|

市場調查報告書

商品編碼

1432663

玉米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)Maize Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

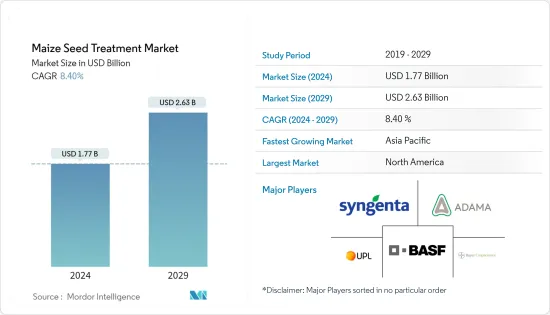

玉米種子處理市場規模預計到 2024 年為 17.7 億美元,預計到 2029 年將達到 26.3 億美元,在預測期內(2024-2029 年)複合年成長率為 8.40%。

主要亮點

- 玉米在全世界種植面積達 1.97 億公頃,是繼稻米和小麥之後的第三大重要穀物。這種作物普及採用市售混合種子,包括基改種子,已開發市場和新興市場的農民都在採用先進的耕作方法來種植玉米。

- 近三年來,玉米種植害蟲秋蠶大面積發生。適當的種子處理可以幫助保護幼苗免受這種致命害蟲的侵害。本公司也致力於研發針對秋蠶的產品。

玉米種子處理市場趨勢

種子匯率的提高導致商業領域的繁榮

商業玉米混合在世界各地越來越受歡迎。過去 20 年來,商業玉米混合一直在北美、歐洲和南美種植。然而,由於種子替代率的提高和混合動力採用率的提高,亞太和非洲等新興市場正在經歷顯著成長。 2018年,亞太地區種子兌換率達近80%。由於混合品種的採用增加以及先進混合品種(包括基因改造品種)的普及,玉米種子處理產品的商業應用市場正在蓬勃發展。這些產品以 B2B 形式出售給種子公司。越來越多的銷售玉米混合的種子公司也支持了玉米種子處理產品的商業應用市場。提高混合和種子匯率的下一個前沿是非洲,與這些相關的指標預計在預測期內將以強勁的速度成長。

北美引領全球市場

北美種植玉米的面積約 3500 萬公頃。它是該地區最重要的作物,廣泛用作糧食、牲畜飼料和飼料。該地區擴大採用基因改造和混合種子,使其成為世界上最大的地理區域。商業應用正在推動這個市場,公司推出了滿足農民作物保護需求的產品,同時考慮土壤和環境的永續性。在預測期內,該地區預計仍將是玉米種子加工市場最大的區域部分。

玉米種子加工產業概況

玉米種子加工市場高度整合,主要企業佔70%以上的市場佔有率。這些參與者的高市場佔有率歸因於其高度多元化的產品系列以及大量的收購和協議。此外,這些參與者也專注於研發、擴大產品系列、廣泛的地理分佈和積極的收購策略。該市場的主要企業包括BASF股份公司、先正達股份公司、安道麥農業解決方案公司、UPL 有限公司和拜耳作物科學公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 化學來源

- 合成

- 生物來源

- 產品類別

- 殺蟲劑

- 殺菌劑

- 其他產品類型

- 目的

- 農場層面

- 商業的

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲

- 北美洲

第6章 競爭形勢

- 最採用的策略

- 市場佔有率分析

- 公司簡介

- BASF SE

- Bayer Crop Science AG

- Syngenta AG

- Adama Agricultural Solutions

- UPL Limited

- Advanced Biological Marketing Inc.

- Corteva Agriscience

- Incotec Group BV

- Valent USA Corporation

第7章 市場機會及未來趨勢

The Maize Seed Treatment Market size is estimated at USD 1.77 billion in 2024, and is expected to reach USD 2.63 billion by 2029, growing at a CAGR of 8.40% during the forecast period (2024-2029).

Key Highlights

- Maize is grown over 197 million hectares worldwide and is the third important cereal crop, after rice and wheat. The crop has high degree of penetration in commercial hybrid seeds, including genetically modified seed, and farmers adopt advanced farming practices for maize cultivation in both developed and developing markets.

