|

市場調查報告書

商品編碼

1432911

綠色資料中心:市場佔有率分析、產業趨勢、成長預測(2024-2029)Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

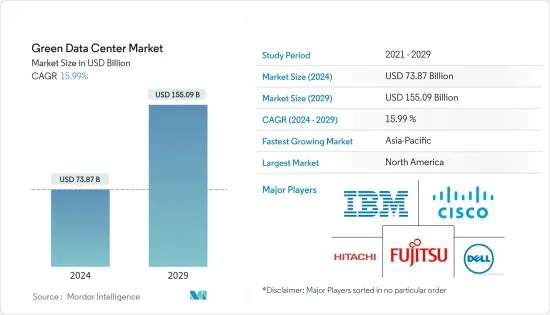

綠色資料中心市場規模預計到2024年為738.7億美元,預計到2029年將達到1550.9億美元,在預測期內(2024-2029年)複合年成長率為15.99%。

主要亮點

- 全球綠色資料中心市場預計未來五年將從目前的576.3億美元增加到1,200億美元。多年來,對資料中心能源消耗比例不斷增加的擔憂,提醒世界各國政府對能源消耗進行監管,這成為推動綠色資料中心市場的主要因素。資料中心和主機代管服務的成長也是推動綠色資料中心的其他因素。

- 隨著雲端運算變得更加節能並更加依賴可再生能源,其他行業如製造、交通和建築也正在轉向綠色資料中心以減少排放,預計這種情況將會發生。例如,汽車製造商可以委託所有內部計算外包給零排放資料中心。

- 對資料儲存和儲存空間的需求不斷成長是推動綠色資料中心需求的關鍵因素。據華為稱,預測期內全球資料中心需求預計將成長3倍至10倍。綠色資料中心為資料儲存和減少能耗提供了實用且環保的解決方案,由於資料中心儲存需求和新建的前景光明,預計綠色資料中心的需求量很大。

- 此外,隨著人工智慧(AI)、機器學習(ML)、巨量資料和物聯網(IoT)的興起,全球資料中心的電力消耗量持續增加,這也是綠色資料中心的另一個原因。是一個促進因素。根據國際能源總署(IEA)的數據,資料中心的電力消耗佔全球電力消耗的1-1.5%。因此,對能源效率的強烈關注可能會推動市場。

- 儘管可以實現長期節省和投資回報,但可再生能源資料中心的初始投資成本很高。建設節能綠色資料中心的初期投資高於傳統資料中心。要改變現有的基礎設施,企業需要更高的投資,這是一種負擔。然而,企業願意投資綠色資料中心,即使他們可以透過改善擁有成本和長期節省來收回初始投資。

- 由於雲端資料中心服務的加速、對資料中心自動化的依賴增加、硬體重用增加作為關鍵課題以及資料中心硬體的再行銷增加等因素,COVID-19正在成為一個更加綠色的市場。- 預計將推動資料中心要求。鑑於 COVID-19 帶來的環境意識增強以及組織資料流量和巨量資料分析的增加,這一趨勢將在大流行後繼續成長。

綠色資料中心市場趨勢

電力領域佔據主要市場佔有率

- 綠色資料中心的建立是為了最大限度地提高能源效率並減少對環境的影響。資料中心電力消耗和冷卻問題是全球企業面臨的兩個最關鍵問題,隨著在這方面的大量投資,提高能源效率已成為關鍵需求。控制這些營運成本對於改善業務營運和維持市場競爭力至關重要。

- 電力在綠色資料中心投資中發揮關鍵作用。低功耗和有效的解決方案可以幫助企業實現目標。採用變速風扇是減少資料中心能耗的技術。根據最近的一項研究,降低中央處理器 (CPU) 風扇的速度可以減少 20% 的功耗。因此,企業應採用變速風扇來冷卻資料中心設備並減少能源使用。

- 資料中心能源成本超過機房及輔助設備的全部投資。然而,最近的研究表明,隨著美國和歐洲成熟市場採取有效的綠色效率措施,這一趨勢正在放緩。

- 伺服器虛擬,透過將伺服器切換到靠市電運作的經濟模式,將實體伺服器用作池,提高伺服器利用率,整合空間和設備,並減少資料中心內所需的實體伺服器數量。從而降低消費量。由於使用的伺服器較少,因此電力和冷卻要求降低,能耗也顯著降低。

- 隨著資料中心用電量的增加、申請的上漲以及二氧化碳排放的增加,對綠色資料中心的需求不斷增加並推動市場的發展。根據Uptime Institute進行的一項研究,資料中心營運商的目標是在過去五年中將平均電力使用效率(PUE)比率從1.98降低到1.55,這是由於資料中心在規模方面的最新發展所致。資料中心和主機代管提供者。

