|

市場調查報告書

商品編碼

1432899

契約包裝:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Contract Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

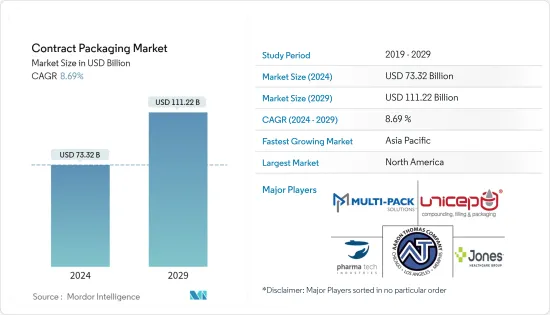

契約包裝市場規模預計到 2024 年為 733.2 億美元,預計到 2029 年將達到 1112.2 億美元,在預測期內(2024-2029 年)複合年成長率為 8.69%。

隨著 COVID-19 大流行的爆發,合同包裝市場正在見證巨大的增長。 由於隔離和社交距離規範導致大多數消費者更喜歡在線購物管道,電子商務市場正在蓬勃發展,公司將端到端或獨立的包裝服務外包以滿足不斷增長的需求。

主要亮點

- 然而,疫情影響了各公司的自動化計劃,對所研究的市場影響甚微。根據包裝和加工技術協會 (PMMI) 的一項研究,大約 67% 的 CPG 公司已擱置其自動化計劃。

- 全球契約包裝市場的成長主要受到製造公司偏好的影響,這些公司通常將包裝任務委託給第三方供應商。這是因為製造商越來越關注成本最佳化和核心業務。契約包裝有幾個優點。首先,它降低了製造商的營運成本。在許多情況下,估計透過將包裝業務委託給契約包裝公司並減少機械和人事費用,營運成本可降低多達7%至9%。

- 其次,包裝法規正在迅速發展,尤其是食品和飲料。 為了滿足這些嚴格的規則和規範,有必要進行大量的檢查和品質檢查操作。 通過外包包裝業務,滿足此類法規(也稱為軍用規格包裝)的繁忙工作被合同包裝所取代,從而激勵更多製造商更喜歡外包包裝而不是內部包裝業務。

- 此外,包裝產業發展迅速,許多新產品、新技術不斷推出。因此,包裝公司需要隨時了解情況,以滿足不斷變化的客戶需求。都市化、可支配收入增加以及對方便且易於打開的包裝的偏好因素正在塑造市場新趨勢。

- 消費者對環境議題的認知不斷提高,加上生產商對經濟型包裝選擇的需求,正在推動契約包裝商採用地球友善替代品和環保包裝設計。此外,永續性和客製化將繼續對契約包裝市場產生積極影響,其在個人護理、食品和飲料等消費包裝商品中的使用在預測期內可能會成長。 2020 年 6 月,CPA、契約包裝商和製造商協會以及歐洲包裝商協會 (ECPA) 聯手提高各自地區對契約包裝和契約製造的認知和利用。這為協會成員提供了投資新技術並在業務中實施永續性的機會。

- 供應商還專注於收購和地域擴張,以保持其在市場上的存在,這導致了市場的逐步整合。 例如,2020 年 3 月,溫斯頓-塞勒姆的 South Atlantic Packaging, Inc. (SAPC) 收購了總部位於佛羅里達州的 Versatile Packagers,這是一家提供包裝、配套、組裝和倉儲解決方案的合同包裝公司。 對於SAPC來說,這是一個很棒的位置。

契約包裝市場趨勢

醫藥可望維持強勁成長

- 製藥業的進步和研究的發展促使了性能優於前輩的新藥的推出。隨著對包裝藥物的需求迅速增加,最近的醫學進步以及許多疾病和缺陷的現有藥物的補充正在間接推動契約包裝市場。