- In last three years, there was a widespread incidence of the pest fall amyworm in maize cultivation. Proper seed treatment can go a long way in protecting young plants against this deadly pest. Companies have also been engaging in R&D to develop products that target fall amyworm.

Maize Seed Treatment Market Trends

Increasing Seed Replacement Rate Leading to Boom in the Commercial Segment

Commercial maize hybrids are increasingly becoming popular across the world. Traditionally, North America, Europe, and South America have been cultivating commercial maize hybrids, since last two decades. However, increasing seed replacement rates and rising adoption of hybrids led to a remarkable growth of developing markets, such as Asia-Pacific and Africa. In 2018, seed replacement rates in Asia-Pacific stood at close to 80%. Increased adoption of hybrid varieties and penetration of advanced hybrids, including genetically modified varieties, have resulted in a booming market for commercial applications of maize seed treatment products. These products are being sold at a B2B level to seed companies. An increase in the number of seed companies selling maize hybrids has also supported the market for commercial applications of maize seed treatment products. The next frontier of hybridization and increased seed replacement rates is Africa, where the metrics related to these are expected to increase at a robust pace over the forecast period.

North America Leads the Global Market

Maize is grown over approximately 35 million hectares in North America. It is the most important grain crop in the region, with extensive application as grain, animal feed, and forage. Increased adoption of genetically modified and hybrid seeds in the region makes the geographical segment the largest among all the regions across the world. The market is driven by commercial applications, where companies are launching products that satisfy the crop protection needs of the farmer, while keeping sustainability of the soil and environment in mind. The region is expected to remain the largest geographical segment in the maize seed treatment market over the forecast period.

Maize Seed Treatment Industry Overview

The maize seed treatment market is highly consolidated, with the top global players occupying more than 70% of the market share. The greater market shares of these players can be attributed to highly diversified product portfolio and numerous acquisitions and agreements. Moreover, these players are focusing on R&D, expansion of product portfolio, wide geographical presence, and aggressive acquisition strategies. Some of the key players in the market include BASF SE, Syngenta AG, Adama Agricultural Solutions, UPL Limited, and Bayer Crop Science, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Chemical Origin

- 5.1.1 Synthetic

- 5.1.2 Biological

- 5.2 Product Type

- 5.2.1 Insecticides

- 5.2.2 Fungicides

- 5.2.3 Other Product Types

- 5.3 Application

- 5.3.1 Farm-level

- 5.3.2 Commercial

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Bayer Crop Science AG

- 6.3.3 Syngenta AG

- 6.3.4 Adama Agricultural Solutions

- 6.3.5 UPL Limited

- 6.3.6 Advanced Biological Marketing Inc.

- 6.3.7 Corteva Agriscience

- 6.3.8 Incotec Group BV

- 6.3.9 Valent USA Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年按類型、應用技術、作物類型、功能和地區分類的種子處理市場報告

2024-2032 年按類型、應用技術、作物類型、功能和地區分類的種子處理市場報告 大豆殺菌劑種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)

大豆殺菌劑種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029) 小麥種子處理:全球市場佔有率分析、產業趨勢、統計資料、成長預測(2024-2029)

小麥種子處理:全球市場佔有率分析、產業趨勢、統計資料、成長預測(2024-2029) 棉籽加工:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

棉籽加工:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029) 稻米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)

稻米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029) 2024 年種子處理全球市場報告

2024 年種子處理全球市場報告 種子處理市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、按應用、地區和競爭細分

種子處理市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、按應用、地區和競爭細分 全球種子處理市場

全球種子處理市場 2030 年種子處理市場預測:按作物類型、劑型、功能、用途和地區進行的全球分析

2030 年種子處理市場預測:按作物類型、劑型、功能、用途和地區進行的全球分析 種子處理的全球市場 - 市場規模,佔有率,成長分析:各類型,各作物,各功能 - 產業預測(2023年~2030年)

種子處理的全球市場 - 市場規模,佔有率,成長分析:各類型,各作物,各功能 - 產業預測(2023年~2030年)