|

市場調查報告書

商品編碼

1404106

發酵化學品-市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Fermentation Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

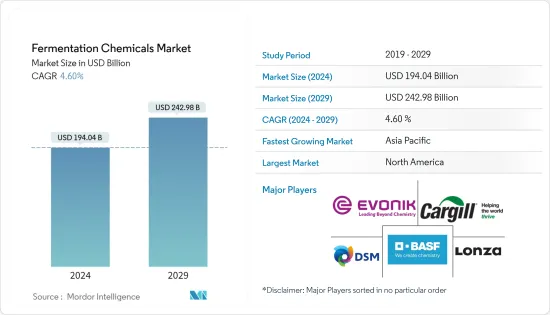

發酵化學品市場規模預計到2024年為1,940.4億美元,預計到2029年將達到2,429.8億美元,在預測期內(2024-2029年)複合年成長率為4.60%。

COVID-19大流行對發酵化學品市場產生了負面影響。然而,市場在2021年顯著復甦。

主要亮點

- 短期來看,甲醇和乙醇產業需求的增加以及製藥業需求的增加是推動所研究市場成長的關鍵因素。

- 然而,由於製造流程複雜性導致的高成本可能會限制市場成長。

- 然而,隨著生態化學機會的增加,全球市場很快就會出現利潤豐厚的成長機會。

- 北美地區主導發酵化學品市場,美國、加拿大和墨西哥等國家的消費量最大。

發酵化學品市場趨勢

食品和飲料產業主導市場

- 發酵通常意味著需要微生物作用。發酵產生酒精飲料,如葡萄酒、啤酒和蘋果酒。發酵也用於乳製品生產和麵包發酵。

- 食品和飲料行業對發酵化學品的需求量很大,因為它們是人類用來生產更安全、更穩定和更好的食品的最古老的生物技術。

- 在亞太地區,由於生活方式的改變、人們的可支配收入、速食以及對食品的偏好,對加工食品的需求正在成長。消費者更喜歡已調理食品的準備時間要少得多,而且新鮮,而且包裝美觀、堅固。

- 此外,預計中國仍將是亞洲最大的食品市場,印度和東南亞的食品支出成長最為強勁。

- 由於人們對包裝食品的過度依賴以及食品加工公司的強大立足點,北美食品加工市場十分強勁。百事可樂、泰森食品和雀巢是該地區主要的食品加工公司。

- 德國是歐洲最大的食品和飲料市場,擁有超過 8,300 萬消費者,是世界上最富有的消費者。 2023年,德國食品市場預計銷售額將達2,455億美元。預計2023年至2027年該市場將以每年3.64%的速度成長。

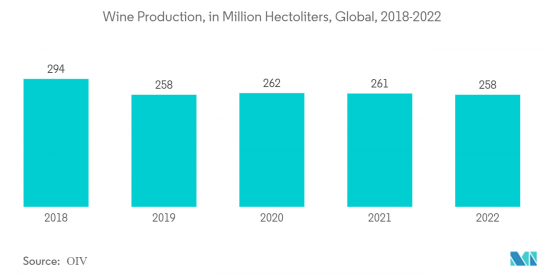

- 根據 OIV(國際葡萄與葡萄酒組織)的數據,2022 年全球葡萄酒產量約為 2.58 億百公升。

- 此外,2022年,義大利是全球最大的葡萄酒生產國,也是葡萄酒出口最多的國家,出口量為2,190萬公升。最大的出口國是另外兩個主要葡萄酒生產國。法國出口量為 1,400 萬百升,西班牙出口量為 2,120 萬公升。

- 這些因素可能會支持食品和飲料領域的研究市場需求。

北美市場佔據主導地位

- 北美目前在全球發酵化學品市場中佔有最高佔有率。

- 在美國,製藥業是北美市場的主要動力,正著力轉型為生態產業。

- 在北美地區,美國佔據全球藥品銷售收益的最大佔有率。據阿斯特捷利康稱,到 2024 年,美國預計將在藥品上花費 6,050 億至 6,350 億美元。

- 加拿大醫藥市場排名全球第九,佔全球市場銷售額的2.1%。加拿大的製藥業在政府的直接支持下正在取得進展。例如,2021 年 8 月,加拿大政府宣布對糖尿病研究進行新投資。

