分析產生了重大影響。由於科技的快速發展,銀行業的資料分析正在經歷顯著的成長。

業務巨量資料分析的市場趨勢

全行風險管理和內部控制推動成長

- 透過利用尖端技術,銀行可以降低信用風險並根據各種風險標準做出更好的決策。借助巨量資料和分析平台,銀行可以控制信用風險並避免違約情況。

- 另一個明顯的跡像是零售銀行正在利用巨量資料分析進行信用風險管理。事實證明,應用基於支付交易行為模式的信用風險指標可以比基於帳戶違約和逾期付款的傳統指標更早偵測信用事件。

- 使用資料和分析工具進行即時詐欺檢測,可以更密切地監控債務人並具有預測貸款損失的能力,有助於降低信貸和流動性風險。

- 正如美國銀行所證明的那樣,巨量資料可用於識別高風險帳戶。美國銀行的企業投資小組負責計算 950 萬筆房屋抵押貸款的違約機率,這使得美國銀行能夠預測違約損失。該銀行將計算壞帳所需的時間從 96 小時減少到 4 小時,從而提高了效率。

歐洲預計將出現顯著成長

- 管理金融機構如何交換和保護客戶個人資訊的最著名的法規是歐盟的《一般資料保護條例》。

- 此外,由於歐盟 (EU)付款服務指令 (PSD2),現在可以透過開放應用程式介面 (API) 進行資料交換。由於資料現在可以自由共用,因此收集、操作和分析資料的能力變得越來越重要。

- 此外,客戶數量和監管變化預計將很快增加。因此,對客戶分析和智慧技術的需求應該會增加。

- 英國勞埃德銀行業務集團採用資料分析來滿足不同客戶類別的需求,同時最佳化目標區隔市場的成長。

- 歐洲零售銀行正在利用巨量資料分析解決方案,以「開放銀行業務」趨勢解決傳統金融機構數十年來面臨的問題。

業務巨量資料分析概述

業務的巨量資料分析市場高度分散,因為有許多全球公司為銀行提供用於詐欺偵測和管理、客戶分析和社群媒體分析等不同應用的巨量資料分析解決方案。該市場的主要參與企業包括 Oracle 公司、IBM 公司和 SAP SE。

- 2023 年 2 月 - Alteryx 宣佈為 Alteryx Inc 的基於雲的分析工具添加新的自助服務和企業級功能,以助您做出更快、更明智的決策。 現在,該平臺已包括對 Designer Cloud 的完全訪問許可權,該平臺已得到改進,可為所有技能水平的員工提供友好、易於使用的拖放式介面,而不會影響數據治理或安全標準。

- 2022 年 8 月 - Aspire Systems 宣布採用整體方法來加速實施。這項創新由人工智慧提供支持,可提高實施速度。透過這種新的自主應用程式實施方法,Aspire Systems 可以幫助企業從 Oracle 雲端 ERP 應用程式實施中獲得最大價值。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 落實政府舉措

- 全行風險管理和內部控制推動成長

- 銀行產生的資料量增加

- 市場課題

- 缺乏資料隱私和安全

第 6 章相關案例和使用案例

第7章市場區隔

- 依解決方案類型

- 資料發現和視覺化 (DDV)

- 進階分析 (AA)

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第8章 競爭形勢

- 公司簡介

- IBM Corporation

- SAP SE

- Oracle Corporation

- Aspire Systems Inc.

- Adobe Systems Incorporated

- Alteryx Inc.

- Microstrategy Inc.

- Mayato GmbH

- Mastercard Inc.

- ThetaRay Ltd

第9章投資分析

第10章市場的未來

The Big Data Analytics In Banking Market size is estimated at USD 8.58 million in 2024, and is expected to reach USD 24.28 million by 2029, growing at a CAGR of 23.11% during the forecast period (2024-2029).

Based on the inputs obtained from numerous insights, such as investment patterns, shopping trends, investment motivation, and personal or financial background, big data analytics can help banks understand client behavior.

