|

市場調查報告書

商品編碼

1432645

蒸餾包裝:市場佔有率分析、產業趨勢、成長預測(2024-2029)Retort Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

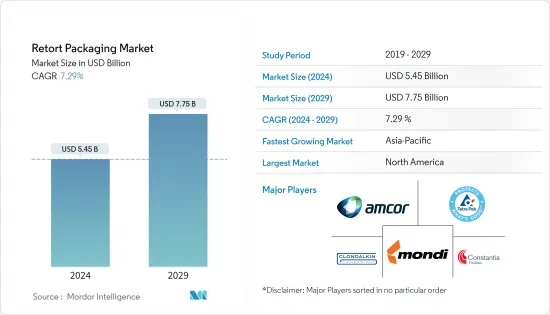

蒸餾包裝市場規模預計2024年為54.5億美元,預計到2029年將達到77.5億美元,在預測期內(2024-2029年)複合年成長率為7.29%成長。

主要亮點

- 由於多種原因,包括生活方式的改變、工作時間長和都市化加快,對即食食品的需求不斷增加。許多顧客正在尋找快速、簡單的用餐選擇,可以在幾分鐘內完成而不犧牲味道或品質。對於想要節省時間和精力的忙碌消費者來說,已烹調用餐提供了一個簡單明了的答案。隨著許多消費者選擇蒸餾包裝選項,蒸煮包裝已擴展到袋裝和托盤產品。據軟包裝協會稱,蒸餾拉繩和袋子約佔全球所有食品包裝的 60%。

- 美國人口普查局報告稱,2022 年 9 月至 2022 年 12 月期間,美國食品和飲料月度零售額有所成長。 2022年9月的售價為782.16億美元。 2022年12月,其價值達到驚人的884.32億美元。預計這一趨勢將在未來幾年持續下去。因此,由於市場零售需求逐漸增加,蒸餾包裝的需求預計在預測期內將會擴大。

- 消費者最初不願支付高價購買寵物的心理正在逐漸讓位於寵物人性化和敏感性增加等趨勢,收養率的迅速上升就證明了這一點。由於軟包裝技術在零售、製藥、食品和飲料以及寵物食品等各個領域的廣泛使用,殺菌袋在世界各地變得越來越受歡迎。

- 然而,蒸餾包裝產業的主要問題之一是蒸餾包裝材料的製造成本高。蒸餾包裝由塑膠、鋁和其他材料製成,使其耐用且能夠承受高溫。然而,這些材料的價格以及製造它們所需的專用機械和生產方法增加了製造價格。由於蒸餾包裝的成本較高,對於資源有限的中小型企業來說,採用該技術可能很困難。為了解決成本問題,製造商正在尋找使蒸餾包裝過程更加高效且更具成本效益的方法。

- 由於冠狀病毒 -19 供應鏈感染疾病和先前的封鎖,紙板在全球範圍內變得越來越難找到。基於此,2020年紙包裝開始漲價,價格還在上漲。此後,這些問題進一步惡化,俄羅斯對烏克蘭形勢的干涉導致造紙原物料價格升至創紀錄水平。多國對俄羅斯實施經濟制裁,導致大宗商品價格上漲、供應鏈中斷,並因俄烏戰爭而對多個世界市場造成影響。俄羅斯和烏克蘭之間的衝突不僅顯著改變了貿易格局,也嚴重影響了人們的生活和生存手段。能源成本和石油價格上漲正在推高全球供應鏈中塑膠樹脂的價格。然而,聚合物產業因2022年俄羅斯入侵烏克蘭而佔據主導地位。市場供應商面臨的主要挑戰是石油和天然氣價格波動導致國內市場原料成本波動。

蒸餾包裝市場趨勢

飲料增速顯著

- 軟包裝解決方案(例如蒸餾包裝)在減少廢棄物方面發揮重要作用,並使線上品牌能夠創新其包裝並改善電子商務體驗。在飲料領域,由於易於處理以及生產和出貨成本降低,對蒸餾包裝的需求正在增加。

