|

市場調查報告書

商品編碼

1403106

低 VOC 塗料 -市場佔有率分析、產業趨勢/統計、2024-2029 年成長預測Low VOC Paint - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

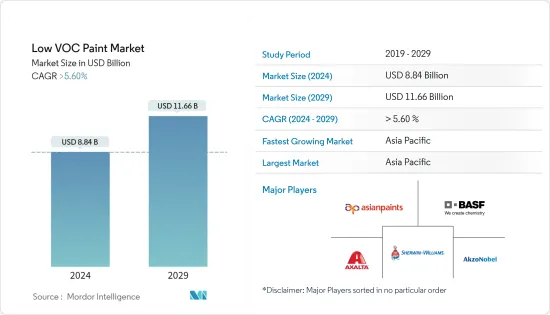

低VOC塗料市場規模預計到2024年為88.4億美元,預計到2029年將達到116.6億美元,在預測期內(2024-2029年)複合年成長率將超過5.60%,預計會成長。

COVID-19大流行影響了 2020 年和 2021 年的低 VOC 塗料市場,導致經濟和商業活動收縮,以及建築和工業產出下降。然而,市場近年來已經復甦,預計在此期間將會成長。

人們對傳統塗料相對於環保且使用安全的低揮發性有機化合物塗料的危害性的認知不斷提高,預計將在預測期內推動市場成長。

另一方面,與傳統塗料相比,低揮發性有機化合物塗料的成本較高,預計將阻礙市場成長。

在預測期內,增加生態建築的建設、轉向使用環境友善化學品以及回收低揮發性有機化合物塗料可能會為受調查的市場提供機會。

由於建築業低揮發性有機化合物塗料的大量消費量,亞太地區在全球市場佔據主導地位。

低VOC塗料市場趨勢

架構及裝飾業需求增加

- 裝飾塗料可以保護表面免受天氣影響,增強防水性,保護表面免受白蟻侵襲,增加表面的耐用性並賦予建築物美觀的吸引力。

- 此外,它還可以防止腐蝕、細菌、紫外線、黴菌、進水和藻類,延長結構的使用壽命。

- 對低揮發性有機化合物塗料的需求主要是由全球住宅和商業建築的成長所推動的,其中建築和裝飾行業佔大多數。

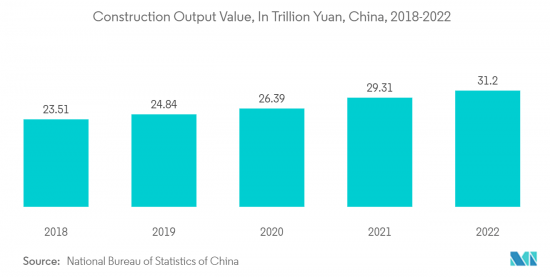

- 中國經濟成長的驅動力主要是住宅和商業設施的快速擴張。該國建築產值於2022年達到峰值,達到約4.64兆美元(31.2兆元)。因此,這些因素往往會增加預測期內的市場需求。

- 根據美國人口普查局的數據,商業竣工面積將反彈至景氣衰退的水平,並於 2022 年達到 1,150 億美元。在美國最受歡迎的商業開發類型是倉庫和私人辦公室。此外,2023年1-8月建築支出達12,847億美元,比2022年同期的12,334億美元成長4.2%。

- 此外,根據歐盟統計局的數據,由於歐盟復甦基金的新投資,歐洲建築業在 2022 年成長了 2.5%。 2022年的主要建設計劃將是非住宅(辦公室、醫院、飯店、學校、工業建築),佔總活動的31.3%。

- 預計此類建設活動將在預測期內增加對低揮發性有機化合物塗料等的需求。

亞太地區主導市場

- 亞太地區主導全球市場。隨著印度、中國、菲律賓、越南和印尼等國家增加對住宅和商業建築的投資,低揮發性有機化合物塗料市場預計在未來幾年將擴大。

- 低VOC塗料因其比普通塗料更環保而廣泛應用於建設產業。低揮發性有機化合物塗料用於多種應用,包括內外牆、天花板、裝飾、混凝土地板、金屬表面、家具和櫥櫃的塗漆。

- 在「十四五」規劃(2021-2025 會計年度)基礎設施投資的支持下,預計 2024 年至 2027 年建設產業的複合年成長率將達到 4.3%。此外,到 2030 年,政府為基礎建設計劃提供 6.8 兆元人民幣(1.1 兆美元)資金也將支持產業成長。 2022年,國家發展與改革委員會(NDRC)核准了109個固定資產投資計劃,價值1.5兆元(2,223億美元)。

