|

市場調查報告書

商品編碼

1435541

螺紋鋼:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Steel Rebar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

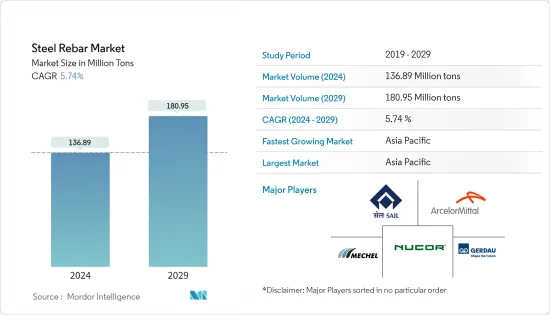

2024年螺紋鋼市場規模預估為1,3689萬噸,預估至2029年將達1,8095萬噸,預測期內(2024-2029年)複合年成長率為5.74%。

由於新型冠狀病毒感染疾病(COVID-19)的爆發,世界各地實施了全國範圍的封鎖,製造活動和供應鏈中斷、生產停頓和勞動力短缺對螺紋鋼市場產生了負面影響。然而,隨著所研究市場的需求復甦,該產業在 2021 年出現復甦。

主要亮點

- 短期內,基礎設施開發計劃和建設活動投資的增加是推動所研究市場成長的一些因素。

- 相反,較便宜的螺紋鋼替代品的可用性可能會阻礙所研究市場的成長。

- 然而,新興國家基礎設施活動的增加預計將在預測期內提供許多機會。

- 由於該地區各國基礎設施擴建新計劃建設的投資增加,亞太地區主導了市場。

螺紋鋼市場趨勢

非住宅領域的需求不斷成長

- 隨著都市化進程的進步,鋼筋廣泛應用於石油天然氣工業、基礎建設、商業建築、企業建築等非住宅領域。

- 美國擁有龐大的建築業,截至 2023 年 1 月僱用人數超過 990 萬人。美國建築業在商業和非住宅建築中發揮重要作用,對國家經濟做出了重大貢獻。由於美國住宅建設活動的增加,預計國內螺紋鋼消費量將增加。

- 根據美國人口普查局的數據,2022 年 12 月美國新建設產值達到 17,929 億美元。 2023年3月,非住宅領域價值9,971.4億美元,較全球成長18.8%。去年同期。

- 此外,根據美國人口普查局的數據,2022 年 6 月私人和公共建築非住宅支出為 4,926.8 億美元,比 2021 年 6 月的 4,842.6 億美元成長 1.74%。因此,該國私人和公共非住宅建築支出的增加預計將為螺紋鋼市場創造上行需求。

- 另外,紅牛美國還計劃在北卡羅來納州康科德市建設佔地 200 萬平方英尺的加工和分銷設施,進行各種建設和商業計劃,價值 7.4 億美元。酪農合作社 Dairgold 位於華盛頓州帕斯科港的加工設施佔地 40 萬平方英尺,價值 5 億美元(計畫於 2023 年竣工)。 Biotics Research Corporation 將在德克薩斯州羅森伯格建造一座 88,000 平方英尺的倉庫、實驗室和辦公設施,價值 900 萬美元(計劃於 2023 年竣工)。

- 此外,沙烏地阿拉伯正在進行許多商業計劃,這可能會導致該國建造更多商業建築。耗資 5000 億美元的未來特大城市 Neom計劃(紅海計劃一期)計劃於2025 年完工,將包括五個島嶼、兩個內陸度假村、Qudiya 娛樂城、超豪華健康目的地Amara 和14 個擁有3,000 間客房的飯店讓·努維爾 (Jean Nouvel) 位於埃爾奧拉 (AlUla) 的夏蘭度假村 (Sharan Resort) 對面設有豪華和超豪華酒店。

- 預計印度將繼續成為G20經濟體成長最快的國家。印度政府宣布三年(2023-2025年)基礎建設投資目標為3,765億美元,其中1,205億美元用於發展27個產業叢集,753億美元用於公路、鐵路和港口互聯互通計劃。