- 殺菌袋軟質包裝是一種由耐熱層壓塑膠製成的軟包裝,在確保減少飲料和產品廢棄物的同時,在幫助線上品牌創新包裝以改善電子商務體驗方面發揮關鍵作用。

- 輕質包裝材料對於飲料尤其是袋裝至關重要。改良的袋設計擴大了其用途,並促使更多消費者購買果汁食品、營養補充、代餐奶昔、纖維補充品和冷壓果汁。

- 然而,飲料品質受到 pH 值、儲存溫度、壓力和污染物存在的影響。殺菌袋包裝無需使用防腐劑即可對飲料進行滅菌,從而保持 pH 值在 4.0 至 7.0 之間的飲料產品的品質和安全性。公司擴大採用具有阻隔性(耐熱、防潮和抗菌)和消除氧化可能性等特性的包裝產品。

- 消費者對健康和保健的意識越來越強。從早晨果汁到能量飲料,消費者現在在符合健康趨勢的提神產品上花費更多。這使得飲料行業對具有成本效益的包裝解決方案產生了很高的需求。

- 英國國家統計局的數據顯示,2022 年第一季消費者在食品和非酒精飲料上的支出超過 290 億英鎊(352.6 億美元)。 2019 年第一季家庭金額約 270 億英鎊(328 億美元)。消費者支出的增加可能會推動蒸餾飲料銷售和產量的增加,這可能會增加對包裝材料的需求。對蒸餾飲料包裝不斷成長的需求使該行業的公司有可能提高製造能力並生產尖端的包裝解決方案。

預計北美將佔據重要市場佔有率

- 城市人口的增加、工作生活的繁忙、單人家庭的增加以及人口購買力的提高正在推動現成產品的成長,這些產品通常採用自立式殺菌袋,從而成為重要的推動力。殺菌袋的成長,也給了我力量。行業。

- 蒸餾包裝作為一種方便、攜帶的包裝解決方案正在迅速普及。與傳統的硬質包裝相比,這個國家的許多消費者更喜歡靈活的立式袋。在過去的十年中,消費者對休閒食品、飲料、嬰兒食品、工業油和潤滑油等產品的立式袋的需求急劇增加。

- 在美國,衛生與公共服務部負責監管人類和動物消費的食品、藥品和營養補充。這是透過美國食品藥物管理局(FDA) 或美國農業部 (USDA) 完成的。用於蒸餾包裝的法規在最高溫度下非常嚴格,並要求材料和工藝符合 FDA 法規 21 CFR 177.1390。

- 許多行業,包括零售、製藥、食品飲料和寵物食品,都擴大採用軟包裝技術,加拿大正在推廣殺菌袋的使用。

- 在這個國家,大約 75% 的食品供應來自包裝食品和加工食品。飲食習慣也發生了變化,中國增加了即食、超加工食品的消費量,這些食品通常富含脂肪、糖和鈉,而且能量密集。這些食品主要包裝在殺菌袋,因為這是包裝需要長期儲存的食品的有效技術。

蒸餾包裝產業概述

蒸餾包裝市場競爭激烈,由多家大公司組成。從市場佔有率來看,目前很少大公司佔據市場主導地位。然而,憑藉創新和永續的包裝,許多公司正在透過贏得新合約和開拓新市場來擴大其市場佔有率。

2022 年 6 月,斯道拉恩索和利樂合作開發飲料紙盒回收解決方案。斯道拉恩索比利時朗格布魯日工廠回收工廠的設計是聯合可行性研究的一部分。每年約有 75,000 噸飲料紙盒抵達比荷盧市場。其中 70% 以上已被收集用於回收。

2022 年 4 月,ProAmpac 推出了其標誌性的 ProActive PCR殺菌袋。 ProActive PCR殺菌袋用於包裝寵物和人類食品,並已獲得 FDA 和 EU核准,可用於蒸餾應用中的食品接觸。為了減少包裝中原始樹脂的使用,ProActive PCR殺菌袋含有超過 30 重量%的 PCR 含量。此外,這些發明的袋子符合英國(UK) 塑膠包裝稅 (PPT) 標準。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- COVID-19 對產業的影響