- 各種製藥公司現在將最終產品的包裝委託給擁有專門從事藥品包裝的熟練業務的公司。藥品包裝是至關重要的方面,因為產品必須對患者安全食用。

- 據估計,到年終,近 50 種處方箋的處方藥將在北美專利到期,這為契約包裝商創造了機會。患者依從性和用藥依從性差會導致住院率增加和疾病惡化。製造商對藥品安全和保護的持續關注以及政府法規的更新是包裝外包要求的因素。根據美國食品藥物管理局(FDA) 的規定,藥品需要高阻隔的包裝材料和密封劑,這些材料和密封劑具有防滲性、耐溶劑、油脂、化學品和耐熱性,以提供更好的保護。

- 自2020年2月下旬以來,美國藥品製造商因對中國的依賴而面臨供不應求的高風險,這種情況可能會持續未來三個月。同時,FDA 已要求美國藥品和醫療設備製造商評估和規劃 API 採購替代方案。

- 在醫療設備方面,FDA 已對中國各地的 63 家製造商和 72 家工廠進行了認證,並已聯繫這些工廠增加基本設備的庫存,以避免供應中斷時短缺。然而,與這些措施相反,原料藥供應製造商 C2 Pharma 認為,美國政府對冠狀病毒的反應可能會促使該國藥品供應鏈的重組。

北美地區佔比最大

- 由於食品和飲料、藥品和美容護理等行業對包裝的需求不斷增加,北美的契約包裝行業正在快速成長。美國和加拿大的各種契約包裝公司已經學會適應充滿課題的商業環境。該公司也意識到激烈的全球競爭、成本壓力以及OEM的高度可變的需求。這種環境正在顯著擴大美國契約包裝市場。許多歐洲公司已經在美國投資,包括蘭根集團和佩爾森創新公司。

- 由於這種穩定性、不斷成長的需求以及製造公司對契約包裝供應商的偏好不斷變化,美國契約包裝市場預計將穩定成長。此外,美國政府制定了有關藥品標籤和包裝的各種法律和法規。此外,美國政府制定了有關藥品標籤和包裝的各種法律和法規,這可能會對契約包裝的需求產生積極影響,因為該地區的製藥公司沒有內部包裝設施。

- 2020 年 2 月,大型飲料合約製造公司 (BBCM) 宣佈在北卡羅來納州開設一家新的飲料聯合包裝工廠。 BBCM 的新工廠將從一條每分鐘生產 1,200 罐的高速罐頭生產線開始,並計劃在未來 18 個月內增加第二條和第三條生產線。 BBCM 計劃向全國和地區的大型客戶提供各種罐裝飲料產品。 BBCM計劃於2020年第二季末全面運作,第一條生產線已售出80%。

- 2020 年 1 月,MSI Express 在美國HCI Equity Partners 的支持下收購了 Power Packaging。 MSI Express 為耐貯存的人類和寵物食品領域的知名品牌提供契約包裝和契約製造服務。透過收購 Power Packaging,MSI Express 進一步擴大了其地理分佈、能力和客戶關係。收購 Power 也將 MSI Express 擴展到新的食品類別,如粉狀飲料、湯底、烘焙混合物、飲料混合物、咖啡和茶、餐飲服務飲料、晚餐套件、義式麵食、米飯、預製食品和沙拉醬。參與。

契約包裝產業概述

契約包裝市場適度分散,擁有大量國內外供應商。該市場中的公司透過聯盟和合併不斷擴大其接近性。隨著各種老牌公司和中小企業外包活動的成長,調查市場在提供可靠、及時的服務方面正面臨著巨大的競爭,而競爭已成為一個市場。總體而言,替代品的威脅是溫和的,預計在預測期內將會成長。

- 2020 年 6 月 - Jones Healthcare Group 對其包裝服務產品進行了重大投資,包括一條完全集成的雙通道 Uhlmann 泡罩包裝線。 隨著臨床和商業上更複雜的藥物劑型和制度的發展,這種全自動設施將提高我們應對激增的需求和獨特的泡罩組合的能力。