北美佔最大市場佔有率

- 北美地區在綠色資料中心市場中佔據最大佔有率,許多服務供應商和軟體供應商引領市場。在北美,由於主機代管供應商和超大型資料中心營運商的大量投資,美國預計將主導市場,其次是加拿大。北美越來越多的設施正在開發為綠色資料中心,增加了對經濟高效的電力解決方案的需求。根據能源部的數據,資料中心約占美國所有用電量的 2%。

- 行動寬頻的擴展、5G 的出現、巨量資料分析和雲端處理的成長是推動該地區新資料中心基礎設施需求的關鍵因素。網路供應商正在快速部署 5G,以實現更好的創新。綠色資料中心供應商強調透過減少能源使用和提高效率來減少公司的碳排放。

- 北美擁有大量的資料中心和大量從硬體服務轉向軟體服務的公司,預計將對市場產生重大影響,成為資料中心轉型的有利市場。微軟、亞馬遜和 Facebook 已承諾將其現有資料中心轉變為綠色資料中心。

- 北美地區也對 IT、銀行、金融和保險 (BFSI)、零售和醫療保健行業的全球資料中心需求做出了重大貢獻。此外,考慮到資料中心的數量及其擴展,該地區的資料中心服務提供者處於有利的市場,從而鼓勵他們控制營運成本。

- 該地區各國政府正在採取積極措施來維護環境的永續性,並進一步加快資料中心的部署。全部區域不斷上升的智慧型手機和網路普及也有助於開拓該地區的綠色資料中心市場。

綠色資料中心產業概況

由於許多參與者在國內外營運,綠色資料中心市場競爭非常激烈。市場集中度中等。主要企業採取的主要策略是產品創新和併購。該市場的主要參與者包括思科技術公司、IBM公司、戴爾EMC公司和富士通有限公司。一些趨勢包括:

2022 年 11 月,大眾汽車的目標是到 2027 年使其資料中心業務實現淨碳中和。為了實現這一目標,該公司與綠山合作,擴大挪威營運商二氧化碳中性資料中心的運算能力。透過與綠山合作,大眾汽車將使用 100% 水力發電的可再生電力運作綠山的所有伺服器,以實現這一目標。同時,它也受到鄰近峽灣的自然冷卻。

2022年11月,SB Energy Global與Google合作,提供942MW綠色能源,以滿足Google德克薩斯州資料中心的消費量。根據這項合作關係,Google 在德克薩斯州的投資和對清潔能源的承諾將為 SB Energy 目前正在建造的四個總合容量為 1.2 吉瓦的太陽能發電工程提供 75% 的可再生能源。這些計劃預計於 2024 年中期運作。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場概況

- 市場概況

- 價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 資料儲存需求增加

- 電力領域佔據主要市場佔有率

- 市場限制因素

- 增加初始投資

第6章市場區隔

- 依服務

- 系統整合

- 監控服務

- 專業服務

- 其他服務

- 依解決方案

- 電源

- 伺服器

- 管理軟體

- 網路科技

- 冷卻

- 其他解決方案

- 依用戶

- 主機代管提供者

- 雲端服務供應商

- 公司

- 依行業分類

- 衛生保健

- 金融服務

- 政府機關

- 電訊/IT

- 其他行業

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- Fujitsu Ltd

- Cisco Technology Inc.

- HP Inc.

- Dell EMC Inc.

- Hitachi Ltd

- Schneider Electric SE

- IBM Corporation

- Eaton Corporation

- Vertiv Corporation

第8章投資分析

第9章 市場機會及未來趨勢

The Green Data Center Market size is estimated at USD 73.87 billion in 2024, and is expected to reach USD 155.09 billion by 2029, growing at a CAGR of 15.99% during the forecast period (2024-2029).

Key Highlights

- The global green data center market is expected from USD 57.63 billion in the current year and is projected to reach USD 120 billion over the next five years. Over the years, the concern regarding the growing percentage of energy consumption by data centers has alerted governments globally to regulate energy consumption, which is the primary factor for driving the green data center market. Also, the growth of data centers and colocation services are other factors driving green data centers.

- As cloud computing becomes more energy-efficient and increasingly relies on renewable sources, other industry verticals such as manufacturing, transportation, and buildings are expected to turn to green data centers to reduce emissions. For instance, a car manufacturer can outsource all of its in-house computing to zero-emission data centers.