- 市場促進因素

- 對輕質緊湊包裝材料的需求不斷成長

- 包裝食品產業的永續發展

- 市場挑戰

- 增加資本投入和原物料回收問題

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按包裝類型

- 小袋

- 紙盒

- 托盤

- 其他類型

- 按材質

- 聚丙烯

- 聚酯纖維

- 鋁箔

- 紙板

- 尼龍

- 食品級鑄塑聚丙烯

- 其他材料

- 按最終用戶材料

- 食品

- 飲料

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 公司簡介

- Amcor PLC

- Constantia Flexibles

- Clifton Packaging Group Limited

- Clondalkin Industries BV

- Coveris Holdings SA

- Flair Flexible Packaging Corporation

- Mondi PLC

- Tetra Pak International SA

- Proampac LLC

- Sonoco Product Company

- Winpak Ltd

- Sealed Air Corporation

第7章 投資分析

第8章 市場未來展望

The Retort Packaging Market size is estimated at USD 5.45 billion in 2024, and is expected to reach USD 7.75 billion by 2029, growing at a CAGR of 7.29% during the forecast period (2024-2029).

Key Highlights

- There is a rising demand for ready-to-eat meals as a result of a number of causes, including changing lifestyles, long workdays, and increased urbanization. Many customers are searching for quick and simple meal options that can be made in a matter of minutes without compromising on taste or quality. For consumers who are busy and want to save time and effort, ready meals provide an easy, simple answer. Retort packaging has expanded due to products in pouches and trays since many consumers choose packaging options for on-the-go consumption. Retorting purses and bags makeup about 60% of all food packaging worldwide, according to the Flexible Packaging Association.

- The US Census Bureau reports that from September 2022 to December 2022, there was a rise in the monthly retail sales of food and drink in the US. In September 2022, the sale was valued at USD 78,216 million. In December 2022, it was worth an astounding USD 88,432 million. In the coming years, it is anticipated that this tendency will continue. Retort packaging demand is therefore anticipated to expand during the projection period as a result of the market's progressive increase in retail sales demand.

- Consumers' initial hesitation of overpaying for pets is progressively giving way to trends like pet humanization and sensitization, which are clearly shown in the sharp increase in adoption rates. Retort pouches are becoming more and more popular all over the world as a result of the expanding use of flexible packaging techniques in a variety of sectors, including retail, pharmaceutical, food and beverage, and pet food.

- However, one key difficulty in the retort packaging industry is the high cost of manufacturing retort packaging materials. Retort packaging is strong and able to survive high temperatures since it is comprised of plastic, aluminium, and other materials. However, the price of these materials and the need for specialized machinery and production methods to create them drive up manufacturing prices. Adopting this technique may be challenging for small enterprises with tight resources due to the high cost of retort packing. Manufacturers are searching for ways to improve the efficiency and cost-effectiveness of the retort packaging process to meet cost issues.

- Due to COVID-19 supply chain issues and earlier lockdowns, finding paper boards has grown increasingly challenging on a global scale. In light of this, a hike in the price of paper packaging began in 2020 and is still in force today. Since then, these problems have gotten worse, and because of Russia's interference in the Ukrainian situation, the price of raw paper materials has increased to record levels. Economic sanctions imposed on Russia by a number of countries have caused a rise in commodity prices, interruptions in the supply chain, and effects on several global markets as a result of the war between Russia and Ukraine. The conflict between Russia and Ukraine has had a profound effect on people's life and means of subsistence, as well as greatly altered trade patterns. The price of plastic resins is increasing across the whole global supply chain as a result of rising energy costs and oil prices. However, the polymer industry was dominated by Russia's invasion of Ukraine in 2022. A major challenge for market vendors is the varying cost of raw materials on the domestic market as a result of fluctuations in the price of oil and gas.