- 據中國政府稱,新的信貸政策將於2023年1月宣布,旨在促進中國都市區的住宅銷售。為了鼓勵中國的住宅銷售,許多地方當局宣布了優惠券計劃。此外,2022年初,政府宣布提供290億美元的專案貸款,幫助建設公司完成停滯的計劃。

- 此外,印度政府計劃在未來七年內投資約 1.3 兆美元用於住宅建設。預計這將導致建造 6000 萬套新住宅。這些計劃正在推動建設產業低揮發性有機化合物塗料市場的發展。

- 此外,印尼政府還啟動了一項在印尼各地建造約100萬套住宅的計劃,並為此累計約10億美元。因此,它極大地促進了市場的成長。

- 低 VOC 塗料的 VOC 含量明顯低於傳統塗料,使其成為更環保、更健康的選擇。在汽車行業,低VOC塗料用於汽車外裝和內裝、汽車輪胎部件的塗裝以及受損汽車的重新塗裝。

- 根據中國工業協會統計,中國是全球最重要的汽車生產基地,預計2022年汽車產量將達到約2,702萬輛,比去年的2,612萬輛成長3.4%。因此,低VOC塗料在汽車領域有著龐大的市場。

- 因此,預計上述因素將在預測期內推動該地區對低揮發性有機化合物塗料的需求。

低VOC塗料產業概況

低揮發性有機化合物塗料市場因其性質而部分分散。主要參與企業(排名不分先後)包括 Akzo Nobel NV、Asian Paints、 BASF SE、Axalta Coating Systems, LLC 和 The Sherwin-Williams Company。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 人們越來越認知到傳統塗料的毒性

- 建築裝飾產業需求不斷成長

- 其他司機

- 抑制因素

- 成本比傳統塗料高

- 其他阻礙因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 類型

- 低揮發性有機化合物

- 無或零 VOC

- 自然的

- 複合型

- 水性的

- 溶劑型

- 粉末

- 目的

- 架構與裝飾

- 一般工業

- 汽車OEM

- 自動修理

- 海洋

- 耐久性消費品

- 其他應用(製藥、電子等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太地區

第6章競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Akzo Nobel NV

- American Formulating & Manufacturing

- Arkema

- Asian Paints

- AURO

- Axalta Coating Systems, LLC

- BASF SE

- Benjamin Moore & Co.

- Berger Paints India Limited

- BioShield Paint Company

- Cloverdale Paint Inc.

- Crown Trade

- Fine Paints of Europe

- Jotun

- Kalekim

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

第7章 市場機會及未來趨勢

- 加大生態建築建設力度

- 轉向環保化學品

The Low VOC Paint Market size is estimated at USD 8.84 billion in 2024, and is expected to reach USD 11.66 billion by 2029, growing at a CAGR of greater than 5.60% during the forecast period (2024-2029).

The COVID-19 pandemic impacted the low VOC paint market in 2020 and 2021, driven by reduced economic and commercial activities coupled with declines in construction and industrial output. But the market recovered in recent years and is anticipated to grow over the period.

The increasing awareness about the harmful effects of conventional paints, which is contrary to low VOC paints as they are eco-friendly and safe to use, is expected to drive the market's growth during the forecast period.

On the other hand, the high cost of low VOC paint compared to conventional paint is expected to hinder the market's growth.

The increasing construction of green buildings, shift toward eco-friendly chemicals, and recycling of low VOC paint will likely provide opportunities for the market studied during the forecast period.

Asia-Pacific dominated the global market due to the high consumption of low-VOC paints from the architectural industry.

Low VOC Paint Market Trends

Increasing Demand from Architectural and Decorative Segment

- Decorative paints help protect the surface from the impact of weather, make the surface waterproof, protect the surface from termite attacks, and increase surface durability, providing an aesthetic appeal to the building.

- In addition, they offer protection from corrosion, bacteria, UV radiation, fungus, water seepage, and algae and enhance the structure's life.

- The demand for Low VOC paints is dominated by the architectural and decorative industry, driven by the growing residential and commercial construction activities worldwide.

- China's growth is fueled mainly by rapid residential and commercial building expansion. The country's construction output peaked in 2022 at about USD 4.64 trillion (31.2 trillion yuan). As a result, these factors tend to increase the market demand during the forecast period.