- 2020 年 5 月 - 夏普 (UDG Healthcare PLC) 從 Quality Packaging Specialist International LLC (QPSI) 手中收購了一家藥品包裝設施。 該設施佔地 160,000 平方英尺,已獲得完全監管授權。 我們在多條二級包裝線上擁有12個初級生產基地,提供一級和二級藥品包裝,包括裝瓶、泡泡、小瓶標籤和醫療器械配套,以及序列化服務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 尋求透過外包非核心業務來獲得競爭優勢的公司

- 電商產業需求增加

- 對尖端技術和創新包裝的需求不斷成長

- 市場限制因素

- 嚴格的政府法規

- 與內部包裝的競爭

- 行業法規和標準

- 契約包裝的演變

第6章市場區隔

- 依包裝

- 初級包裝

- 二次包裝

- 三級包裝

- 依最終用戶產業

- 食品

- 飲料

- 藥品

- 家居用品/個人護理

- 其他最終用戶產業

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第7章 競爭形勢

- 公司簡介

- Aaron Thomas Company

- Multipack Solutions LLC

- Pharma Tech Industries Inc.

- Reed Lane Inc.

- Sharp Packaging Services

- UNICEP Packaging LLC

- Green Packaging Asia

- Jones Healthcare Group

- Stamar Packaging Inc.

- Budelpack Poortvliet BV

- Complete Co-Packing Services Ltd

第8章投資分析

第9章 未來展望

The Contract Packaging Market size is estimated at USD 73.32 billion in 2024, and is expected to reach USD 111.22 billion by 2029, growing at a CAGR of 8.69% during the forecast period (2024-2029).

With the outbreak of the COVID-19 pandemic, the contract packaging market has witnessed tremendous growth, as the e-commerce market has taken a boom, owing to lockdown and social distancing norms where the majority of the consumers has been preferring online channel for shopping, and companies have been outsourcing their packaging end to end or standalone services to meet the growing demand.

Key Highlights

- However, the pandemic impacted the automation plans for various company, which has some minimalistic effect in the market studied. According to the Association for Packaging and Processing Technologies (PMMI) survey, around 67% of CPG companies have put automation plans on hold than win comparison to 23% of SMEs.

- Growth in the global contract packaging market is mainly influenced by the changing preferences of manufacturing firms, who usually outsource packing activities to third-party players. This is because manufacturers are increasingly focusing on cost optimization and their core business. Contract packaging provides several advantages. Firstly, it reduces the operational costs of the manufacturers. In many cases, it is estimated that the operational costs can be reduced by as much as 7% to 9% through outsourcing packaging activities to contract packagers and the decreasing costs of machines and labor costs.

- Secondly, packaging regulations, especially in the case of food and beverage products, are evolving rapidly. Meeting such stringent rules and norms require several inspection and quality check operations. By outsourcing packaging activities, the hectic task of meeting such regulations (also known as mil-spec packaging) is passed on to the contract packaging agency, motivating more manufacturers to prefer contract package over in-house packaging activities.

- Moreover, the packaging industry is rapidly growing, with many new products and technologies being introduced. Therefore, packaging companies need to stay updated to meet the changing needs of customers. Factors, such as urbanization, increasing disposable incomes, and preference for convenient and easy-to-open packages, shape new trends in the market.

- Raising consumer awareness about environmental concerns, along with the producers' demand for economical packaging options, is impelling contract packagers to adopt earth-friendly alternatives and eco-sensitive package designs. Furthermore, sustainability and customization are likely to continue to positively impact the contract packaging market, leading to growth in use in consumer-packaged goods, such as personal care and food and beverages, over the forecast period. In June 2020, CPA, The Association for Contract Packagers, and Manufacturers and The European CoPackers Association (ECPA) collaborated to increase the awareness and use of the contract packaging and contract manufacturing industry in their respective regions. This presents an opportunity for the members of each organization to invest in new technologies and introduce sustainability into their operations.

- To remain relevant in the market, vendors are also focusing on acquisitions and geographical expansions, due to which the market is gradually consolidating. For instance, in March 2020, South Atlantic Packaging Corp. (SAPC) in Winston-Salem, a contract packaging company that offers to package, kitting, assembly, and warehousing solutions, bought Florida-based Versatile Packagers. It provides an excellent location for SAPC.