- 所有上述因素預計將在預測期內推動鋼筋的需求。

亞太地區主導市場

- 亞太地區預計將主導全球市場佔有率。由於印度、中國、菲律賓、越南和印尼等國家住宅和商業建築投資的增加,螺紋鋼市場預計在未來幾年將成長。

- 中國龐大的建築業對鋼筋的使用產生了巨大的需求。此外,中國近年來一直是世界基礎設施的主要投資者之一,並做出了重要貢獻。例如,根據中國國家統計局(NBS)的數據,2022年中國建築業產值將達到27.63兆元(41.08581億美元),比2021年成長6.6%。

- 此外,由於政府的支持和舉措,印度的住宅產業正在崛起,需求進一步增加。據印度品牌股權基金會(IBEF)稱,住房與城市發展部(MoHUA)已在2022-2023年預算中撥出98億日元用於建造住宅,並設立基金以完成停滯的計劃,並撥款5000萬美元。

- 此外,印尼預計在第二季開始為數千名公務員建造價值27億美元的公寓,遷往婆羅洲島的新首都。此外,印尼政府計劃透過外國投資籌集80%的資金。因此,預計這將導致該國住宅建築對鋼筋的消耗產生上升需求。

- 印尼計劃在北加里曼丹省(卡盧特勒)卡延河開發價值10億美元的900兆瓦水力發電發電工程。該計劃目前處於EPC階段,計劃於2022年開工。計劃計劃於2025年竣工後投入運作。

- 隨著2025年大阪世博會的舉辦,日本的建設產業可望蓬勃發展。此外,ESR Cayman、大阪 OS Cosmo Square資料中心計劃是日本最大的建設計劃,價值 20 億美元,將於 2022 年第四季開始施工。 ESR 開曼、OS Cosmo Square資料中心、大阪計劃於 2021 年第二季宣布。大阪市大壩建設計畫於 2026 年第一季完成。第二大計劃愛知縣的Shitara水壩開發項目,計劃價值5.7億美元,於2022年第四季開始開發。日本國土交通省的愛知縣設樂大壩開發計劃位於日本,於 2022 年第三季宣布,預計竣工日期為 2034 年第四季。

- 因此,在預測期內,各國需求的成長預計將推動該地區的市場研究。

鋼筋產業概況

螺紋鋼市場本質上是細分的。該市場的主要企業(排名不分先後)包括ArcelorMittal、Gerdau S/A、Nucor Corporation、Mechel、SAIL等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 亞太地區建築業快速成長

- 商業建築增加

- 其他司機

- 抑制因素

- 鋼筋替代品的可用性

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模(基於數量))

- 類型

- 形變

- 溫和的

- 最終用戶產業

- 住宅

- 非住宅

- 商業的

- 基礎設施

- 設施

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- ArcelorMittal

- Celsa Steel(UK)Ltd

- Contractors Materials Company(CMC)

- Daido Steel Co., Ltd.

- Essar

- Gerdau S/A

- HYUNDAI STEEL

- JFE Steel Corporation

- Jiangsu Shagang Group

- KOBE STEEL, LTD.

- Mechel

- NIPPON STEEL CORPORATION

- Nucor Corporation

- SAIL

- Sohar Steel Group

- Tata Steel

第7章 市場機會及未來趨勢

- 新興國家基礎建設活動活性化導致需求增加

- 其他機會

The Steel Rebar Market size is estimated at 136.89 Million tons in 2024, and is expected to reach 180.95 Million tons by 2029, growing at a CAGR of 5.74% during the forecast period (2024-2029).

Due to the COVID-19 outbreak, nationwide lockdowns around the globe, disruption in manufacturing activities and supply chains, production halts, and labor unavailability have negatively impacted the steel rebar market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, rising investments in infrastructure development projects and construction activities are some of the factors driving the growth of the market studied.