Key Highlights

- The considerable increase in the volume of data generated and governmental requirements are the main forces behind adopting Big Data analytics in the banking sector. With the development of technology, consumers are using more and more devices to start transactions (such as smartphones), which impacts the volume of transactions. Given the current data growth rate, better data collection, organization, integration, and analysis are necessary.

- Government rules and considerable data gathering are affecting the banking industry. As technology develops, more consumers are using more devices to start transactions (such as smartphones), which boosts the volume of transactions. This motivates big data analytics, which gives data analysts a single location to see and quickly locate all data points. Thanks to this consolidated picture, team members can exchange insights that could enhance the banking industry.

- A Big Data Analytics solution offers the processing, persistence, and analytic capabilities necessary to unearth fresh business insights while enabling a company to store all its data in a flexible, affordable environment. An analytics tool for big data gathers and keeps track of structured and unstructured data and techniques for arranging enormous amounts of wildly different data from various sources.

- The majority of legacy systems are unable to handle the rising burden. The entire system's stability may be compromised if the necessary amounts of data are gathered, stored, and analyzed utilizing an obsolete infrastructure. Organizations must either improve their processing capacity or entirely redesign their systems to tackle the issue.

- Due to the rise in usage and adoption in banking sectors to analyze and research consumer data and implement efficient strategies, the COVID-19 pandemic has significantly impacted data analytics in the banking industry. Because of the rapid evolution of technology, data analytics in banking has seen tremendous growth.

Big Data Analytics in Banking Market Trends

Risk Management and Internal Controls Across the Bank to Witness the Growth

- With the use of cutting-edge technologies, banks can reduce credit risk and make better decisions based on a variety of risk criteria. Banks can control credit risk and avert default circumstances thanks to the big data and analytics platform.

- Additionally, a blatant indicator is the retail bank's use of Big Data analytics for credit risk management. It has been demonstrated that applying credit risk indicators based on behavioral patterns in payment transactions allows for the detection of credit events much sooner than conventional indicators based on overdrawn accounts and late payments.

- Real-time fraud detection using data and analytics tools helps reduce credit and liquidity risk by enabling close monitoring of debtors and the ability to foresee loan default.

- Big data can be used to identify high-risk accounts, as demonstrated by The Bank of America. For 9.5 million mortgages, the Corporate Investment Group is responsible for calculating the likelihood of default, which helped Bank of America forecast losses from loan defaults. By cutting the time needed to calculate loan defaults from 96 to 4 hours, the bank was able to increase its efficiency.

Europe to Expected to Witness Significant Growth

- The most well-known rule governing how financial organizations exchange and safeguard customers' private information continues to be the General Data Protection Rule of the European Union.

- Moreover, data exchange was made possible through open application programming interfaces (APIs) as a result of the Payment Services Directive (PSD2) by the European Union. Due to an environment where data can be shared freely, the capacity to collect, handle, and analyze data has grown in importance.

- Additionally, it is anticipated that both the number of customers and regulatory revisions will rise shortly. The demand for customer analytics and intelligence technologies should consequently increase.

- The UK-based Lloyds Banking Group employed data analytics to meet the needs of diverse client categories while optimizing growth in targeted segments.

- European retail banks are using Big Data analytics solutions due to the "open banking" trend, which addresses problems that traditional financial institutions have faced for decades.

Big Data Analytics in Banking Industry Overview

Big Data Analytics In Banking Market is quite fragmented due to the existence of numerous global firms that provide a range of big data analytics solutions for banks for diverse applications, such as fraud detection and management, customer analytics, social media analytics, etc. Oracle Corporation, IBM Corporation, and SAP SE are some of the major market participants.

- February 2023 - Alteryx announced new self-service and enterprise-grade capabilities to its Alteryx Inc cloud-based analytics tool to support clients in making quicker and more informed decisions. With full access to Designer Cloud now included, the platform has been improved to provide employees of all skill levels with an approachable, simple-to-use drag-and-drop interface without compromising data governance or security standards.