- According to the US Census Bureau, the value of completed commercial construction has rebounded to pre-recession levels, reaching USD 115 billion in 2022. The most popular types of commercial development started in the United States were warehouses and private offices. Additionally, during the first eight months of 2023, construction spending amounted to USD 1,284.7 billion, which increased by 4.2% to USD 1,233.4 billion for the same period in 2022.

- Furthermore, according to Eurostat, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- Such construction activities are expected to increase the demand During the forecast period such as low-VOC paints.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region dominated the global market share. With growing investment in residential and commercial construction in countries such as India, China, the Philippines, Vietnam, and Indonesia, the market for low-VOC paints is expected to increase in the coming years.

- Low-VOC paints are widely used in the construction industry as it is eco-friendly compared to regular paints. Low VOC paints are used for various applications, including painting interior and exterior walls, ceilings, trim, concrete floors, metal surfaces, furniture, and cabinets.

- The construction industry is expected to record an average annual growth rate of 4.3% between 2024 and 2027, supported by investment in infrastructure as part of the 14th Five-Year Plan (FYP 2021-2025). Additionally, growth in the industry will also be aided by CNY 6.8 trillion (USD 1.1 trillion) of government funds for infrastructure construction projects by 2030. In 2022, the National Development and Reform Commission (NDRC) approved 109 fixed asset investment projects worth CNY 1.5 trillion (USD 222.3 billion).

- According to the Government of China, in January 2023, announced the new credit policy aims to drive urban housing sales in the country. To drive housing sales in China, many local authorities announced voucher schemes. Earlier in 2022, the government also announced a pledge of USD 29 billion in special loans, thereby allowing construction firms to finish stalled projects.

- Furthermore, the Indian government is likely to invest around USD 1.3 trillion in housing over the next seven years. It is expected to see the construction of 60 million new homes. Such projects are driving the low VOC paints market in the construction industry.

- Moreover, the Indonesian government has started a program to build about one million housing units across Indonesia, for which the government has allocated about USD 1 billion in the budget. Thus boosting the market growth significantly.

- Low VOC paints contain significantly less VOCs than traditional paints, making them a more environmentally friendly and healthier option. In the automotive industry, low VOC paints are used for painting exteriors and interior surfaces of the vehicle, automotive tire parts and refinishing damaged vehicles.

- According to the China Association of Automobile Manufacturers (CAAM), China has the most significant automotive production base in the world, with a total vehicle production of around 27.02 million units in 2022, registering an increase of 3.4 % compared to 26.12 million units produced last year. Thus providing a massive market for low-VOC paint in the automotive sector.

- Thus, the factors above are expected to drive the demand for low-VOC paints in the region during the forecast period.

Low VOC Paint Industry Overview

The low VOC paint market is partially fragmented in nature. The major players (not in any particular order) include Akzo Nobel N.V., Asian Paints, BASF SE, Axalta Coating Systems, LLC, and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Awareness about Harmful Effects of Conventional Paint

- 4.1.2 increasing Demand in Architectural and Decorative Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost in Comparison to Conventional Paint

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Low-VOC

- 5.1.2 No or Zero VOC

- 5.1.3 Natural

- 5.2 Formulation Type

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.3 Application

- 5.3.1 Architecture and Decorative

- 5.3.2 General Industrial

- 5.3.3 Automotive OEM

- 5.3.4 Automotive Refinish

- 5.3.5 Marine

- 5.3.6 Consumer Durables

- 5.3.7 Other Applications (Pharmaceuticals, Electronics, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 American Formulating & Manufacturing

- 6.4.3 Arkema

- 6.4.4 Asian Paints

- 6.4.5 AURO

- 6.4.6 Axalta Coating Systems, LLC

- 6.4.7 BASF SE

- 6.4.8 Benjamin Moore & Co.

- 6.4.9 Berger Paints India Limited

- 6.4.10 BioShield Paint Company

- 6.4.11 Cloverdale Paint Inc.

- 6.4.12 Crown Trade

- 6.4.13 Fine Paints of Europe

- 6.4.14 Jotun

- 6.4.15 Kalekim

- 6.4.16 Kansai Paint Co.,Ltd.

- 6.4.17 Nippon Paint Holdings Co., Ltd.

- 6.4.18 PPG Industries, Inc.

- 6.4.19 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Construction of Green Buildings

- 7.2 Shift toward Eco-friendly Chemicals