- On the flip side, the availability of cheap substitutes for steel rebar is likely to hinder the growth of the market studied.

- However, rising infrastructural activities in developing countries are anticipated to provide numerous opportunities over the forecast period.

- Asia-Pacific region dominated the market, owing to the increasing investments in constructing new projects for infrastructural expansion across various countries in the region.

Steel Rebar Market Trends

Growing Demand from the Non-Residential Sector

- With increasing urbanization, steel rebars are experiencing extensive utilization from the non-residential segment, like the oil and gas industry, infrastructure, commercial construction, corporate buildings, etc.

- The United States boasts a colossal construction sector that employs over 9.9 million employees as of January 2023. Playing a prominent role in commercial and non-residential construction, the United States construction sector exhibits a significant contribution to the country's economy. Due to increasing non-residential construction activities in the United States the consumption of steel rebar in the country is expected to increase.

- According to the United States Census Bureau, the value of new construction output in the United States amounted to USD 1,792.9 billion in December 2022. The non-residential sector accounted for USD 997.14 billion in March 2023, registering a growth of 18.8% compared to the same period the previous year.

- Moreover, according to the United States Census Bureau, the private and public construction nonresidential spending in June 2022 was 492.68 billion, which showed an increase of 1.74% compared to June 2021, which amounted to USD 484.26 billion. Therefore, increasing in the spending on private and public non-residential constructions in the country is expected to create an upside demand for steel rebar market.

- Apart from that, there are various construction commercial projects scheduled in the United States Red Bull North America's USD 740 million worth 2 million-square-foot processing and distribution facility in Concord, North Carolina; Dairy cooperative DairgoldUSD 500 million worth 400,000-square-foot processing facility in Port of Pasco, Washington (completion scheduled for 2023); Biotics Research Corporation USD 9 million worth 88,000-square-foot warehouse, laboratory, and office facility in Rosenberg, Texas (completion scheduled for 2023).

- Furthermore, Saudi Arabia is working on a lot of commercial projects, which will likely lead to more commercial buildinings in the country.The USD 500 billion futuristic mega-city "Neom" project, the Red Sea Project - Phase 1, which is expected to be completed by 2025 and has 14 luxury and hyper-luxury hotels with 3,000 rooms spread across five islands and two inland resorts, Qiddiya Entertainment City, Amaala - the uber-luxury wellness tourism destination, and Jean Nouvel's Sharaan resort in Al-Ula.

- India is anticipated to remain the fastest-growing G20 economy. The Indian government announced a target of USD 376.5 billion in infrastructure investment over three years (2023-2025), including USD 120.5 billion for developing 27 industrial clusters and USD 75.3 billion for road, railway, and port connectivity projects.

- All the above-mentioned factors are expected to propel the demand for steel rebar during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is anticipated to dominate the global market share. With growing investments in residential and commercial construction in the countries, such as India, China, the Philippines, Vietnam, and Indonesia, the market for steel rebars is expected to grow in the coming years.

- China's massive construction sector has generated significant demand for the use of steel rebars. Moreover, China is a huge contributor, as it has been one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to 27.63 trillion yuan (USD 4108.581 billion), an increase of 6.6% compared with 2021.

- Moreover, the residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects.

- Furthermore, Indonesia expects to begin construction in the second quarter on apartments worth USD 2.7 billion for thousands of civil servants due to move to its new capital city on Borneo island. Moreover, tndonesian government intends to finance it for 80% through foreign investments. Therefore, this is expected to create an upside demand for the consumption of steel rebars from the contry's residential construction.

- Indonesia plans to develop a USD 1 billion worth 900 MW hydropower project in Kayan River in the North Kalimantan (Kaltara) province. The project stands at the EPC stage, with a startup date planned for 2022. The project is expected to be commissioned after the completion of the construction in 2025.