- August 2022 - Aspire Systems launches the holistic approach to accelerate implementation. This innovation is powered by AI and drives implementation speeds. With this new autonomous application implementation methodology, Aspire Systems is geared to help businesses derive maximum value out of their Oracle Cloud ERP Application implementation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Enforcement of Government Initiatives

- 5.1.2 Risk Management and Internal Controls Across the Bank to Witness the Growth

- 5.1.3 Increasing Volume of Data Generated by Banks

- 5.2 Market Challenges

- 5.2.1 Lack of Data Privacy and Security

6 RELEVANT CASE STUDIES AND USE CASES

7 MARKET SEGMENTATION

- 7.1 By Solution Type

- 7.1.1 Data Discovery and Visualization (DDV)

- 7.1.2 Advanced Analytics (AA)

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia-Pacific

- 7.2.4 Latin America

- 7.2.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 IBM Corporation

- 8.1.2 SAP SE

- 8.1.3 Oracle Corporation

- 8.1.4 Aspire Systems Inc.

- 8.1.5 Adobe Systems Incorporated

- 8.1.6 Alteryx Inc.

- 8.1.7 Microstrategy Inc.

- 8.1.8 Mayato GmbH

- 8.1.9 Mastercard Inc.

- 8.1.10 ThetaRay Ltd

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

全球巨量資料分析市場規模、佔有率、成長分析、依類型、依分析工具、依部署模式、依組件、依應用程式(數據發現和視覺化、供應鏈管理)、依垂直行業 - 2024-2031 年行業預測

全球巨量資料分析市場規模、佔有率、成長分析、依類型、依分析工具、依部署模式、依組件、依應用程式(數據發現和視覺化、供應鏈管理)、依垂直行業 - 2024-2031 年行業預測 2024 年巨量資料與分析全球市場報告

2024 年巨量資料與分析全球市場報告 巨量資料分析市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模式、按應用、組織規模、產業、地區、競爭細分

巨量資料分析市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模式、按應用、組織規模、產業、地區、競爭細分 巨量資料和分析市場:按組件、分析工具、最終用途、部署模型、用途- 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測

巨量資料和分析市場:按組件、分析工具、最終用途、部署模型、用途- 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測 巨量資料分析的全球市場的評估:各零件,各企業規模,各終端用戶,各部署,各地區,機會,預測(2016年~2030年)

巨量資料分析的全球市場的評估:各零件,各企業規模,各終端用戶,各部署,各地區,機會,預測(2016年~2030年) 全球供應鏈大數據分析市場:市場規模、份額、趨勢分析、機會、預測——按解決方案、按服務、按最終用戶、按地區 (2019-2029)

全球供應鏈大數據分析市場:市場規模、份額、趨勢分析、機會、預測——按解決方案、按服務、按最終用戶、按地區 (2019-2029) 2022-2029 年教育領域大數據分析的全球市場規模研究與預測,按組件、部署模型、應用程序、部門、地區分析

2022-2029 年教育領域大數據分析的全球市場規模研究與預測,按組件、部署模型、應用程序、部門、地區分析 2022-2028 年能源行業大數據分析全球市場規模調查,按產品、應用、最終用戶、地區預測

2022-2028 年能源行業大數據分析全球市場規模調查,按產品、應用、最終用戶、地區預測 能源領域的巨量資料分析市場:各類服務,各應用領域,各終端用戶,各企業規模:全球機會分析與產業預測,2021年~2031年

能源領域的巨量資料分析市場:各類服務,各應用領域,各終端用戶,各企業規模:全球機會分析與產業預測,2021年~2031年 銀行業務的資料分析市場:各零件,各部署模式,各組織規模,各類型,各用途:全球機會分析及產業預測,2021年~2031年

銀行業務的資料分析市場:各零件,各部署模式,各組織規模,各類型,各用途:全球機會分析及產業預測,2021年~2031年