|

市場調查報告書

商品編碼

1406910

電動汽車用固態電池:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029EV Solid-state Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

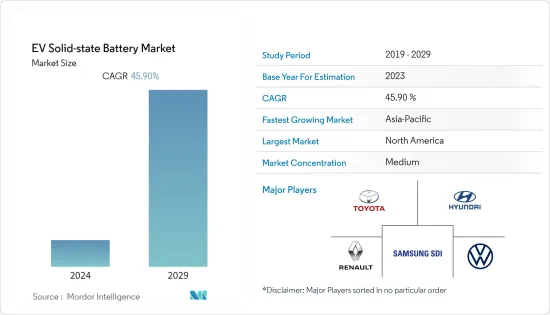

電動車固態電池市場規模為1.83億美元,預計五年內將達到12.14億美元,預測期內複合年成長率超過45.9%。

主要亮點

- COVID-19 大流行最初對市場產生了負面影響,由於生產單位關閉或封鎖,2020 年上半年銷售量減少。然而,到 2021 年,由於放鬆管制以及激勵和救助等政府舉措,市場得以重新獲得動力。此外,為了滿足不斷成長的市場需求,公司正在投資新設施。例如

- 2023年6月,優美科在比利時奧倫開設了世界上最大、最先進的固態電池材料原型實驗室之一。 600平方公尺的設施配備了最先進的設備和技術,支援整個固態電池研究鏈。

- 中期來看,對節能、高性能和低排放氣體車輛的需求不斷增加,有關車輛排放氣體的法律規章更加嚴格,以及電池成本下降是預測期內推動市場成長的主要因素。充當

- 目前,豐田汽車公司、特斯拉汽車公司、大眾工業公司、通用汽車集團、現代起亞汽車集團等公司佔據了電動車市場86%以上的佔有率。此外,這些公司是固態電池市場的早期進入者,預計將繼續佔領大部分市場。例如,2023年2月,日產宣布將於2025年啟動先導計畫,並於2028年推出首款採用固態電池的電動車。

- 亞太地區預計成長最快,其次是歐洲和北美。中國、印度、日本和韓國等國家的汽車工業正傾向於創新、技術以及先進電動車和電池的開發。對減少碳排放和開發更先進電池技術的需求不斷成長預計將在預測期內推動市場成長。例如

- 2023年6月,豐田計劃引入先進的固態電池和其他技術,以提高電動車的續航里程和性能並降低成本。

電動車固態電池的市場趨勢

擴大電動車銷量

- 世界各地越來越多的運動加速小型小客車電動車 (EV) 的普及,並逐步淘汰配備內燃機的傳統車輛。平均燃油價格的上漲反映出歐洲的新電動車註冊比例高於其他地區。因此,由於燃油價格上漲,電動車的大規模採用預計將在全球電動動力傳動系統市場激增。

- 歐洲是電動動力傳動系統的重要市場,佔汽車生產的重要佔有率。芬蘭、挪威、瑞典和荷蘭等國家的電動車普及是全世界最高的。 2022年中國成為全球最大的插電式電動車銷售市場,同年銷量達近6.2輛。中歐和西歐則位居第二,當年售出約 2.7 輛電動車。

- 2022年純電動小客車年銷量將突破700萬輛。預計到2026年終,它將佔所有汽車銷量的15%左右。因此,電動車登記數量的增加帶動了電動車動力傳動系統總成產量的增加。

- 電動車因其較低的初期成本和較低的營運成本而對廣大客戶,尤其是低收入者俱有吸引力。目前,交通成本佔家庭總支出的很大一部分,低收入家庭將從這種更實惠、更方便的選擇中受益最多。

- 電動車需求的增加和固態電池的優勢預計將在預測期內推動需求。

亞太地區有潛力呈現顯著成長

亞太市場由中國、印度和日本等國家主導。亞太地區仍是一個不成熟的市場,但潛力巨大。

中國政府正在鼓勵引進電動車。該國已經計劃逐步淘汰為包括卡車在內的當前一代商用車輛提供動力的柴油。該計劃是到2050年完全禁止柴油和汽油汽車。因此,新興市場是最大的成長市場之一,並有可能推動中國電動車市場以及新商用車的開拓和訂單。