Contract Packaging Market Trends

Pharmaceutical is Expected to Hold Significant Growth

- The growth in advancement and research in the pharmaceutical industry has resulted in the introduction of new drugs, with more exceptional performance compared to their predecessors. Recent improvements in medical sciences and additions to medicines already available for numerous diseases and deficiencies drive the contract packaging market, indirectly, as the necessity of packaging the drugs has multiplied rapidly.

- Various pharmaceutical companies are now outsourcing the job of packaging end-products to companies skilled labor specialized in handling the packaging of medicines. The pharmaceutical packaging of drugs is a vital aspect, as the product should be safe for patient's consumption.

- In North America, it is estimated that by the end of 2020, nearly 50 well-known, highly-prescribed drugs will go off-patent, which creates opportunities for contract packagers. Poor patient compliance or medication adherence can lead to increased hospitalization and worsening of the disease. Manufacturers' ongoing focus on drug safety and protection, and the latest government regulations, are the factors for the outsourcing packaging requirements. As per the Food and Drug Administration (FDA) regulations in the United States, pharmaceutical drugs need high barrier packaging materials and sealants that are impermeable and resistant to solvents, grease, chemicals, and heat for better security protection.

- Since late February 2020, U.S. pharmaceutical manufacturers, being dependent on China, have a high risk of supply shortages, which may continue over the next three months. In the meantime, the FDA asked U.S. pharmaceutical and medical device manufacturers to evaluate and plan for API sourcing alternatives.

- Concerning medical devices, FDA recognized 63 manufacturers and 72 facilities across China, which were contacted for essential devices inventory pileup, to avoid shortage in case of a supply disruption. However, contrary to such measures being taken, C2 Pharma, an API supplier outsourcing manufacturer, observed that the U.S. government's coronavirus response could realign the country's pharmaceutical supply chain.

North America to Account for the Largest Share

- The contract packaging sector in North America is rapidly growing due to the increasing demand for packaging in segments, like food and beverages, pharmaceuticals, beauty care, and other sections. Various contract packaging companies in the United States and Canada have learned to adapt to challenging business conditions. The companies are also getting aware regarding the intense global competition, cost pressures, and highly variable demand from OEMs. This environment is significantly increasing the contract packaging market in the United States. Many European companies, such as Langen Group and Persson Innovation, have already invested in the United States.

- Owing to the stability, rising demand, and changing the preference of manufacturing firms toward contract packagers, the U.S. contract packaging market is expected to witness steady growth. Also, the U.S. government has placed various laws and regulations on the labeling and packaging of the drugs. This could create a positive impact on the demand for contract packaging, owing to the inability of an in-house packaging facility for few pharmaceutical companies in this region.

- In February 2020, Big Beverages Contract Manufacturing (BBCM) announced the opening of its new beverage co-packing facility in North Carolina. In their new facility, BBCM will begin with one highspeed can-line capable of producing 1,200 cans per minute with plans to add lines two and three over the next 18 months. BBCM plans to provide a variety of canned beverage products for large national and regional customers. BBCM will be fully operational in late Q2 2020, and its first production line is 80% sold out.

- In January 2020, MSI Express, backed by HCI Equity Partners, which is headquartered in the United States, has acquired Power Packaging. MSI Express is a provider of contract packaging and contract manufacturing services for well-known brands in the shelf-stable human and pet food space. The acquisition of Power Packaging further expands MSI Express's geographical presence, capabilities, and customer relationships. Power also brings MSI Express into new food categories such as powdered beverages, soups and bases, baking mixes, beverage mixes, coffees and teas, foodservice beverages, dinner kits, pasta, rice, side dishes, and salad dressings.

Contract Packaging Industry Overview

The contract packaging market is moderately fragmented, with the presence of many domestic and international vendors. The companies in the market are continually expanding their geographical proximity with the help of partnerships and mergers. With the growth of outsourcing activities among various established players, as well as SMB, the market studied has been witnessing significant competition, in terms of providing reliable and speed of services, making it a competitive market. Overall, the threat of substitutes is moderate and is expected to grow during the forecast period.