Retort Packaging Market Trends

Beverages to Witness Significant Growth Rate

- Flexible packaging solutions, such as retort packaging, play a crucial role in reducing waste and allows online brands to innovate their packaging to enhance the e-commerce experience. There is a high demand for retort packaging in the beverage sector due to factors such as ease of handling and reduced production and shipment costs.

- Made from heat-resistant laminated plastic, retort pouch packaging, a form of flexible packaging, plays a crucial role in ensuring the reduction of beverage and product waste while allowing online brands to innovate their packaging to enhance the e-commerce experience simultaneously.

- Lightweight packaging material is essential for beverages, particularly in pouches. The improving designs of pouches increased their applications, attracting more consumers to purchase fruit drinks, nutraceuticals, meal replacement shakes, fibre supplements, and cold-pressed juices.

- However, the quality of beverages is affected by pH, storage temperature, pressure, and contaminants' presence. Retort pouch packaging sterilizes beverages by preserving the quality and safety of beverage products with pH levels between 4.0 and 7.0 without using preservatives. Companies are increasingly employing packaging products with properties such as barrier resistance (to heat, moisture, and bacteria) and to eliminate possible oxidation.

- Consumers are becoming increasingly conscious of health and wellness. From juice in the morning to energy drinks, consumers now are spending more on products that provide refreshments that are well within the wellness trend. This has created a high demand for cost-effective packaging solutions in the beverage segment.

- In the first quarter of 2022, consumer spending on food and non-alcoholic drinks amounted to over GBP 29 billion (USD 35.26 billion), according to the Office for National Statistics (UK). The amount of money spent by households in the first quarter of 2019 was around GBP 27 billion (USD 32.8 billion). Increased sales and manufacturing of retort drinks might result from rising consumer expenditure, which would increase the need for packaging materials. Companies in this industry may be able to boost their manufacturing capabilities and produce cutting-edge packaging solutions as a result of the rising demand for retort beverage packaging.

North America is Expected to Hold Significant Market Share

- Increased urban population, busy work life, growing single households, and increasing spending power of the population have boosted the growth of readymade, which are normally packaged in stand-up retort pouches, thereby also acting as key drivers for the growth of the retort pouch industry.

- Retort packaging has been rapidly gaining popularity, as it is a highly convenient and portable packaging solution. Many shoppers in the country prefer flexible, stand-up pouches over traditional, rigid packaging. Consumers have driven demand for stand-up pouches exponentially over the past decade, whether for snack food, beverage, baby food, or industrial oils and lubricants.

- In the United States, the Department of Health and Human Services regulates food, pharmaceutical, and nutraceutical products consumed by humans and animals. This is done through either the Food and Drug Administration (FDA) or the US Department of Agriculture (USDA). The regulation used for retort packages is quite demanding under the highest temperatures and requires the materials and processes to be listed under FDA regulation 21 CFR 177.1390.

- The growing adoption of flexible packaging techniques across numerous industries, including retail, pharmaceutical, food and beverage, and pet food, is propelling the use of retort pouches in Canada.

- In the country, about 75% of the food supply comes from packaged, processed food items. Also, there is a change in eating habits, and the country is witnessing an increase in consumption of ultra-processed, ready-to-consume foods, which are typically energy-dense with high fat, sugar, and sodium content. These food are mostly packed in retort pouches as it provides an effective technique for packaging food products that require extended shelf life.

Retort Packaging Industry Overview

The retort packaging market is highly competitive and consists of several major players. In terms of market share, few of the major players currently dominate the market. However, with innovative and sustainable packaging, many companies are increasing their market presence by securing new contracts and by tapping new markets.

In June 2022, Stora Enso and Tetra Pak joined forces on a beverage carton recycling solution. A design for a recycling plant at Stora Enso's Langerbrugge location in Belgium is part of the joint feasibility study. The Benelux market receives around 75,000 tonnes of beverage cartons annually. More than 70% of these have already been collected for recycling.