- The rise in demand for data storage and storage space is a key factor driving the need for green data centers. According to Huawei, the global estimate of data center demand is expected to increase by 3 to 10 times over the forecast period. Green data center, which provides practical and eco-friendly solutions in terms of data storage and reduction in energy consumption, is expected to witness great demand, owing to the positive outlook of the data center storage needs and new constructions, which have been brought about due to the regulations and the anticipated rise in need to reduce the operational expenditure.

- Moreover, due to the rise of artificial intelligence (AI), machine learning (ML), big data, and the Internet of Things (IoT), the data centers' global electricity consumption will continue to increase, which is another driving factor for green data centers. According to International Energy Agency (IEA), data centers account for 1 to 1.5 percent of global electricity consumption. Hence, a strong focus on energy efficiency could drive the market.

- Despite the long-term savings and ROI, renewable energy data centers have a high initial investment cost. The initial investment in building an energy-efficient green data center is higher than the traditional one. To modify the existing infrastructure, companies need higher investments which is a restrain. However, companies are willing to invest in green data centers even though the cost of ownership is better and savings in the long term will pay back initial investments.

- COVID-19 is expected to drive the demand for green data centers owing to factors such as acceleration of cloud data center services, growing reliance on data center automation, driving up of hardware reuse as a primary challenge, greater remarketing of data center hardware. An increase in environmental awareness due to COVID-19 and this trend continues to grow post-pandemic considering the increase in organizations data traffic and big data analytics.

Green Data Center Market Trends

Power Segment to Hold a Significant Market Share

- Green data centers are built to maximize energy efficiency and lower environmental impact. The key demand is for greater energy efficiency because these data centers' power consumption and cooling problems are two of the most significant problems that enterprises confront globally and invest heavily in these. It is vital to control these operating costs to improve business operations and maintain market competitiveness.

- Power plays a significant role in investments in green data centers. Both low-power and effective solutions assist organizations in achieving their goals. Moving to variable-speed fans is one technique to reduce energy consumption in the data center. According to recent research, lowering the central processing unit (CPU) fan speed can reduce power consumption by 20%. As a result, businesses should employ variable-speed fans to cool data center equipment and reduce energy use.

- Datacenter energy costs have exceeded the overall investments in equipment rooms and auxiliary devices. However, results from recent research have shown that this trend is slowing down due to the effective green efficiency measures taken up in mature markets of the United States and Europe.

- By switching to economy mode, where servers run on utility power, server virtualization, where physical servers are used as pools, increases server utilization, consolidates space and equipment and reduces energy consumption because it decreases the number of physical servers needed within the data center. Due to the reduced number of servers being utilized, energy consumption decreases significantly due to a reduced need for electricity and cooling.

- With the increasing electricity usage, billings, and increasing emissions of CO2 from these data centers, the need for green data centers is set to increase, thereby driving the market forward. According to the survey conducted by the Uptime Institute, Data center operators aim to get their average power usage effectiveness (PUE) ratio reduced from 1.98 to 1.55 over the last five years owing to the development of the newest data centers from hyper-scale and colocation providers with a particular focus of energy efficiency.

North America Occupies the Largest Market Share

- The North American region holds the largest share in the green data center market, owing to the presence of many services and software providers driving the market forward. The United States is expected to dominate the market in North America, followed by Canada, with high investments by colocation providers and hyper-scale data center operators. The demand for cost-effective and efficient power solutions has increased, with more facilities being developed as green data centers in North America. According to the Department of Energy, data centers account for about 2% of all electricity use in the US.

- The expansion of mobile broadband, the emergence of 5G, growth in big data analytics, and cloud computing are the primary factors driving the demand for new data center infrastructures in this region. Network providers are working to ensure the implementation of 5G at a rapid pace for better innovation. Green data center providers have highlighted the reduction in the carbon footprint of corporations by reducing energy usage and increasing efficiency.

- North America, comprising a considerable amount of data centers and a large number of enterprises switching from hardware to software-based services, is expected to impact the market significantly and be a lucrative market for data center transformation. Microsoft, Amazon, and Facebook pledged to convert their existing data centers into green ones.

- The North American region also contributes substantially to the global data center requirements from the IT, banking, financial servcies, and insurance (BFSI), retail, and healthcare industries. In addition, data center service providers in the region are prompted to manage their operating costs, as the region is a lucrative market, considering the number of data centers and their expansions.

- The government across the region is taking active measures to maintain environmental sustainability, further accelerating data centers' deployment. The rising smartphone and internet penetration across this region lead to the development of the green data center market in the region.