印度的電動車市場正處於成長階段。塔塔、馬恆達、馬魯蒂鈴木和現代汽車等印度汽車巨頭正在努力為印度的電動車提供實惠的選擇。此外,政府還提供補貼和計劃,以在印度引入電動車。

政府制定了各種減少國內污染的策略。例如,透過 FAME 和 FAME II 政策,該國正在透過向客戶提供獎勵以及為投資者和製造商建立電動汽車工廠提供有吸引力的選擇來促進綠色汽車的快速普及。

此外,塔塔 Nexon 等價格實惠的電動車也吸引著消費者。這款最近推出的中型 SUV 是印度最暢銷的汽車之一,一年內售出 4,000 多輛。同樣,名爵以合理的價格銷售了3000輛電動車,這是推動印度電動車銷售成長的另一個因素。

日本政府也提出了2050年實現二氧化碳零排放的「碳中和」目標。儘管受到 COVID-19 大流行的影響,博世仍推出了 Huis Ten 純電動公車,以實現其環境保護目標。此外,近年來,對插電式混合動力汽車、燃料電池電動車和純電動車等替代動力車的需求顯著增加。全國各地的汽車製造商正在測試電動卡車的潛力,而電動卡車有潛力幫助人們擺脫內燃機汽車,從而保護環境。

這樣的案例可以支持電動車市場的成長軌跡,進而推動未來十年對固態電池的需求。

電動車固態電池產業概況

電動車固態電池市場預計將由豐田汽車公司、雷諾集團、Stellantis NV、通用汽車、三菱汽車、大眾汽車、福特汽車、現代集團、三星SDI、Panasonic和LG化學主導。公司正在關注這一點。

2022年2月,東風E70在國內交付50輛電動計程車。該車輛被標記為第一款商業性固態電池車輛。

2022年1月,日產、雷諾和三菱結成策略聯盟,以加強在電動車市場的地位。在此次合作中,三菱將加強行銷,日產將開發固態電池技術,雷諾將開發車輛的電氣和電子架構。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 電動車銷量的成長預計將推動市場

- 市場抑制因素

- 電動車固態電池的高成本可能會阻礙市場成長

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 車型

- 小客車

- 商用車

- 推進力

- 插電式混合電動車

- 混合車

- 電池電動車

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Toyota Motor Corporation

- Hyundai Motor Company

- Renault Group

- Samsung SDI Co. Ltd

- Volkswagen AG

- Mitsubishi Motors

- Ford Motor Company

- General Motors

- Stellantis NV

- LG Chem Ltd

第7章 市場機會及未來趨勢

The EV solid-state battery market was valued at USD 183 million, and it is expected to reach USD 1,214 million over the period of five years, registering a CAGR of over 45.9% during the forecast period.

Key Highlights

- The COVID-19 pandemic initially had a negative impact on the market as the shutdown of manufacturing units, and lockdowns resulted in a decrease in sales during the first half of 2020. However, eased restrictions coupled with notable initiatives of the government in the form of incentives and relief packages helped the market regain momentum by 2021. Further, the companies are also focusing on investing in new facilities due to the increasing demand in the market. For instance,

- In June 2023, In Olen, Belgium, Umicore opened one of the world's largest and most advanced solid-state battery material prototyping labs. The 600-square-meter facility, outfitted with cutting-edge installations and technology, supports the entire chain of solid-state battery research.

- Over the medium term, increased demand for fuel-efficient, high-performance, and low-emission vehicles, increasingly strict laws and regulations on vehicle emissions, declining battery costs, etc., are expected to act as primary factors driving the market growth over the forecast period.

- As of now, the electric vehicle market is dominated by Toyota Motor Corporation, Tesla Motors Inc., Volkswagen AG, Honda Motor Company Ltd., General Motors Group, Hyundai Kia Automotive Group, etc., with more than 86% of the market share. Further, these companies are expected to be early movers in the solid-state battery market and are likely to remain to hold the larger chunk of the market. For instance, In February 2023, Nissan announced that the company is going to start a pilot project in 2025 to bring its first electric car with a solid-state battery by 2028.