- 最近,美國食品和飲料行業經歷了顯著成長,這可能會推動市場研究。

- 2022年3月,雀巢宣布計畫在美國亞利桑那州鳳凰城投資6.75億美元,生產燕麥奶咖啡奶精等飲料。該工廠計劃於 2024 年運作。

- 此外,加拿大和墨西哥對製藥、食品和食品和飲料行業使用的發酵化學品的需求也在增加。

- 因此,上述因素導致預測期內北美發酵化學品市場的需求不斷增加。

發酵化學品產業概況

全球發酵化學品市場部分整合。主要參與企業包括(排名不分先後)BASF股份公司、嘉吉公司、贏創工業股份公司、帝斯曼和龍沙。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 甲醇和乙醇產業需求不斷成長

- 製藥業需求增加

- 其他司機

- 抑制因素

- 製造流程複雜,成本高

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 產品類別

- 酒精

- 有機酸

- 酵素

- 其他產品類型

- 目的

- 工業的

- 食品和飲料

- 藥品/營養品

- 塑膠和纖維

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太地區

第6章競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AB Enzymes

- Ajinomoto Co., Inc.

- ADM

- BASF SE

- Biocon

- BioVectra

- Cargill, Incorporated.

- Chr. Hansen Holding A/S

- DSM

- Evonik Industries AG

- Lonza

- MicroBiopharm Japan Co., Ltd.

- Novasep

- Novozymes

- Teva Pharmaceutical Industries Ltd.

第7章 市場機會及未來趨勢

- 生態化學的成長機會

- 其他機會

The Fermentation Chemicals Market size is estimated at USD 194.04 billion in 2024, and is expected to reach USD 242.98 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the fermentation chemicals market. However, the market recovered significantly in 2021.

Key Highlights

- Over the short term, the growing demand from the methanol and ethanol industry and increasing demand from the pharmaceutical industry are major factors driving the studied market's growth.

- However, high costs due to the complexity involved in the manufacturing process are likely to restrain the growth of the studied market.

- Nevertheless, growing green chemistry opportunities will likely create lucrative growth opportunities for the global market soon.

- The North American region dominates the fermentation chemicals market, with the largest consumption coming from countries like the United States, Canada, and Mexico.

Fermentation Chemicals Market Trends

Food and Beverage Sector to Dominate the Market

- Fermentation usually signifies that the action of microorganisms is desirable. Fermentation produces alcoholic beverages such as wine, beer, and cider. Fermentation is also used to produce dairy products and leavening bread.

- Fermentation chemicals are highly demanded by the food and beverages industry as it is the oldest biotechnology used by human beings to produce safer, more stable, and better foodstuff.

- In the Asia-Pacific region, the demand for processed food is growing due to increasing lifestyle changes, disposable income of people, working professionals, and preferences for fast food. Consumers prefer ready-to-eat foods as these require considerably lesser time for cooking, are fresh, and include attractive and sturdy packaging.

- Also, China is expected to continue to be Asia's largest food market, and India and Southeast Asia will witness the most significant increases in food spending.

- The market for food processing in North America is robust due to the excessive dependence of people on packaged food products and the strong foothold of the food processing companies. PepsiCo, Tyson Foods, and Nestle are large food processing companies operating in the region.

- Germany is by far Europe's largest market for foods and beverages, home to more than 83 million of the world's wealthiest consumers. In 2023, the German food market is expected to generate USD 245.50 billion in revenue. The market is expected to grow annually by 3.64% between 2023 to 2027.

- According to OIV (International Organisation of Vine and Wine), global wine production in 2022 amounted to about 258 million hectoliters.

- Additionally, in 2022, Italy was the world's top wine producer and exported the most wine, amounting to 21.9 million hectoliters. The top exporters were the other two top wine producers. France exported 14 million hectoliters, while Spain exported 21.2 million.