- June 2020 - Jones Healthcare Group made a major investment in its packaging services offering which includes a fully integrated two-lane Uhlmann blister packaging line. The fully automated equipment will improve the firm's capacity to manage surges regarding the demand and unique blister combinations, as more complex pharmaceutical dosage forms and regimes are evolving clinically and commercially.

- May 2020 - Sharp (UDG Healthcare PLC) acquired a pharmaceutical packaging facility from Quality Packaging Specialists International LLC (QPSI). The facility covers an area of 160,000 sq. ft and has full regulatory approval. It encompasses 12 primary production sites for multiple secondary packaging lines to offer both primary and secondary pharmaceutical packaging, including bottling, blistering, vial labeling, and medical device kitting, as well as serialization services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Companies Looking to Gain Competitive Advantage by Outsourcing Non-core Operations

- 5.1.2 Increasing Demand from the E-commerce Industry

- 5.1.3 Increasing Need for Latest Technology and Innovative Packaging

- 5.2 Market Restraints

- 5.2.1 Stringent Government Regulations

- 5.2.2 Competition from In-house Packaging

- 5.3 Industry Regulations and Standards

- 5.4 Evolution of Contract Packaging

6 MARKET SEGMENTATION

- 6.1 By Packaging

- 6.1.1 Primary

- 6.1.2 Secondary

- 6.1.3 Tertiary

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Pharmaceutical

- 6.2.4 Household and Personal Care

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Netherlands

- 6.3.2.5 Italy

- 6.3.2.6 Spain

- 6.3.2.7 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Aaron Thomas Company

- 7.1.2 Multipack Solutions LLC

- 7.1.3 Pharma Tech Industries Inc.

- 7.1.4 Reed Lane Inc.

- 7.1.5 Sharp Packaging Services

- 7.1.6 UNICEP Packaging LLC

- 7.1.7 Green Packaging Asia

- 7.1.8 Jones Healthcare Group

- 7.1.9 Stamar Packaging Inc.

- 7.1.10 Budelpack Poortvliet BV

- 7.1.11 Complete Co-Packing Services Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

合約包裝與履行服務 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)

合約包裝與履行服務 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029) 全球合約包裝市場 2024-2028

全球合約包裝市場 2024-2028 受託包裝市場:依包裝、依最終用戶行業、依地區

受託包裝市場:依包裝、依最終用戶行業、依地區 受託包裝的全球市場,預測(2030年)

受託包裝的全球市場,預測(2030年) 化學契約包裝服務市場:2019-2029年全球市場規模、佔有率、趨勢分析、機遇和預測報告

化學契約包裝服務市場:2019-2029年全球市場規模、佔有率、趨勢分析、機遇和預測報告 合約包裝市場:按包裝材料(一級、二級、三級)、最終用戶(食品和飲料、家居用品和個人護理)分類 - 全球預測 2023-2030 年

合約包裝市場:按包裝材料(一級、二級、三級)、最終用戶(食品和飲料、家居用品和個人護理)分類 - 全球預測 2023-2030 年 受託包裝的按全球市場規模:各用途,各材料,包裝,各產品,各類服務 - 地區預測,競爭策略,市場區隔預測(~2032年)

受託包裝的按全球市場規模:各用途,各材料,包裝,各產品,各類服務 - 地區預測,競爭策略,市場區隔預測(~2032年) 受託包裝的全球市場

受託包裝的全球市場 合同包裝市場:2023-2028 年全球行業趨勢、份額、規模、增長、機遇和預測

合同包裝市場:2023-2028 年全球行業趨勢、份額、規模、增長、機遇和預測 受託包裝的全球市場的分析·預測 (~2028年):包裝類型·材料·服務·終端用戶·各地區

受託包裝的全球市場的分析·預測 (~2028年):包裝類型·材料·服務·終端用戶·各地區