- The Asia-Pacific region is expected to witness the fastest growth, followed by Europe and North America. The automotive industry in countries such as China, India, Japan, and South Korea is inclined toward innovation, technology, and the development of advanced electric vehicles and batteries. The increasing demand for reducing carbon emissions and developing more advanced battery technology is expected to propel the market growth during the forecast period. For instance,

- In June 2023, To improve the range and performance and to cut costs of its electric vehicles, Toyota is planning to introduce high-performance, solid-state batteries and other technologies.

EV Solid-state Battery Market Trends

Increasing Sales of Electric Vehicle

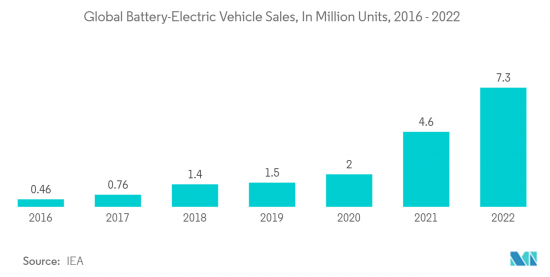

- The movement to accelerate the adoption of light-duty passenger electric cars (EVs) and phase out traditional vehicles with internal combustion engines is gaining traction around the world. The increase in average fuel prices reflects the fact that Europe has a higher share of new electric car registrations than other parts of the world. Hence, mass adoption of electric vehicles, owing to rising fuel prices, is expected to proliferate globally in the electric powertrain market.

- Europe is a crucial market for electric powertrains and holds a substantial share of automotive production. Countries such as Finland, Norway, Sweden, and the Netherlands have the highest adoption rate of EVs in the world. With nearly 6.2 sales that year, China was the world's largest market for plug-in electric car sales in 2022. Central and Western Europe came in second, with approximately 2.7 electric vehicles sold that year.

- The annual sales volume of battery-electric passenger cars will cross the 7 million mark in 2022. It is expected to account for about 15% of the overall vehicle sales by the end of 2026. Hence, the increase in electric car registrations resulted in an increased production of electric vehicle powertrains.

- Lower operating expenses, along with lower up-front expenditures, make electric vehicles more appealing to a wider range of customers, particularly low-income customers. Currently, transportation expenditures account for a significant portion of overall household expenses, and low-income households will gain the most from this more reasonable, accessible option.

- The increasing demand for electric vehicles and the benefits of solid-state batteries are expected to drive the demand over the forecast period.

Asia-Pacific May Illustrate Enormous Growth

The Asia-Pacific market is led by countries like China, India, and Japan. Asia-Pacific is still an immature market with immense hidden potential.

The government of China is encouraging people to adopt electric vehicles. The country has already made plans to phase out diesel fuel, which runs the current generation of commercial vehicles, such as trucks. The country is planning to completely ban diesel and petrol vehicles by 2050. Therefore, the country, being one of the largest growing electric markets, along with new developments and orders for commercial vehicles, is likely to drive the Chinese electric vehicle market.

The electric vehicle market in India is in the growing stage. Automobile giants in India, including TATA, Mahindra, Maruti Suzuki, and Hyundai Motors, are taking initiatives to provide affordable options for electric vehicles in India. Moreover, the government is providing subsidies and schemes to adopt electric mobility in India.

The government has been formulating various strategies to reduce pollution in the country. For instance, with its FAME and FAME II policies, the country has been providing incentives to customers and attractive options for investors and manufacturers to set up EV plants to propel the nation toward the faster adoption of green vehicles.

Moreover, electric cars at reasonable prices are attracting consumers, such as Tata Nexon. The recently launched mid-size SUV is one of the hot-selling cars in India, and more than 4,000 units have been sold within the year. Similarly, the 3,000 units sold by MG electric cars at a reasonable price is one of the factors increasing the sales of electric cars in India.