- Such factors likely support the demand for the studied market from the food and beverages segment.

North America to Dominate the Market

- North America currently accounts for the highest global fermentation chemicals market share.

- The pharmaceutical industry highly drives the market for North America in the United States and its growing focus to turn itself into a green industry.

- In North America, the United States accounts for the largest share of the revenue generated by global pharmaceutical sales. In 2024, the United States is projected to spend between USD 605 and 635 billion on medicines, according to AstraZeneca. It will make the country achieve the highest pharmaceutical spending by far.

- Canada's pharmaceuticals market is the ninth-largest globally, with a 2.1% share of global market sales. The pharmaceutical sector in Canada is progressing under direct support from the government. For instance, in August 2021, the government of Canada announced new investments in diabetes research.

- Recently, the food & beverage industry witnessed major growth in the United States, likely to drive the market studied.

- In March 2022, Nestle announced its plans to invest USD 675 million in a new plant in Metro Phoenix, Arizona, the United States, to produce beverages, including oat milk coffee creamers, as consumer demand for plant-based products increases. The plant is expected to be operational in 2024.

- Additionally, there is an increasing demand for fermentation chemicals from Canada and Mexico for use in the pharmaceutical, food & beverage industries.

- Therefore, the abovementioned factors contribute to the increasing demand for the fermentation chemicals market in North America during the forecast period.

Fermentation Chemicals Industry Overview

The global fermentation chemicals market is partially consolidated in nature. The major players include BASF SE, Cargill, Incorporated., Evonik Industries AG, DSM, and Lonza, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Methanol and Ethanol Industry

- 4.1.2 Increasing Demand from the Pharmaceutical Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost Due to the Complexity Involved in the Manufacturing Process

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Alcohols

- 5.1.2 Organic Acids

- 5.1.3 Enzymes

- 5.1.4 Other Product Types

- 5.2 Application

- 5.2.1 Industrial

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceutical and Nutritional

- 5.2.4 Plastics and Fibers

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AB Enzymes

- 6.4.2 Ajinomoto Co., Inc.

- 6.4.3 ADM

- 6.4.4 BASF SE

- 6.4.5 Biocon

- 6.4.6 BioVectra

- 6.4.7 Cargill, Incorporated.

- 6.4.8 Chr. Hansen Holding A/S

- 6.4.9 DSM

- 6.4.10 Evonik Industries AG

- 6.4.11 Lonza

- 6.4.12 MicroBiopharm Japan Co., Ltd.

- 6.4.13 Novasep

- 6.4.14 Novozymes

- 6.4.15 Teva Pharmaceutical Industries Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Opportunities for Green Chemistry

- 7.2 Other Opportunities

精密發酵市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按生產成分、微生物、最終用戶產業、地區和競爭細分

精密發酵市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按生產成分、微生物、最終用戶產業、地區和競爭細分 2023-2030 年全球發酵化學品市場規模研究與預測(按產品、應用和區域分析)

2023-2030 年全球發酵化學品市場規模研究與預測(按產品、應用和區域分析) 發酵化學品市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2024-2030

發酵化學品市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2024-2030 2024 年精準發酵全球市場報告

2024 年精準發酵全球市場報告 發酵化學品市場報告:2030 年趨勢、預測與競爭分析

發酵化學品市場報告:2030 年趨勢、預測與競爭分析 發酵化學品市場:按產品、按應用分類 - 2024-2030 年全球預測

發酵化學品市場:按產品、按應用分類 - 2024-2030 年全球預測 2024 年發酵化學品全球市場報告

2024 年發酵化學品全球市場報告 全球工業發酵化學品市場預測(截至 2030 年)

全球工業發酵化學品市場預測(截至 2030 年) 精準發酵的技術成長機會

精準發酵的技術成長機會 全球哺乳動物細胞發酵技術市場規模研究與預測(按類型、按應用、最終用途和區域分析),2023-2030 年

全球哺乳動物細胞發酵技術市場規模研究與預測(按類型、按應用、最終用途和區域分析),2023-2030 年