- The Japanese construction industry is expected to be booming as the country will host the World Expo in 2025 in Osaka, Japan. Furthermore, the ESR Cayman, OS Cosmosquare Data Centre, Osaka project, valued at USD 2,000 million, was Japan's largest building project, on which construction started in Q4 2022. The ESR Cayman, OS Cosmosquare Data Centre, Osaka project was announced in Q2 2021 in Osaka (City), Japan, with a completion date of Q1 2026. The second-largest project, the MLIT Japan, Shitara Dam Development, Aichi, with a project value of USD 570 million, began development in Q4 2022. The MLIT Japan, Shitara Dam Development, Aichi project is located in Japan and was announced in Q3 2022, with a completion date of Q4 2034.

- Thus, rising demand from various countries is expected to drive the market studied in the region during the forecast period.

Steel Rebar Industry Overview

The Steel Rebar market is partially fragmented in nature. The major players in this market (not in a particular order) include ArcelorMittal, Gerdau S/A, Nucor Corporation, Mechel, and SAIL, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Growing Construction Industry in Asia-Pacific Region

- 4.1.2 Increasing Commercial Construction

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes for Steel Rebar

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Deformed

- 5.1.2 Mild

- 5.2 End-user Industry

- 5.2.1 Residential

- 5.2.2 Non-Residential

- 5.2.2.1 Commercial

- 5.2.2.2 Infrastructure

- 5.2.2.3 Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 Celsa Steel (UK) Ltd

- 6.4.3 Contractors Materials Company (CMC)

- 6.4.4 Daido Steel Co., Ltd.

- 6.4.5 Essar

- 6.4.6 Gerdau S/A

- 6.4.7 HYUNDAI STEEL

- 6.4.8 JFE Steel Corporation

- 6.4.9 Jiangsu Shagang Group

- 6.4.10 KOBE STEEL, LTD.

- 6.4.11 Mechel

- 6.4.12 NIPPON STEEL CORPORATION

- 6.4.13 Nucor Corporation

- 6.4.14 SAIL

- 6.4.15 Sohar Steel Group

- 6.4.16 Tata Steel

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand Due to Rising Infrastructural Activities in Developing Countries

- 7.2 Other Opportunities

2024-2028年全球鋼筋市場

2024-2028年全球鋼筋市場 冷軋鋼捲市場:依硬度、最終用戶產業:2023-2032 年全球機會分析與產業預測

冷軋鋼捲市場:依硬度、最終用戶產業:2023-2032 年全球機會分析與產業預測 2024 年世界螺紋鋼市場報告

2024 年世界螺紋鋼市場報告 美國螺紋鋼市場規模和預測、區域佔有率、趨勢和成長機會分析報告範圍:按類型、塗層類型和應用

美國螺紋鋼市場規模和預測、區域佔有率、趨勢和成長機會分析報告範圍:按類型、塗層類型和應用 圓鋼市場:依材料類型、依直徑範圍、依製造程序、依最終用途行業、依應用、依配銷通路、依地區

圓鋼市場:依材料類型、依直徑範圍、依製造程序、依最終用途行業、依應用、依配銷通路、依地區 全球鋼筋市場,預測(截至 2030 年)

全球鋼筋市場,預測(截至 2030 年) 鋼筋市場報告:2030 年趨勢、預測與競爭分析

鋼筋市場報告:2030 年趨勢、預測與競爭分析 螺紋鋼市場(類型:碳鋼螺紋鋼、不銹鋼螺紋鋼、鍍鋅螺紋鋼、環氧塗層螺紋鋼等;鋼筋類型:變形和輕度)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

螺紋鋼市場(類型:碳鋼螺紋鋼、不銹鋼螺紋鋼、鍍鋅螺紋鋼、環氧塗層螺紋鋼等;鋼筋類型:變形和輕度)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 2023-2027年熱處理(TMT)鋼筋的全球市場

2023-2027年熱處理(TMT)鋼筋的全球市場 冷軋鋼捲市場:各產品類型,各終端用戶,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測

冷軋鋼捲市場:各產品類型,各終端用戶,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測