The Japanese government also proposed a 'carbon neutral' goal of achieving zero carbon emissions by 2050. To achieve its environmental protection goals, Huis Ten Bosch introduced pure electric buses, despite disruptions of the COVID-19 pandemic. Moreover, the demand for alternatively powered vehicles, such as plug-in hybrids, fuel cell electric vehicles, and battery electric vehicles, has increased significantly over the past few years. Vehicle manufacturers across the country are testing the possibilities of electric trucks, which may support the government's move from IC engine vehicles, thereby protecting the environment.

Such instances may aid the growth trajectory of the electric vehicle market, which, in turn, may propel the demand for solid-state batteries over the coming decade.

EV Solid-state Battery Industry Overview

The EV solid-state battery market is expected to be dominated by Toyota Motor Corporation, Renault Group, Stellantis NV, General Motors, Mitsubishi Motors, Volkswagen AG, Ford Motor Company, Hyundai Group, Samsung SDI, Panasonic, and LG Chem. The companies are focused.

In February 2022, in China, Dongfeng E70 delivered 50 electric sedans for taxis. This vehicle is marked as the first commercially available solid-state battery vehicle.

In January 2022, Nissan, Renault, and Mitsubishi came under a strategic alliance to strengthen their position in the electric vehicle market. In this alliance, Mitsubishi will reinforce marketing, Nissan will develop solid-state battery technology, and Renault will develop electrical and electronics architecture for vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Sales of Electric Vehicle is Expected to Drive the Market

- 4.2 Market Restraints

- 4.2.1 High Cost of EV Solid-State Battery May Hamper the Growth of the Market

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 Propulsion

- 5.2.1 Plug-in Hybrid Electric Vehicle

- 5.2.2 Hybrid Electric Vehicle

- 5.2.3 Battery Electric Vehicle

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Toyota Motor Corporation

- 6.2.2 Hyundai Motor Company

- 6.2.3 Renault Group

- 6.2.4 Samsung SDI Co. Ltd

- 6.2.5 Volkswagen AG

- 6.2.6 Mitsubishi Motors

- 6.2.7 Ford Motor Company

- 6.2.8 General Motors

- 6.2.9 Stellantis NV

- 6.2.10 LG Chem Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

電動車固態電池的全球市場:依車型、電池能量密度、推進力、地區、機會、預測,2017-2031

電動車固態電池的全球市場:依車型、電池能量密度、推進力、地區、機會、預測,2017-2031 全球固態電池市場規模、佔有率、成長分析、依產品(平板電腦、筆記型電腦)、最終用戶(遊戲機、筆記型電腦)- 2024-2031 年產業預測

全球固態電池市場規模、佔有率、成長分析、依產品(平板電腦、筆記型電腦)、最終用戶(遊戲機、筆記型電腦)- 2024-2031 年產業預測 2024年全固態電池全球市場報告

2024年全固態電池全球市場報告 全球固態電池市場:到2032年的機會與策略

全球固態電池市場:到2032年的機會與策略 固態電池市場 - 全球和區域分析:按電解質類型、按電池類型、按容量、按用途、按地區 - 分析和預測 (2023-2032)

固態電池市場 - 全球和區域分析:按電解質類型、按電池類型、按容量、按用途、按地區 - 分析和預測 (2023-2032) 全球固體電池市場(~2030):型號(單芯、多芯)、容量(20mAh以下、20-500mAh、500mAh以上)、電池類型(一次、二次)、用途(CE產品、電動車、醫療設備)/地區

全球固體電池市場(~2030):型號(單芯、多芯)、容量(20mAh以下、20-500mAh、500mAh以上)、電池類型(一次、二次)、用途(CE產品、電動車、醫療設備)/地區 固態電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測。按類型、容量、應用、地區和競爭細分

固態電池市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測。按類型、容量、應用、地區和競爭細分 全固體電池市場報告:至2030年的趨勢、預測與競爭分析

全固體電池市場報告:至2030年的趨勢、預測與競爭分析 2023-2027年全球固態電池市場

2023-2027年全球固態電池市場 新能源汽車固態電池發展分析

新能源汽車固態電池發展分析