In April 2022, ProAmpac introduced its distinctive ProActive PCR Retort pouches. ProActive PCR Retort pouches are made for packaging pet and human food, and they are both FDA and EU-approved for food contact in retort applications. In order to reduce the usage of virgin resins in the packaging, ProActive PCR Retort pouches have a 30-weight percentage or higher PCR content. Additionally, these inventive pouches are Plastics Packaging Tax (PPT) compliant for the United Kingdom (UK).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Impact of COVID-19 on the Industry

- 4.3 Market Drivers

- 4.3.1 Growing Demand for Lightweight and Compact Packaging Materials

- 4.3.2 Sustained Growth in the Packaged Food Industry

- 4.4 Market Challenges

- 4.4.1 Higher Capital Investments and Raw Material Recycling Issues

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Packaging Type

- 5.1.1 Pouches

- 5.1.2 Cartons

- 5.1.3 Trays

- 5.1.4 Other Types

- 5.2 By Material

- 5.2.1 Polypropylene

- 5.2.2 Polyester

- 5.2.3 Aluminum Foil

- 5.2.4 Paper Board

- 5.2.5 Nylon

- 5.2.6 Food Grade Cast Polypropylene

- 5.2.7 Other Materials

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Other End-User Industry

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Mexico

- 5.4.4.2 Brazil

- 5.4.4.3 Argentina

- 5.4.4.4 Rest of Latin America

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle-East & Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor PLC

- 6.1.2 Constantia Flexibles

- 6.1.3 Clifton Packaging Group Limited

- 6.1.4 Clondalkin Industries BV

- 6.1.5 Coveris Holdings SA

- 6.1.6 Flair Flexible Packaging Corporation

- 6.1.7 Mondi PLC

- 6.1.8 Tetra Pak International SA

- 6.1.9 Proampac LLC

- 6.1.10 Sonoco Product Company

- 6.1.11 Winpak Ltd

- 6.1.12 Sealed Air Corporation

7 INVESTMENT ANALYSIS

8 FUTURE OUTLOOK OF THE MARKET

至 2030 年蒸煮包裝市場預測 - 各產品類型(紙箱、袋子、托盤和其他包裝類型)、材料、封閉類型、配銷通路、應用、最終用戶和地理位置的全球分析

至 2030 年蒸煮包裝市場預測 - 各產品類型(紙箱、袋子、托盤和其他包裝類型)、材料、封閉類型、配銷通路、應用、最終用戶和地理位置的全球分析 2024 年蒸餾設備世界市場報告

2024 年蒸餾設備世界市場報告 殺菌機市場依製程(批量滅菌、連續滅菌)、應用(乳製品、肉類及海鮮、飲料、穀物及豆類等)及地區分類2024-2032年

殺菌機市場依製程(批量滅菌、連續滅菌)、應用(乳製品、肉類及海鮮、飲料、穀物及豆類等)及地區分類2024-2032年 全球蒸煮包裝市場 - 2023-2030

全球蒸煮包裝市場 - 2023-2030 蒸餾包裝市場:按類型、材料和最終用戶分類:2023-2032 年全球機會分析和產業預測

蒸餾包裝市場:按類型、材料和最終用戶分類:2023-2032 年全球機會分析和產業預測 殺菌包裝市場:依產品種類、依材料類型、依最終用途產業、蒸餾類型、依地區

殺菌包裝市場:依產品種類、依材料類型、依最終用途產業、蒸餾類型、依地區 煮沸袋市場:按材料、外觀、應用分類 - 2023-2030 年全球預測

煮沸袋市場:按材料、外觀、應用分類 - 2023-2030 年全球預測 全球蒸煮包裝市場

全球蒸煮包裝市場 蒸餾包裝的全球市場 2023-2027

蒸餾包裝的全球市場 2023-2027 蒸煮包裝市場 - 2018-2028 年全球行業規模、佔有率、趨勢、機會和預測,按材料(聚丙烯、鋁箔、聚醯胺、其他)、包裝類型、應用、地區和競爭分類

蒸煮包裝市場 - 2018-2028 年全球行業規模、佔有率、趨勢、機會和預測,按材料(聚丙烯、鋁箔、聚醯胺、其他)、包裝類型、應用、地區和競爭分類