Green Data Center Industry Overview

The green data center market is highly competitive, owing to many players in the market running their business domestically and internationally. The market is moderately concentrated. The key strategies adopted by the major players are product innovation and mergers and acquisitions. Some major players in the market are Cisco Technology Inc., IBM Corporation, Dell EMC Inc., and Fujitsu Ltd, among others. Some of the developments are:-

In November 2022, Volkswagen AG aims to make its data center operations net carbon neutral by 2027. To reach this goal, the company has expanded its computing capacities at the Norwegian operator of CO-neutral data centers by partnering with Green Mountain. The partnership with Green Mountain will allow Volkswagen to hit this target, with all servers at Green Mountain running on 100% renewable electricity generated by hydropower. At the same time, they are naturally cooled by the adjacent fjord.

In November 2022, SB Energy Global partnered with Google to supply 942 MW of Green Energy to match Google's texas Data center consumption. Under the partnership, Google's investment in Texas and commitment to clean energy will be supported by 75% of the renewable energy generated by four solar projects of SB Energy that have a combined capacity of 1.2 gigawatts and are currently under construction. These projects aim to be operational by the middle of 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGTHS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Data Storage

- 5.1.2 Power Segment to Hold a Significant Market Share

- 5.2 Market Restraints

- 5.2.1 Higher Initial Investments

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 System Integration

- 6.1.2 Monitoring Service

- 6.1.3 Professional Service

- 6.1.4 Other Services

- 6.2 By Solution

- 6.2.1 Power

- 6.2.2 Servers

- 6.2.3 Management Software

- 6.2.4 Networking Technologies

- 6.2.5 Cooling

- 6.2.6 Other Solutions

- 6.3 By User

- 6.3.1 Colocation Providers

- 6.3.2 Cloud Service Providers

- 6.3.3 Enterprises

- 6.4 By Industry Vertical

- 6.4.1 Healthcare

- 6.4.2 Financial Services

- 6.4.3 Government

- 6.4.4 Telecom and IT

- 6.4.5 Other Industry Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Technology Inc.

- 7.1.3 HP Inc.

- 7.1.4 Dell EMC Inc.

- 7.1.5 Hitachi Ltd

- 7.1.6 Schneider Electric SE

- 7.1.7 IBM Corporation

- 7.1.8 Eaton Corporation

- 7.1.9 Vertiv Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

綠色資料中心市場 - 2024 年至 2029 年預測

綠色資料中心市場 - 2024 年至 2029 年預測 綠色資料中心市場至2030年的預測:按組件、公司規模、最終用戶和地區的全球分析

綠色資料中心市場至2030年的預測:按組件、公司規模、最終用戶和地區的全球分析 2024 年碳中和資料中心全球市場報告

2024 年碳中和資料中心全球市場報告 2024-2032 年按組件、資料中心類型、垂直產業和地區分類的綠色資料中心市場報告

2024-2032 年按組件、資料中心類型、垂直產業和地區分類的綠色資料中心市場報告 碳中和資料中心市場報告:2030 年趨勢、預測和競爭分析

碳中和資料中心市場報告:2030 年趨勢、預測和競爭分析 碳中和資料中心市場:按產品類型、產業分類 - 2024-2030 年全球預測

碳中和資料中心市場:按產品類型、產業分類 - 2024-2030 年全球預測 綠色資料中心市場規模 - 按組件(解決方案、服務)、應用程式(託管、BFSI、能源、政府、醫療保健、製造、IT 和電信)、區域展望和全球預測,2024 年 - 2032 年

綠色資料中心市場規模 - 按組件(解決方案、服務)、應用程式(託管、BFSI、能源、政府、醫療保健、製造、IT 和電信)、區域展望和全球預測,2024 年 - 2032 年 綠色資料中心市場、份額、規模、趨勢、行業分析報告:按組件、按公司規模、按最終用途行業、按地區、按細分市場、預測,2023-2032年

綠色資料中心市場、份額、規模、趨勢、行業分析報告:按組件、按公司規模、按最終用途行業、按地區、按細分市場、預測,2023-2032年 碳中和資料中心市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按資料中心類型、碳中和解決方案、最終用戶、地區、競爭細分

碳中和資料中心市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按資料中心類型、碳中和解決方案、最終用戶、地區、競爭細分 綠色資料中心市場規模、佔有率、趨勢分析報告:按組成部分、按企業規模、按最終用途、按地區、細分市場趨勢,2023-2030 年

綠色資料中心市場規模、佔有率、趨勢分析報告:按組成部分、按企業規模、按最終用途、按地區、細分市場趨勢,2023-2030 年